Sub Saharan Africa Mergers and Acquisition transactions totalled US$39.6 billion in the first nine months of 2022

Refinitiv, a London Stock Exchange Group business, today released the investment banking analysis for the Sub-Saharan African for the third quarter of 2022.

Investment Banking Fees

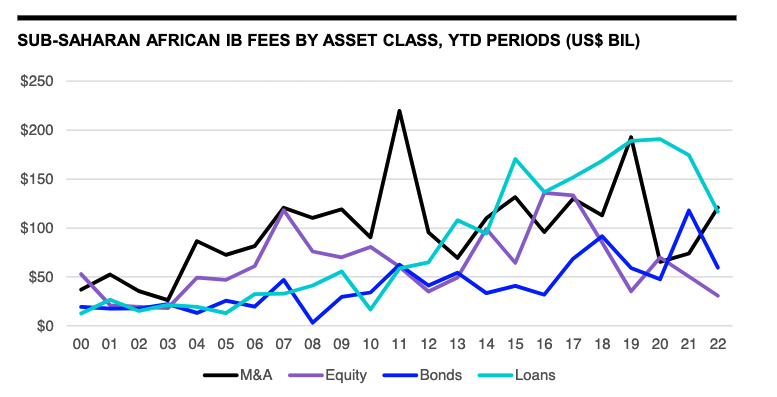

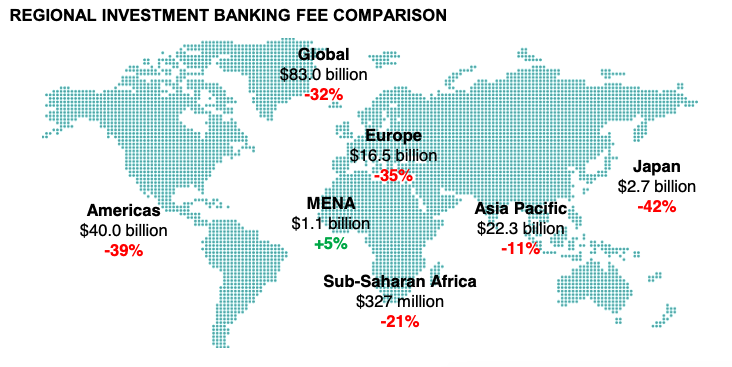

An estimated US$327.5 million worth of investment banking fees were generated in Sub Saharan Africa during the first nine months of 2022, 21% less than the same period in 2021 and the lowest first nine-month total in the region since 2013. Fees totalled US$112.9 million during the third quarter of 2022, an increase of 46% from the previous quarter.

Advisory fees earned from completed M&A transactions in the region reached US120.8 million, a 64% increase from the first nine months of last year and a three-year high. Equity capital markets underwriting fees declined 39% to US$30.8 million, the lowest first nine-month total since 2003, while debt capital markets fees declined 50% to US$59.3 million. Syndicated lending fees declined 33% to US$116.6 million, the lowest first nine-month total since 2014.

Seventy-two percent of all Sub-Saharan African fees were generated in South Africa during the first nine months of 2022, followed by Mauritius (10%) and Nigeria (5%). Citi earned the most investment banking fees in the region during the first nine months of 2022, a total of US$26.7 million or an 8% share of the total fee pool.

Mergers & Acquisitions

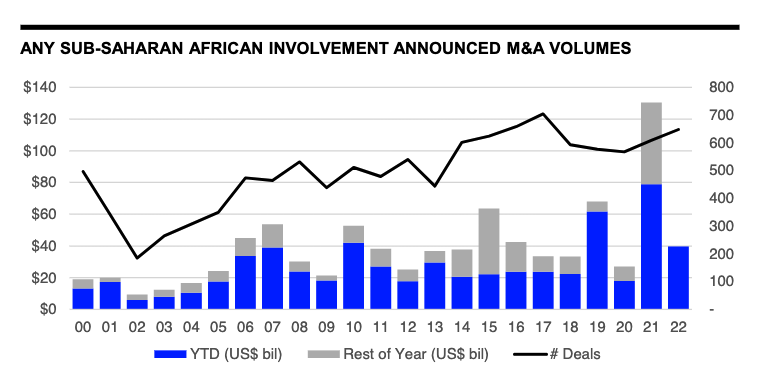

The value of announced M&A transactions with any Sub-Saharan African involvement reached US$39.6 billion during the first nine months of 2022, 50% less than the value recorded during the same period in 2021. Despite the decline in value, the number of deal announcements in the region increased 6% from last year to the highest first nine-month total since 2017.

Deals involving a Sub-Saharan African target totalled US$24.4 billion during the first nine months of 2022, down 61% from the same period last year but higher than the level recorded during each of the previous seven years. Domestic deals declined 82% from last year’s record high value to US$9.3 billion, while inbound deals increased 47% to US$15.1 billion as the number of transactions increased 11% to an all-time high of 243. Sub-Saharan African outbound M&A totalled US$11.1 billion, down 1% from last year but the second highest first nine-month total since our records began in 1980.

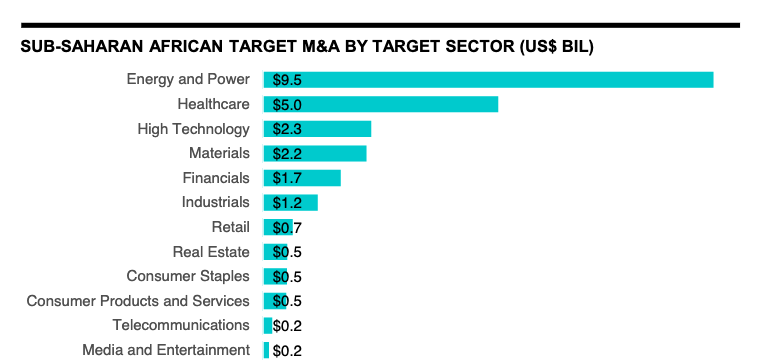

The Energy & Power sector was most active, with deals targeting energy & power companies accounting for 39% of Sub-Saharan African target M&A during the first nine months of 2022, followed by Healthcare with 20%. South Africa was the most targeted nation, followed by Angola and Nigeria. Scotiabank topped the any Sub-Saharan African involvement announced M&A financial advisor league table during the first nine months of 2022.

Equity Capital Markets

Sub-Saharan African equity and equity-related issuance totalled US$993.2 million during the first nine months of 2022, the lowest first nine-month total since 2003. Proceeds raised by companies in the region declined 15% compared to the first nine months of 2021, while the number of issues fell 18%.

All proceeds were raised by follow-on issuance with Pepkor Holdings, MTN Nigeria Communications and South African coal exporter ThungelaResources among those in the region raising new equity funds from follow-ons. No convertible or initial public offerings were recorded in Sub-Saharan Africa during the first nine months of 2022.

Issuers in South Africa raised more in the equity capital markets than any other Sub-Saharan African nation during the first nine months of 2022, a total of US$716.1 million, while Nigerian issuers raised a combined US$277.1 million. Citi took first place in the Sub-Saharan African ECM underwriting league table during the first nine months of 2022 with a 37% market share.

Debt Capital Markets

Sub-Saharan African debt issuance totalled US$21.6 billion during the first nine months of 2022, down 43% from the value recorded during the same period in 2021. The number of issues declined 40% from last year at this time. US$4.2 billion was raised during the third quarter of 2022, down 35% from the previous quarter and the lowest quarterly total in two years.

South Africa was the most active issuer nation during the first nine months of 2022, accounting for 47% of total bond proceeds, followed by Ivory Coast (27%) and Nigeria (10%). Government & agency issuers account for 62% of proceeds raised during the first nine months of 2022, while issuers in the technology sector account for 24%. Citi took the top spot in the Sub-Saharan African bond bookrunner ranking during the first nine months of 2022, with US$3.1 billion of related proceeds, or a 14% market share.