Taco, Toasters, Fire and Oranges

After a brief hiatus, US President Donald Trump’s trade war is back in full swing. Or is it? The 90-day suspension of the reciprocal tariffs announced in April has now expired, and Trump sent letters to countries outlining where they stand.

For the most part, the tariffs are very similar to those proclaimed on what Trump termed “Liberation Day”, April 2. The only difference seems to be rounding, so that South Africa gets 30% instead of 34%, as was the case in April. Have we gone full circle?

Not quite. The tariffs are set to take effect on 1 August, leaving some room for negotiations. However, trade deals normally take years to finalise and are incredibly detailed. So far, only Vietnam, Indonesia, China and the UK have managed to reach an agreement with the US, and these have been fairly vague. Uncertainty persists.

Taco

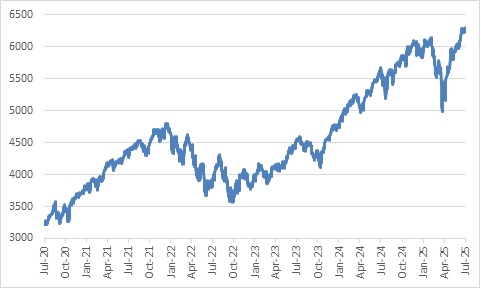

In contrast to the market sell-off after the first Liberation Day, the response this time round has been very muted even though the proposed tariff levels are very similar. The S&P 500 continues to trade near record highs, and the strength of the market, along with ongoing resilience in the US economy and the recent passage of the Big Beautiful Bill, has probably emboldened Trump to get tough on trade again. The tariffs have also already raised quite a bit of revenue for the government - $50 billion in May and June - without severe economic consequences so far.

Chart 1: S&P 500 index

Source: LSEG Datastream

This is consistent with a pattern stretching back to Trump’s first term, namely going on the attack when the wind is in his sails and pulling back when there are headwinds. This is exactly what happened in April, when the market crash caused him to suspend most of the tariffs. For this reason, the idea of TACO -Trump Always Chickens Out - has taken hold with investors. The market now fully believes that this is a bluff and a negotiation tactic, and that the final tariffs will not be as high as currently threatened.

The problem is that something or someone will need to convince Trump to back down and accept more reasonable tariffs. The someone could be Republican politicians, worried about a voter backlash, or the CEOs of major companies, concerned about their margins. The something would be an adverse market reaction or bad economic data. Neither is likely until there is some unhappiness.

Even then, Trump is clearly committed to the idea of higher tariffs. There is no doubt that tariffs will settle well above the 3% level they averaged at the start of the year. Where and when they settle remains an open question. An average tariff rate of 10% to 15% is very high, but manageable and can probably be absorbed by various players across the value chain without significant damage. More than that, and someone, probably the end consumer, faces a price shock.

For now, there is economic resilience. America’s biggest banks reported second quarter earnings last week, and they all noted that their customers were not showing major signs of stress. However, this doesn’t mean it is a rosy picture. Companies stockpiled goods before the tariffs kicked in meaning that consumers have not been exposed to the full extent of price increases yet. And while labour market data does not point to mass layoffs, people who have lost jobs are struggling to find employment. A further drag is the mass arrests of undocumented immigrants and sharply lower numbers of new immigrants. This has probably not showed up in official employment data yet, but nonetheless implies fewer people available to work and therefore earn and spend.

All this still points to a softening of the US economy towards the end of the year, something that was likely to happen anyway, but that new policies will intensify. Ultimately the tariffs have to show up as some combination of higher consumer prices, lower sales (where people refuse to pay more) and squeezed corporate margins (when firms cannot pass tariff costs on). Exporters will bear some of the pain, but most of it will fall on Americans.

Toasters

There are already hints of rising consumer prices for goods. Remember that services account for two-thirds of the US consumer price index (CPI), and of that, a substantial portion is related to housing rents, which continue to fall gradually from elevated levels.

The June CPI shows that prices are rising for appliances, such as toasters and microwaves, and also clothing. These are goods that are predominantly imported.

Click here to read more...