Submerging, diverging and emerging markets

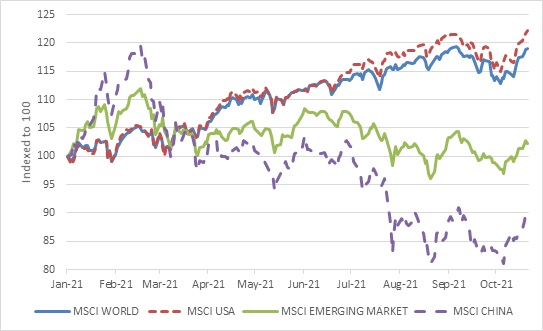

Emerging markets have underperformed developed markets this year. On the equity side, the MSCI World Index has returned 19% in dollars in 2021, against the 2% of the MSCI Emerging Markets Index.

The underperformance is less stark in the bond market, since developed economy government bonds have sold off to a similar extent as emerging market government bonds, but developed market corporate bonds have outperformed.

Chart 1: Emerging market and developed market equities in 2021 in US dollars

Source: Refinitiv Datastream

In equities, a big part of the reason for the emerging market underperformance is that the MSCI World Index is dominated by the US with a 67% weight, and it has had a stellar run this year. In contrast, the biggest country in MSCI’s emerging market equity index is China, with a 33% weight, with a negative performance this year for reasons we’ll get into below.

Emerging markets have always been a mixed bunch, but the current global environment is causing a notable divergence. In general, emerging markets have been harder hit by the Covid-19 pandemic than advanced economies. The latter simply had more financial resources to respond to the crisis, both in terms of fiscal and monetary policies. Richer nations have also been able to vaccinate a larger share of their populations faster, though often in fits and starts.

The International Monetary Fund recently estimated that advanced economies will return to their pre-pandemic growth trend in 2022. In other words, they will have caught up and be back where they would have been had the pandemic not happened. But emerging economies excluding China will still be 5% below that trend, China itself will be 2% below that trend and the poorest developing countries will be almost 7% below a no-pandemic scenario. Aside from the pandemic itself, which is by no means over and continues to distort the global economy, there are other factors at play in individual emerging markets.

China’s three headaches

China is the most important emerging market by far. It joined the World Trade Organisation almost exactly 20 years ago. Although few realised it at the time, that was one of the most consequential events in modern economic history, as the country would come to dominate trade in manufactured goods. Exports have become less important to Chinese growth over the years, but it benefited as people across the world switched from spending on services to spending on goods during the pandemic.

Three issues loom large in China today, but there is an underlying connection between them, namely the government’s desire to transition the economy to a more sustainable, balanced and equitable growth path. Firstly, there’s the crackdown on monopolistic technology companies, as well on private education and other contributors to the cost of living of China’s urban middle class.

Secondly, China is experiencing widespread load-shedding due to an energy crisis that is partly due to the shift away from polluting coal-fired power. This impacted third quarter economic growth, which was the slowest in decades, excluding 2020’s pandemic-affected quarters.

Thirdly, the crackdown on excessive and unsustainable debt in the property sector has pushed a number of developers to the brink of bankruptcy, most notably Evergrande (though it somehow managed to scrape together enough cash to make a key interest payment last week). Investment in the property sector as a share of overall economic activity increased dramatically in the past decade, overtaking exports in importance. This major growth driver is likely to be much more subdued in the years ahead, particularly given its poor demographic profile. This could have a negative impact on commodity exporters like Brazil and South Africa, since the property sector was a big source of demand for commodities, particularly steel. Whether this will be offset over time by demand from the global energy transition remains to be seen. For the time being, commodity prices are still elevated, partly because of supply problems.

Emerging markets come in all shapes and sizes. India is another billion-plus emerging nation, but its economic make-up is very different from China’s. Others include oil and gas exporters (Russia, Nigeria, Saudi Arabia), high-tech manufacturers (Korea and Taiwan), financial centres (Singapore and Hong Kong), non-oil commodity exporters (Chile, South Africa, Indonesia) and commodity importers (Egypt, Turkey and Eastern Europe). Some are tourist paradises (like Thailand and Mauritius). Some are fallen angels (Greece and Argentina) and some are rising stars (Vietnam). Finally, there are countries whose underdeveloped financial markets mean they are out of bounds for most investors, despite posting impressive economic growth rates (such as Ethiopia).

The big divergence

The big divergence at the moment is driven by the types of imports and exports countries specialise in, as well as their current inflation experience, and the two are linked. Consumers in developing countries tend to spend a greater portion of their incomes on food and energy than their peers in rich countries. The surge in global food and fuel prices therefore takes a bigger bite out of disposable incomes. Since these commodities are priced in dollars, exchange rate movements can worsen the situation.

Tourism-dependent economies are clearly still battling and likely face a long road to recovery. A return to normal tourism numbers in these countries requires not only higher domestic and international vaccination rates, but also a willingness on the part of holiday-makers to once again take long flights into the metaphorical unknown. If people’s attitudes to travel have changed, it could be a case of Long Covid for the economies of these countries.

Korea and Taiwan are the biggest exporters of semi-conductors (microchips) that are as scarce as hen’s teeth these days. Overall export values for these two countries are at record levels. As an aside, it is a matter of debate whether they are still emerging markets from a developmental point of view given their high living standards, but MSCI still classifies them as such in its flagship emerging markets equity index, where they are the number two and three with low single digit weights.

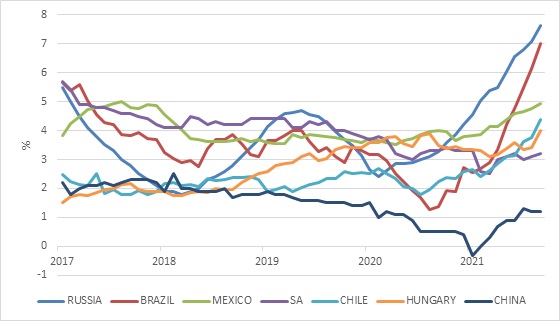

Net energy exporters are clearly smiling. Russia is a top five global exporter of oil, gas and coal and clearly benefits. But Russia is among many emerging markets whose inflation rates have risen sharply, necessitating interest rate hikes to 7.5% from 4.25% a year ago. Core inflation, excluding food and fuel prices, hit 7.6% in September.

Chart 2: Core inflation rates in selected emerging markets

Source: Refinitiv Datastream

Brazil is another emerging market battling inflation, even though it too became an energy exporter in recent years thanks to its offshore oil fields. The central bank has been aggressively hiking short-term rates from 2% a year ago to 6.5%. It might need to do more as headline inflation has hit double-digit levels, while core inflation is up to 7%. Brazil experienced hyperinflation in the early 1990s, requiring the currency to be changed four times between 1989 and 1994. These memories are still fresh in people’s minds and the central bank needs to demonstrate that it will not let inflation run riot again. As a result, Brazil’s 10-year government bond yield has shot up above 11%, even higher than it was during the pandemic panic in March last year. It doesn’t help that the market is anxious that the government might open the spending taps ahead of next year’s presidential elections. Brazil’s government debt level is already one of the highest in its peer group (ahead of even South Africa).

Turkey has gone in the other direction, cutting interest rates last month and again last week (by 2%). But Turkey has been a special case for the past five or so years. President Erdogan is following a growth-at-all-costs strategy, bullying his central bank into keeping rates low despite persistent double-digit inflation rates over this period. In fact, two weeks ago he fired two top central bank officials who were opposed to further monetary easing. The lack of central bank credibility means Erdogan’s government pays 18% to borrow over 10 years, the highest by far of any G20 country apart from Argentina, which is itself a special case. Turkey has low levels of government debt, but it has high levels of private sector debt denominated in hard currency, so the slump of the lira to record lows against the dollar will hurt.

In the middle, Cyril

South Africa sits in the middle of some of these trends. It has benefited greatly from commodity price increases, but it is an importer of fuel products. It has also lagged in vaccinating its population, although this has picked up speed recently. Its hospitality sector is desperate for foreign visitors, but the economy is not as dependent on tourism as Egypt, Thailand and Turkey.

Importantly, inflation is still well behaved. Consumer inflation increased in line with the consensus forecast to 5% year-on-year in September, from 4.9% in August. Inflationary pressures still largely stem from global commodity prices, with food inflation at 7% and fuel at 19%. Government entities are also culprits, with electricity inflation coming in at 14%.

However, core inflation remains muted at 3.2% year-on-year. Since it includes categories that are set by the interaction of supply and demand in the domestic economy, it suggests underlying inflation is still tame, unlike some other emerging markets. This includes the key rental inflation categories, which posted increases of only 0.9% for actual rents, and 1.3% for owners’ implied rent. This means that the SA Reserve Bank can still afford to take it easy on rate hikes, and a gradual cycle will likely kick off next year. The Reserve Bank also enjoys a large degree of credibility, which means it needn’t overreact.

Over the past 30 years, each successive interest rate cycle had lower peaks and troughs, and this is likely to be the case in the future too.

It is on the fiscal policy side that South Africa lost a great deal of credibility, which it is now attempting to regain. Next week’s Medium Term Budget will shed more light on the country’s fiscal trajectory. As the examples above show, policy credibility is absolutely crucial and once lost, it is very slow and expensive to regain. Quite simply, investors are sceptical that the government is truly committed to fiscal consolidation and expect political considerations to prevail. They are prepared to lend to the government – it has not struggled to sell bonds – but at a price. That is the main reason why bond yields are so much higher than expected inflation, despite recent improvements in tax revenues.

Fear the Fed

The final complication for all emerging markets is the looming tighter monetary policy from the US Federal Reserve. The world still runs on dollars, and therefore the big emerging market meltdowns of the past four decades have all coincided with a period of rising US rates and dollar scarcity. This doesn’t mean rising rates are bad for emerging markets all the time. It depends on the conditions that gave rise to the rate hikes. If the Fed hikes because the US economy is in good health, the broader impact has historically been limited. If the Fed has to tap the brakes in response to unwelcome inflation, it is a different story.

Chart 3: Developed versus emerging market equity valuations

Source: Refinitiv Datastream

Multi-nation diversification

Finally, it’s worth asking whether local investors should even consider investing in other emerging markets, given that we already live in one.

South Africa is a small portion of the global emerging markets universe, accounting for 3% of MSCI’s emerging markets index. So there is a lot of opportunity in the emerging market universe beyond South Africa and its heavy reliance on commodities. In fact, the emerging market universe has changed dramatically over the past decade or so. It is much less of a proxy for commodity prices now, and firmly centred on Asia with a larger exposure to technology shares and the growing middle-class consumer in those countries. And although multinational companies listed in developed economies will sell to those consumers, investors who want “pure play” exposure will have to turn to the domestic stock exchanges, where these shares are often under-researched and under-appreciated. With the exception of India, emerging market equities are much cheaper than the US, and also trade at discount non-US developed markets.

The bonds also offer much higher yields, though arguably South African investors don’t need emerging market bond exposure given the attractive local yields. So in a nutshell, emerging market exposure does make sense.

More broadly, local investors need to be aware of what is happening in emerging markets, since some of those trends will impact South Africa too. However, others might pass us by. As always, proper diversification is the name of the game.