Stormy September in the markets

Every once in a while, investors collectively decide that risks that were lurking in the background are now worth paying attention to. When that happens markets can endure serious wobbles. This is pretty much September’s story, when a perfect storm of three risks suddenly loomed larger than before: inflation (and interest rates), Chinese property, and the US debt ceiling.

Dancing on the ceiling

Starting with the latter, the debt ceiling is a self-imposed limit on the total amount of allowable outstanding federal debt. Ironically, it was initially put in place to make borrowing easier. Before 1917, Congress had to approve every single loan. During WW1, the law was changed to provide the US Treasury with greater flexibility to borrow as needed, provided total debt was below a certain level. This limit was routinely raised without fanfare, but in the last three decades lawmakers have started using the debt ceiling as a political tool.

Even worse, Congress already approved the spending, but now it cannot agree on approving the associated borrowing. In other words, this is not about prudently limiting future borrowing, but about paying for bills already incurred.

The US government has now hit the debt limit. Once cash reserves run out it cannot meet financial obligations like paying salaries in full. From the market’s point of view, the worst-case scenario is a failure to make interest payments, a default on what are supposed to be the safest assets in the world and the bedrock of global financial markets.

Though Congress hastily approved a bill last week to suspend the debt ceiling until December, that is merely kicking the can down the road. A longer-term solution is needed, and is likely to emerge, but is still caught up in the political bickering over President Biden’s two other big spending plans on physical and social infrastructure. Winston Churchill, whose mother was American, famously said you could count on the US to do the right thing but only once they’ve tried everything else. Previous episodes of debt ceiling brinkmanship did not end up having a major market impact.

Nonetheless, this is a shambolic way of running the finances of the world’s largest economy. In contrast, as an aside, South Africa’s budgeting and debt management process is extremely orderly and transparent even if total debt levels are too high. Investors, taxpayers and the public always know what to expect over the next three years.

The real state of real estate

On the other side of the world, the focus in China was on a potential restructuring of heavily indebted real estate developer China Evergrande, which missed a key interest payment. It’s clear that it is unable to fully repay its enormous pile of debt and other obligations. The only question is what the impact will be. While Evergrande’s share and bond prices have predictably crashed, there is no sign yet of a broader financial panic, such as a run on the banking system or wholesale funding markets. Beijing will probably attempt an orderly piecemeal dismantling of the giant developer, and given its deep pockets and centralised control, can pull it off. But weakness in the broader real estate sector, a driver of the country’s breakneck growth over the past three decades, is likely to persist or even worsen. There seems to already be an oversupply of housing. With developers across the board likely to find it much tougher and more expensive to fund themselves, new building activity could slow to a crawl.

There are short- term worries too. Growth in the world’s number two economy is already struggling from Covid-19 lockdowns and now has to contend with power outages that have sent the September manufacturing purchasing manager’s index into contractionary territory below 50 index points. With China and Asia more broadly being the world’s factory, the electricity blackouts and Covid-19 outbreaks across the region have intensified the global supply-chain problems.

Tenacious inflation

This brings us to inflation. The surge in inflation is still largely a function of pandemic-related distortions. Companies everywhere face rising costs and shortages of key inputs, including labour.

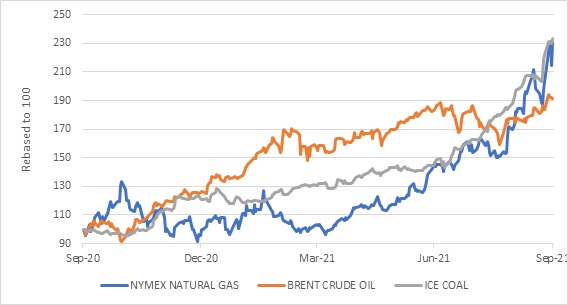

Chart 1: Energy prices over the past year

Source: Refinitiv Datastream

Recently, energy prices have shot up, particularly natural gas prices in Europe. Though higher oil and gas prices will have a direct impact on a consumer price index, these tend to be short-lived. However, when higher energy costs cause companies across a broad range of sectors to raise their selling prices, we have a so-called second-round effect. This is when we should start feeling uncomfortable. And then if workers bid up their wages in response, we have the beginnings of a wage-price spiral. Clearly, this requires that companies have pricing power and workers bargaining power. Farmers for instance, face rising costs for diesel and fertiliser, but cannot raise prices. In a global marketplace, they are price-takers. But in other industries, demand is strong enough for firms to dare raise prices, while the pandemic has left many sectors short of workers, forcing wage increases. These are still early signs, but something investors are becoming more nervous about.

It doesn’t help that petrol pumps across the UK have been running dry, recalling the fuel lines of the 1970s, the era of dreaded stagflation. A shortage of truck drivers in the UK is the main reason these petrol stations cannot refill quickly, but supply disruptions across the energy universe in oil, gas, coal and refined products is a global phenomenon. The weather has also played a big role.

The end (of free money) is nigh

The major central banks insist that such pandemic-related distortions will eventually fade, and that will lead to the current inflation surge abating. But they are also laying the groundwork for removing emergency monetary support. After all, when the pandemic is no longer distorting the economy, those emergency measures will not be needed anymore. First up is the Fed, who will in all likelihood start gradually tapering its monthly bond purchases from December or January. It could start raising rates by the end of next year. The Bank of England also recently indicated that it could start raising rates in the “medium-term”. The European Central Bank is far away from rates increases, but will probably reduce the scale of its emergency bond buying early next year. The Bank of Japan, as always, is a special case. Japan seems to have escaped the global inflation surge and consumer inflation there is still a big round zero.

Emerging markets have been increasing rates in droves, with a total of eleven hiking in the month (though South Africa stayed on hold).

In other words, the era of free money is coming to a close. This doesn’t mean of course that rates are about to rocket higher, killing off the global economic recovery. All indications are that central banks will be gentle in removing stimulus. But higher rates can negatively impact share prices by putting downward pressures on company valuations. In other words, if investors are prepared to pay less for each dollar of profits, even if the profits themselves are otherwise unaffected. Of course, higher borrowing costs can also reduce profitability.

So what was the market response to these three rising risks? In simple terms, global equities fell, bond yields rose and the dollar gained. There were few places to hide.

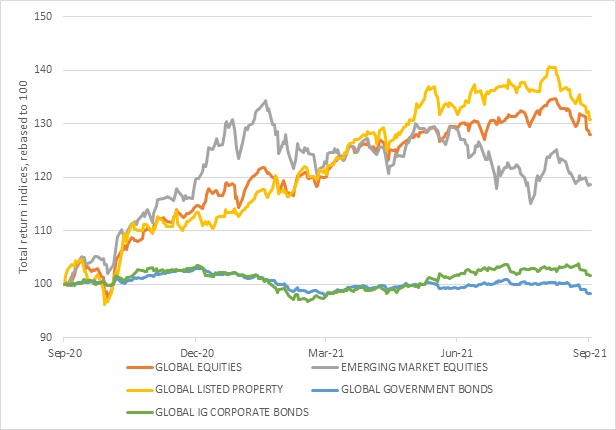

Chart 2: Global asset class performance over the past year in US$

Source: Refinitiv Datastream

After a run of seven straight positive months, it should not have been a huge surprise that global equities were negative in September, but the decline was severe with the MSCI All Country World Index experiencing its worst month in a year. It fell 4% in US dollars, reducing the year-to-date gain to 11%. Over 12 months, global equities returned 28%, benefiting from strong growth in corporate earnings.

The benchmark US 10-year Treasury yield increased from 1.3% to 1.5%, but remains extremely low in absolute terms. However, when yields are this low, even small movements can cause big capital losses. The Bloomberg Global Aggregate Bond Index lost 1.8% in dollars in the month. This means the global fixed income benchmark has lost 4% so far this year.

Global listed property was also sharply negative in September, with the FTSE/EPRA Nareit Developed Index losing 5.8% in dollars, cutting the year-to-date return to 15% and the one-year return to 29%. This is ahead of global equities and impressive considering how badly parts of the sector have been hit by the pandemic.

Local followed global

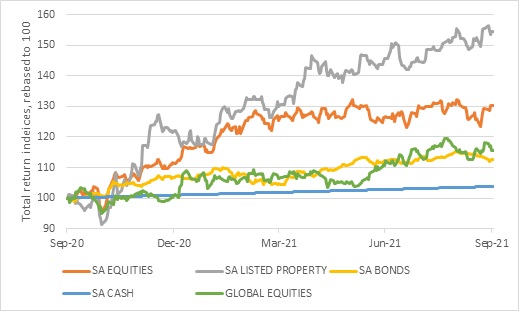

Local equities followed global markets lower in September. The FTSE/JSE Capped SWIX lost 1.4% in the month, which reduced the return for the first nine months of the year to 16.9 % and the 12-month return to 30%. The third quarter return was 3%. The FTSE/JSE All Share Index lost 3% in the month. It has a greater weighting to mining shares.

Chart 2: Local asset class performance over the past year in rands

Source: Refinitiv Datastream

Weaker industrial and precious metals prices pulled down the shares of mining companies, particularly PGM miners, but Sasol shot up on higher energy prices. The resources index lost 9% in the month, reducing the year-to-date return to 8.7% and the one-year return to 17%.

The industrials index was marginally negative in September. It lost 0.7% in the month, dragging year-to-date returns down to 9% and 12-month returns to 17%.

On the other hand, financials were positive again in September, gaining 2%. This means financials are ahead on a year-to-date and one-year basis, with returns of 26% and 51% respectively. It means the financial index has finally regained pandemic-related losses.

Listed property was marginally lower in September. The FTSE/JSE All Property Index lost 0.3% in the month, but the 12-month return remains impressive at 58%. Despite this strong recovery, the index has yet to return to pre-pandemic levels.

Local bonds sold off with their global counterparts, and the All Bond Index lost 1.9% in the month. However, the year-to-date return of 5.4% and one-year return of 12.6% is still well ahead of cash.

In summary

It was a September we’d rather not remember. At least the currency played the role of shock absorber. The rand lost 4% against the dollar in the month, cushioning the blow from declines in global equity prices. This highlights the importance of having multiple sources of return in a portfolio. Moreover, we should remember that markets never move up in a straight line. Corrections are normal as investors reassess growth prospects and risks from time to time. The benefit long-term investors have over traders is that they don’t need to show a profit every month. Instead, they can wait patiently for opportunities to emerge and value to be unlocked. Following last month’s declines, local bonds and equities are even more attractively priced.