Springtime blues

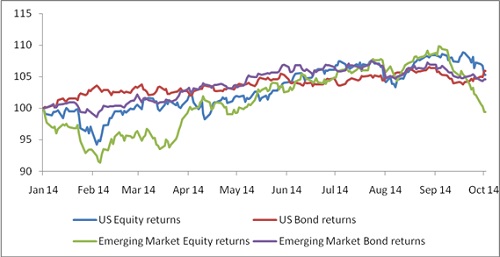

September was a very bad month for most markets and the weakness spilled over into the first few days of October. US equities, as represented by the S&P500 index, fell 1.5% in September, wiping out most of the third quarter gains. US bonds are beating equities year-to-date. In Europe, the UK FTSE 100 lost 2.9% which left its 2014 return in the negative. The Japanese equity market bucked the global trend in the third quarter, but is still catching up from a very poor first quarter.

The JSE followed global markets lower, with a 2.5% loss on the All Share index in September. The All Share also posted a negative third quarter, losing 2.1%. Year-to-date returns on the JSE are 7% (including dividends), ahead of cash, bonds and inflation. In US dollar terms, the JSE All Share index is pretty much where it started the year, and also where it was almost seven years ago.

The local market was led down by mining shares, especially gold and platinum miners. On a year-to-date basis, a significant gap has opened up between the three main JSE sectors again, with financials returning 14%, industrials 8% and resources only 4%.Listed property is now the stand-out local asset class for 2014 with a 13% total return.

Reasons behind the correction

As usual, it is a combination of factors rather than a single issue. Some commentators are quick to point to geopolitical flashpoints - the broken ceasefire in Ukraine, US and UK airstrikes in Iraq and Syria and the spread of the Ebola virus. Others argue that the abrupt departure of Bill Gross, the manager of the world’s largest bond fund, could disrupt the less liquid areas of the fixed income market. Meanwhile, China’s growth is under pressure and the ongoing protests in Hong Kong have highlighted the fact that China’s old growth model has now run out of road. Eurozone economic growth is also stalling and inflation continues to trend lower to only 0.3% (the weaker euro, at $1.26, should help a bit). The strong dollar has wreaked havoc with emerging market currencies. Emerging market equities fell more than developed markets in September. The MSCI Emerging Markets index collapsed 7.5% in the month in dollar terms, compared to the 2.8% loss of the MSCI World. Emerging market bonds have held up surprisingly well.

Finally, after a strong run on many markets, profit-taking is quite normal and healthy. This often happens in September and is ascribed, without much evidence, to the fact that Northern Hemisphere traders reassess their portfolios after returning from holiday. The truth is corrections like these cannot be predicted and long-term investors should not be alarmed.

SA haunted by the twin deficits

Apart from the above reasons, financial markets also reflect South Africa’s economic problems. The rand lost 5% against the US dollar since the beginning of September, trading around R11.30/$. While this move has been in line with the weakness of other emerging market currencies (as well as the Australian Dollar), the rand remains vulnerable. Our current account deficit of 6.2% of gross domestic product (GDP) is large by international standards, while our negative real interest rates stand out compared to our emerging market peer group (Brazil’s real interest rate is around 5%).

Due to the large current account deficit, the SARB appears to be aiming for a normalised repo rate (i.e. a repo rate exceeding inflation by some margin) before the US rate hiking cycle commences. New data released last week showed that the trade deficit, a big contributor to the current account deficit, widened to R16 billion in August due to the lagged effect of the platinum strike and surprisingly resilient imports.

The latest data on our budget deficit is also concerning, with domestic growth falling well below earlier expectations, the South African government’s finances are coming under severe pressure as tax revenue growth starts lagging projections. By the end of August, spending was growing by 10% year-on-year but revenue was only growing by 6.9%, pointing to a shortfall of around R20 billion compared to the February Budget projection. With South Africa’s sovereign debt already downgraded this year, the National Treasury is facing the daunting task of reducing the budget deficit to an acceptable size, through a combination of higher tax rates and/or spending cuts. The current size of our “twin deficits” is thus forcing the authorities to tighten monetary and fiscal policies at a time of weakening growth and an uncertain outlook for commodity prices.

Chart 1: Major global asset classes in 2014

Source: Datastream

SA Economy’s ups and downs

Local new vehicle sales data from Naamsa last week showed an 11.5% year-on-year increase, albeit from a strike-hit base last year. The third quarter as a whole also showed a healthy increase over the second quarter. Vehicle sales are a very useful indicator of credit conditions, the health of the manufacturing sector and consumer sentiment. In terms of the former, the latest FNB/BER Consumer Confidence index dropped to -1 index points in the third quarter from +4 points in the second quarter. The second quarter appears to have been an outlier, suggesting that the underlying reading of consumer confidence is still negative, with survey participants uncertain about the health of the economy and their finances.

Local manufacturing rebounding after strikes

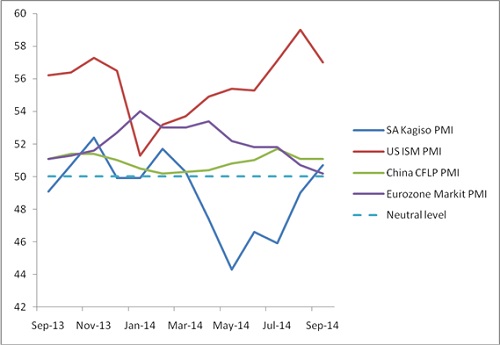

In terms of the local manufacturing sector, the September Kagiso purchasing managers index (PMI) rose back above the 50-point level that separates contraction from expansion for the first time since March. However, the 50.7 index reading is very tentatively in positive territory, mainly driven by an improvement in the business activity index. Demand remains subdued relative to inventories, suggesting limited need for new production.

Global commodity prices are plunging, including key South African exports iron ore (-40% year-to-date), platinum (-7%) and coal (-16%). Therefore manufactured exports as well as substituting imports with locally produced items - something the weak rand should help with - remains areas of potential growth and desperately needed employment creation for South Africa (new StatsSA data shows the private sector only created a net 12 000 jobs in the second quarter; the manufacturing sector shed jobs). Sourcing new export contracts takes time and strikes, electricity shortages and other bottlenecks don’t help. There are tentative signs of this happening, but for it to continue, we also need our trading partners to post decent growth rates.

Global manufacturing generally softer

In terms of international manufacturing, the JPMorgan Global PMI, covering some 90% of global manufacturing activity, fell to a four-month low in September, but remains comfortably above 50 points. On a country or regional level, the US ISM index remained solidly in positive territory at 57 index points in September, however this was down from a four-year high of 59 in August.

The Eurozone PMI manufacturing slowed to 50.3 in September, with new orders contracting for the first time since June 2013. Worryingly, the two biggest economies in the bloc, Germany and France, are both in negative territory. Japan’s PMI was also slightly lower in September, but at 51.7 points remains positive after a sharp contraction immediately after the April tax hike.

China’s official PMI, which focuses on larger state-controlled firms, held steady at 51.1. The HSBC manufacturing PMI, which focuses on privately owned firms, was 50.2 in September, barely above stagnation territory. China’s 7.5% annual growth target is at risk, with all the signs pointing to lower domestic demand amid rising industrial overcapacity and a property market that is experiencing price declines (though exports to the US are growing nicely). The question is whether authorities in Beijing will allow the economy to slow for the necessary process of rebalancing to take place, or whether they will try to stimulate economic activity through monetary policy, as they’ve done on previous occasions when in danger of missing the growth target. Beijing has eased mortgage lending restrictions for the first time since 2008 last week – second-home buyers only need to put down a 30% deposit, instead of 60% - but has stopped short of cutting interest rates or banks’ reserve ratio requirements.

Chart 2: global purchasing manager’s indices

Source: Datastream, Markit