Staying invested worked

Exactly 110 years ago this week in 1911, the New York Times sent the first commercial telegram that travelled around the world. The telegram, which simply read “This message sent around the world,” was relayed by 16 different operators across the world and took 16 minutes to return to New York.

Today, information can be sent anywhere virtually instantaneously. The entire global economy and its financial markets rely on the speedy and accurate transmission of information across vast distances. We rely on satellites to pinpoint the location of everything from delivery vans to giant oil tankers. Every day, so-called high frequency traders deploy billions of dollars to exploit millisecond advantages in the prices of financial securities. In fact, high frequency trading is estimated to account for about half of US equity trading volumes.

Everything is rapid, and everything is global.

It makes it difficult to keep your head when making investment decisions. For the proverbial man in the street, there is probably too much information. An endless number of websites and newsletters offer investment tips, sometimes touting get-rich-quick schemes or warning of an imminent crash in markets. We can log in and check portfolio values by the minute, when it wasn’t that long ago that we had to wait for statements to arrive by mail. This increased transparency is fantastic on one level, but problematic on another. Having all the information at your fingertips increases the urge to act on it. If portfolio values are down, for whatever reason, many investors feel compelled to sell. If one portion of the portfolio is doing particularly well, why not move everything there?

However, not responding to the ups and downs of the market and sitting tight is an advantage that long-term investors have over traders. They need to show a daily or weekly profit. For the rest of us, investment success is determined over years if not decades.

South African investors – and South Africans in general - have been on an emotional rollercoaster ride in recent years. Sadly, the news has often been bad. And where there was good news, such as the ‘Ramaphoria’ rally of early 2018 when the new president promised a ‘New Dawn,’ it was soon overtaken by other events.

And yet here we are in the latter half of 2021, and investment returns have actually been reasonably good, all things considered. Investors who stayed the course during the various tough points have been rewarded.

Five years isn’t a particularly long period when it comes to investment - don’t call it “the long term” - but it is long enough to draw some conclusions.

Rand only slightly weaker

Despite everything, the rand weakened only modestly against the dollar over the past five years, about 1% per year. This runs somewhat counter to the popular perception that the rand is a prodigious decliner. Although it fell sharply during the global panic at the start of the pandemic in March and April last year, it recovered those losses for the most part fairly quickly.

In other words, the rand has not been a huge contributor to domestic portfolios in the sense of boosting offshore returns. However, it worked at a crucial point. When it fell sharply last year, it cushioned the blow of slumping global equity markets. At its worst point, the MSCI All Country World Index fell 34% peak-to-trough in dollars but only 21% in rand. And it recovered those losses in rand terms in only three weeks, while it took more than four months in dollar terms (a record recovery in terms of speed).

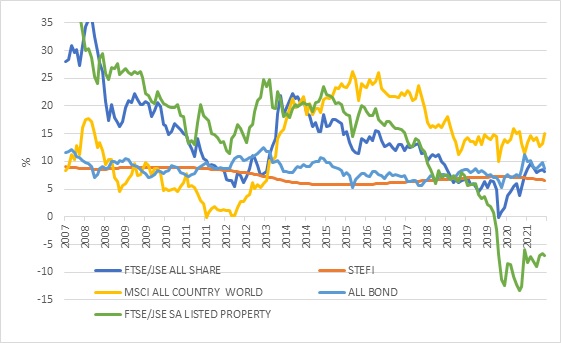

At the end of July, the best performing asset class in rand over the previous five years was global equity, with a 15% annualised return.

Chart 1: 5-year annualised returns in rand, %

Source: Refinitiv Datastream

A stellar period

In dollar terms, this represents one of the best five-year periods for global equities in recent decades. The post financial crisis period (2008 to 2014) delivered a better return, but this followed a 50% market crash. The five-year period prior to the crisis also delivered exceptional returns amid a debt-fuelled global economic boom. Prior to that, the dotcom bubble of the late 1990s also delivered very strong returns. On the downside, returns were negative on a rolling five-year basis in the early 2000s and again in 2009 and 2012.

In other words, we shouldn’t necessarily expect this stellar run to continue, or at least continue at the same pace. Markets are cyclical after all. Compounding matters means that valuations are elevated for global equities, which is a different way of saying that positive sentiment ran ahead of underlying earnings generation.

Above average valuations have historically led to below average subsequent returns. However, we are now seeing strong earnings growth coming through and that has stabilised valuations. It is also the US market, and within it the technology giants, that are particularly expensive. High valuations also don’t mean a crash is coming. These happen when there is a recession on the horizon and currently that is not the case.

A rough patch

South African equity returns were trending lower even before Covid hit. On the eve of the pandemic, the five-year return from the JSE All Share was only 4%, well below the return from money market and inflation. Already, many investors were writing off the asset class, looking jealously at the strong performance of global markets.

At the end of April, the JSE experienced its first negative five- year period since the early 1970s. It would have been understandable, perhaps, for investors to abandon hope of a recovery and sell out completely. After all, South Africa was knee-deep in the worst recession since the 1930s. However, the global economy bailed us out. The JSE started rallying in line with global equity markets, with the unexpected commodity boom adding rocket fuel. Local equities would end the 2020 calendar year in positive territory and, and at the end of July, the five-year annual return from the All Share was 8%, ahead of cash and inflation.

The FTSE/JSE Capped Swix, a less concentrated benchmark with more domestic exposure, still lags with a return of 4.4% per year over the past five years, in line with inflation.

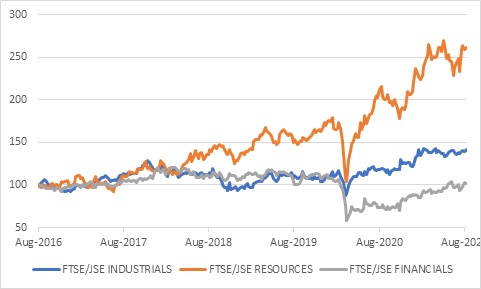

Now this has led to cries from some that the local market is completely divorced from economic reality. This is not true. Those companies whose fates are most closely linked to the domestic economy have generally seen their share prices struggle. A rough proxy is the JSE’s financials index, which has not yet recovered to pre-pandemic levels. But cycles do turn, and the moderate improvement in domestic economic growth prospects means the outlook for those firms is also better.

Chart 2: JSE economic sectors over five years

Source: Refinitiv Datastream

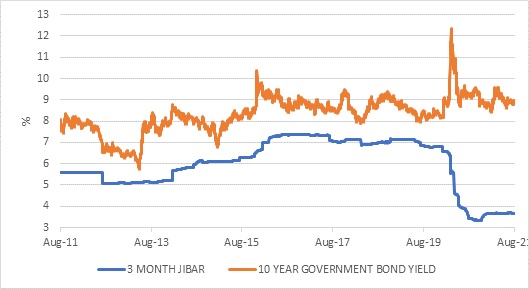

High yields

The South African bond market possibly had to deal with more bad news than even the local equity market in the past five years. After all, local equities have a substantial global component. On the other hand, the local bond market is dominated by a single issuer, the South African government, whose creditworthiness has steadily deteriorated as its debt burden has increased. Over this period, the South African government was downgraded to junk status by all three major ratings agencies and its bonds excluded from one of the main global indices. Cumulatively, net foreign sales amounted to R47 billion over this rocky period, and foreign ownership of government bonds declined from a peak of 43% to 29%.

Yet, the return form local bonds was 8.9% per year over the past five years, almost double the inflation rate.

The reason is that the starting yield was so high precisely because the market has worried about the government’s creditworthiness and commitment to sound policy since the sudden firing of Finance Minister Nene in December 2015. A succession of finance ministers since then has not changed this. If anything, considering how much global yields fell while South Africa’s stayed more or less the same, perceptions of creditworthiness have worsened.

The yield on the All Bond Index five years ago was 9%. The return over this period was therefore entirely from interest payments, not from capital gains (bond yields and prices move in opposite directions). The starting yield is even higher today, suggesting that the return outlook is still good. A lot of bad news is priced in.

Chart 3: SA long-term and short-term interest rates, %

Source: Refinitiv Datastream

Doldrums

The one asset class that is still in the doldrums is local listed property. As recently as 2015, it was the best performing asset class on a five-year view, beating even global equity. It was seen by many as the perfect investment, providing both high levels of income and growth. However, the stellar performance was clearly unsustainable, supported by questionable capital allocation, financial engineering and debt. It is a reminder how quickly an investment can go from darling to dog, and a warning not to fall in love with any particular investment. Again, markets are cyclical.

The sector was still dealing with the fallout when the pandemic hit. Ecommerce and remote working now pose structural risks since the exposure to office buildings and shopping malls in the local benchmark is much higher than in the more diversified global listed property benchmark. On the plus side, local listed property is as cheap as it has been in decades, offering an opportunity for investors who are prepared to sit through this current period of uncertainty.

Uncertainty

Of course, uncertainty is not confined to property. It is a part of life now, and possibly getting worse. The Delta variant continues to spread and there is no guarantee it won’t eventually be replaced by an even nastier variant, given that large numbers of unvaccinated people globally provide ample opportunity for mutation. Meanwhile, nature has greeted the release of the alarming new report from United Nations’ Intergovernmental Panel on Climate Change by unleashing hellish temperatures, wildfires as well as floods in various countries across the world.

Faced with these and many other worries, many investors will seek the safety of cash. However, cash returns (money market) have taken a decided blow. Though the five-year average is still elevated at 6%, the asset class is closely linked to the repo rate, which is currently 3.5%. There is no prospect of a return to the generous pre-pandemic cash returns. Yes, the Reserve Bank is likely to start raising rates in a few months’ time. The Bank’s own forecasts of inflation average around 4.5%, which means over the next two years there is no reason to raise rates aggressively. Over the last 25 years, each successive interest rate cycle had a lower peak and a lower trough as South African inflation and short-term rates gradually converge with the rest of the world.

Having said that, short-term interest rates here are still well above those of developed countries such as the US and UK. Count yourself lucky if you can earn basis points in interest from a bank deposit or money market fund based there. A diversified South African fixed interest portfolio spread across cash, government bonds and corporate credit can still be expected to deliver a positive real return, while the same cannot be said overseas.

Sound strategy

In our fast-paced world, things change quickly and unexpectedly. On the eve of the pandemic, the five-year return on the average retail balanced fund was 4.7%, according to Morningstar. At the end of July 2021, it improved to 6.2%. Who would have thought it would get better despite the devastation of the pandemic? This is why we have the old adage of “time in the market, not timing the market”.

There is another old adage that says don’t go grocery shopping when you are hungry, since you will end up buying a lot of food (often unhealthy) you don’t need. It is similarly important to not make investment decisions in the heat of the moment when emotions are running high and we are bombarded with news. Information may be able to travel at lightning speed, but that doesn’t mean we have to respond to it. To this end, every long-term investor requires a sound investment strategy based on patience and appropriate diversification.