“Something’s out there” – A case for externalising your investments from SA

Luke McMahon, Research and Investment Analyst at Glacier by Sanlam.

South Africa accounts for approximately only 1.50% of total world market capitalisation. The US alone comprises more than 50% of the world’s free-float stock market capitalisation, followed by countries such as China, Japan and the United Kingdom.

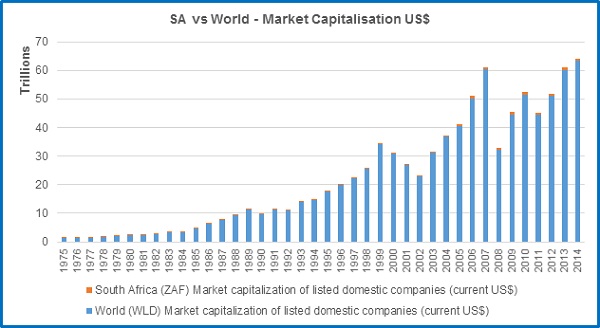

According to Singh (2015), if you only invest locally, you deny yourself the opportunity to invest in those companies that have an international footprint and could generate substantial profits for investors across different economies and markets. By allocating a portion of investments offshore, one could spread the risk, and enhance the possibility of generating better returns by diversifying. It also gives an investor access to sectors that would not readily be available on the JSE. Having said that, data from the World Bank (Figure 1.) shows that SA’s equity market represents but a small fraction of total world market capital.

Figure 1.

Source. data.worldbank.org

Although the graph above shows the value of SA market capitalisation to be growing in relation to world market capitalisation, one needs to be cognisant of the inherent risks that accompany investing in the SA financial market.

Inherent risks in SA’s financial market environment

When it comes to evaluating the state of SA’s financial market it is not difficult to stumble upon a myriad of factors that create significant headwinds for local investors. According to a survey of 620 SA risk management experts, conducted by IRMSA (2015), the top 10 sovereign risks that are likely facing SA are: 1) Corruption; 2) High unemployment; 3) Shortfall of critical infrastructure; 4) Profound political and social instability; 5) Major escalation of organised crime; 6) Escalation of cyber-attacks; 7) Failure of a major financial mechanism or institution; 8) Severe income disparity; 9) Mismanaged Urbanisation; 10) Massive incidents of data fraud. In addition to these factors, the situation is worsened by harmful economic factors such as elevated levels of inflation, which erode the nominal value of local investments quicker, and the prolonged devaluation of the country’s currency. As a result of this SA’s GDP per Capita (PPP) is currently $12390 p.a., whereas the US GDP per Capita (PPP) is currently approximately four times that at $52549 p.a. Hence the purchasing power of SA citizens is significantly weak in global terms. The case is therefore strong for SA investors to externalise a portion of their investments offshore in order to keep up with global standards.

Benefits of investing offshore

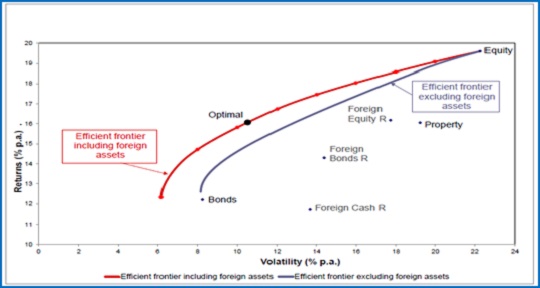

With increased systemic risk in the local SA economy thanks to political debacles, government inefficiencies, volatile market movements, sovereign credit downgrades, devastating drought conditions and significant rand depreciation, offshore investing remains high on the agenda for many SA investors (Cairns, 2015). One way of mitigating these systemic risks is by investing assets abroad and diversifying exposure to a single country. Academically the rationale behind this is compelling and investment industry professionals encourage an investment strategy which has a serious focus on international investing over the long term (Cairns, 2015; Paine, 2016). Therefore diversification of risk is the main benefit a local investor can derive from allocating a portion of their investments abroad as demonstrated from the graph below.

Figure 2.

Source. Bradfield & Munro (2015)

It is quite evident from the figure above that the inclusion of foreign assets significantly shifts the efficient frontier to the left, i.e. the volatility (risk) is reduced and shifts the frontier upward, i.e. returns are enhanced.

What are prominent asset managers saying about offshore investment environments?

Glacier Research’s Bull & Bear Report collates the performance expectations of leading South African Asset Managers (seven participants) over the coming 12 months. Asset Managers are asked to comment on expected performance for various asset classes and index sectors; currency levels; commodity prices and the performance of selected global markets. These viewpoints are subject to change in line with changes in economic and market conditions. Some of the latest findings are given below.

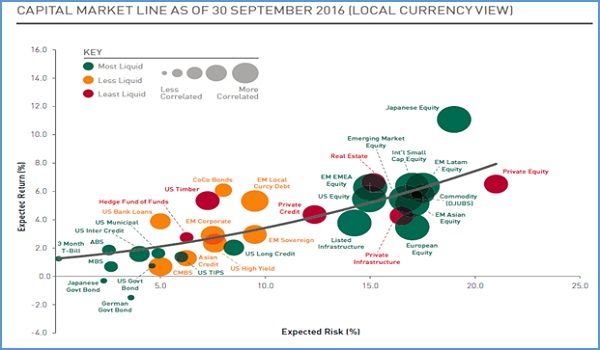

Also, a prominent globally-based asset manager is seeing good value in offshore markets. Assets that seem attractive are situated above the capital market line (Figure 4). Also the most liquid stocks available are found in developed markets, such as in the US and Japan. Emerging market equity has also shown strong performance over the last year.

Figure 3. Capital Market Line (Global)

Source. Pinebridge Investments

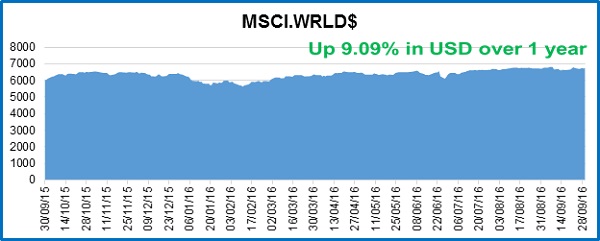

An illustration of an investment that would take these major global equity markets into account is provided in figure 3 below. The MSCI World Index currently comprises US equity (59.28%); Japanese Equity (9.18%); UK equity (6.63%), French equity (3.67%), Canadian equity (3.62%) and other (17.62%). An investor (local) that had simply externalised their investment into US dollars and passively invested in the MSCI World Index would have returned over 9% over the last year.

Figure 4. MSCI World Index

Data Source. I-NET

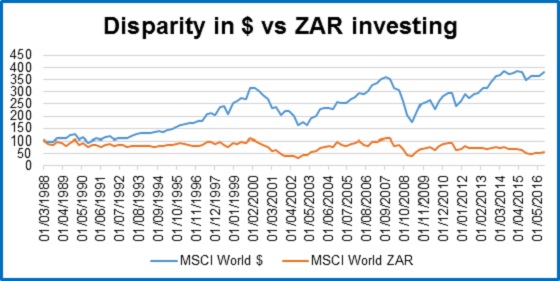

If this is put in further context, taking into account a US dollar or ZAR investor, one can begin to see the negative effects (severe rand depreciation and sovereign risk) that SA’s investment environment would have on a ZAR investor. Figure 4 below provides a comparison of an equal investment in the MSCI World Index over the last twenty-eight years. It is clear a rand-denominated offshore investment in this case would have struggled significantly, hence making the case for expatriating funds offshore.

Figure 5. MSCI World Index - $ vs ZAR

Data Source. I-NET

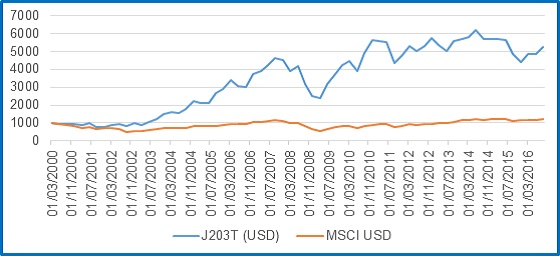

However, as a side-note it should be borne in mind that an investor would nonetheless also be able to achieve significant value in the local SA market. Playing’s devil’s advocate (Figure 6.), one can see that the South African (JSE All Share) market outperformed the MSCI World Index in USD terms over the last sixteen years.

Figure 6. MSCI World Index vs JSE (203) in $ terms

Data Source. I-NET

Although, this is not to say that SA’s market would continue to outperform, especially since the JSE is currently trading at a P/E ratio of 23, which is well above its fifty-year average mean of 16. This suggests the local market is highly overvalued. In light of this and the fact that SA’s economic growth outlook seems dismal, earnings will unlikely catch up to price in the short term. This could potentially see a price-rating occur and cause the level of the JSE All Share to decline as investors sell, based on a depressed earnings growth outlook for SA companies. Having said this, we should then consider an offshore investment as a viable alternative or diversifier of this risk should this phenomenon take place.

Offshore asset management perspective

When one compares the local asset management industry in South Africa with global peers, the statistics show that SA is significantly ranked lower than global peers. This is largely due to the fact that the asset management industry in developed markets is significantly more mature.

Figure 7. Top Global Asset Centres: June 2016

Source: IPE Research

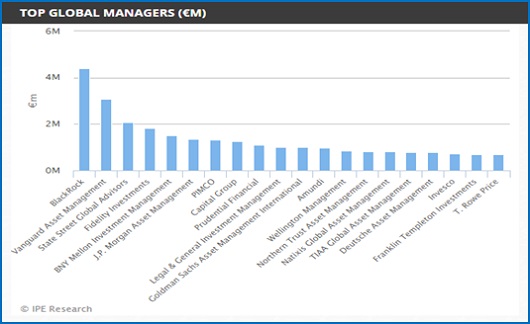

Figure 8. Top Global Managers

Source: IPE Research

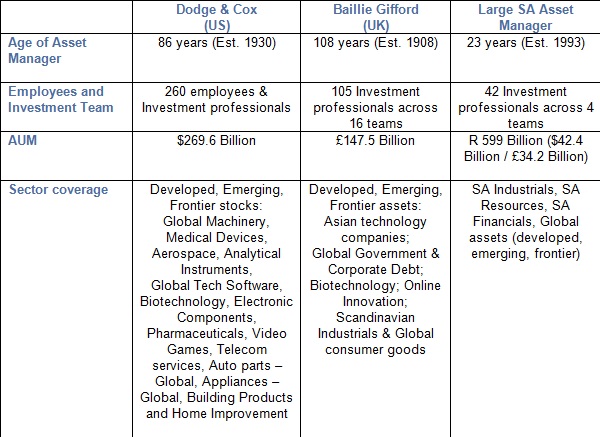

When one compares the local asset management capability (Table. 1) in South Africa with global peers, the statistics show that SA asset managers are slightly more constrained in their asset management capability and experience than global peers.

Global Asset Managers vs Top SA Asset Manager

Table 1. Global Asset Managers vs SA Asset Manager

Conclusion

In order to maximise investment potential it may be prudent for investors to adopt an approach whereby they “think globally, but act locally”. Being concentrated and over exposed to just one market is rarely going to produce the optimal risk-reward results that one would hope for in an investment. Empirical evidence has shown that a long-term, well-diversified international portfolio can help mitigate unnecessary risk and at the same time offer opportunities for enhanced returns. This research segment has shown that by investing offshore one can exploit international currency and interest rates and diversify against local sovereign risk across various countries, regions and economies. It allows a local investor an opportunity to invest in different countries at different growth cycles and also choose from a wider selection of industries and sectors which are not readily available in SA’s financial market. Finally, increased investment opportunities are created by allowing a local investor access to a wider range of top global asset managers which demonstrate superior investment capabilities than most SA asset managers.

References:

Cairns, P. (2015) - What’s the best way to invest offshore? Moneyweb, February, 2015. Web: http://www.moneyweb.co.za/investing/offshore-investing/whats-the-best-way-to-invest-offshore/ - accessed: 10/03/2016

IRMSA. (2015). IRMSA Risk Report – South Africa Risks 2015. The Institute of Risk Management. South Africa.

Kennedy, L. (2016). Top 400 Asset Managers 2016: Global assets now €56.3trn. Investment & Pensions Europe. Web: https://www.ipe.com/reports/special-reports/top-400-asset-managers/top-400-asset-managers-2016-global-assets-now-563trn/10013542.fullarticle (Accessed – 24/11/2016).

Paine, C. (2016) - Investing offshore as a South African – Why, How & Where? Fin24, January, 2016. Web: http://www.fin24.com/BizNews/investing-offshore-as-a-south-african-why-how-where-20160115 - accessed: 11/03/2016

Singh, A. (2015). Why you should consider investing offshore. Old Mutual. Private Wealth Management. Web: https://www.oldmutual.co.za/docs/default-source/personal-solutions/financial-planning/pricate-wealth-management/articles-and-newsletters/why-invest-offshore-article.pdf?sfvrsn=0 (Accessed – 24/11/2016).