Some key uncertainties from last year will continue to drive markets in 2026

Despite plenty of volatility, 2025 delivered strong returns to investors. With the benefit of hindsight, few things dominated headlines to the same extent as US President Donald Trump and artificial intelligence (AI) mania.

Both had an outsized impact on the investor experience, and we saw markets becoming increasingly concentrated during the year, raising particular concerns for investors. Looking ahead into 2026, the key challenge will remain finding opportunities trading at reasonable long-term valuations and not overpaying for assets.

Trump policy was a key driver of markets in 2025

Whether it is through his market moving tweets or trade policy interventions reshaping the global world order, there can be little doubt that US President Donald Trump loomed large on the investor landscape last year. It remains to be seen whether his policies will have a positive or negative outcome for the US economy over the medium-to-longer term. Below are some key developments that impacted markets during the year.

• The ever-growing US debt pile:?US debt grew to over US$ 38 trillion in October 2025, raising concerns about the sustainability of the US fiscal trajectory.

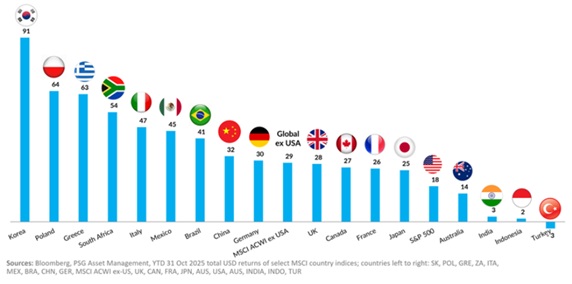

• Tariffs and US dollar weakness:?‘America First’ trade policy, growing debt concerns and a rethink of US exceptionalism weighed on the US dollar, with the Dollar Index (DXY) down 10% for the year to 31 December 2025). A weaker dollar has also made returns from non-US dollar denominated assets appear more attractive on a relative basis, and after many years of underperforming the US markets, we have seen emerging bull markets outside the US.

EMs and China: Bull markets emerging outside the US

• Attacks on the US Federal Reserve (Fed):?Donald Trump has not made any secret about his disdain for Federal Reserve Chair Jerome Powell, who is set to retire in May this year, and who has recently become the subject of a criminal investigation. Last year, President Trump sought to bring criminal charges against Federal Reserve Governor Lisa Cook. Currently, prediction markets put Kevin Hasset (who is highly sympathetic towards Trump’s policies) in the lead to be nominated as Federal Reserve Chairman.

• Gold:?Up over 62% for the year in 2025 and continuing to build on 2024’s strong performance in response to fears around inflation and US dollar weakness.

We are only a few weeks into the new year, and President Trump has already been flexing his military muscles. This provides an indication that we may see more policy changes emanating from the US this year.

Surviving the ‘everything AI’ rally (or bubble?)

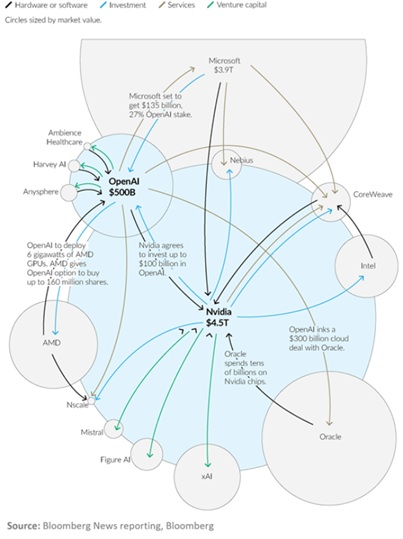

In October 2025, Nvidia became the world’s first US$5 trillion company. Although AI exuberance has continued to drive stock markets, late October marked something of a ‘sentiment shift’ as investors started questioning the circular nature of various deals and became concerned about a move away from funding AI capex from free cash flow to using debt financing instead.

• How Nvidia and OpenAI fuel the AI money machine

OpenAI has done deals totalling nearly US$1.5 trillion with various suppliers of processing power, but only generated an estimated US$12 billion of revenue for the year, and recorded a quarterly loss of US$12 billion.

• Uncertainty about who will benefit from AI:?The AI boom has captured the public imagination, but while it seems clear that the technology has transformative potential, it is far less clear who will be the winners from this going forward. Research by Nobel Laureate William Nordhaus analysed the impact of innovations between 1948 and 2001 on US markets, and found that only 2.2% of the surplus went to the innovators, while nearly 98% accrued to society as a whole.

• Questions about who will fund future capex:?The hyperscalers (companies that run large cloud-based data centres), may have deep pockets, but they do not have unlimited cash flows, and are increasingly turning to debt to fund investment in AI infrastructure. Oracle has been a leader in funding AI capex with debt, and saw its credit default swap (CDS) spreads ramp up sharply towards the end of the year.

While it is easy to get caught up in the hype surrounding AI, it is far from clear who the ultimate beneficiaries of and winners from the AI revolution will be. Investors will be well-served to remember that the price paid for an investment, remain one of the key drivers of outcomes achieved.

Market concentration

AI hype and the American exceptionalism narrative have driven markets to unprecedented levels of market concentration. In the past, aligning closely to an index was often viewed as a way to mitigate risk, especially since the index so often serves as a benchmark for funds. The diversification benefits many believe indices offer, are eroded as markets become increasingly concentrated. This means that many investors are inadvertently taking on more risk than they might realise (read more about this in?The hidden risks of hugging an index), and that investors need to take care to ensure portfolios are suitably diversified.

Looking ahead in 2026

Plotting an investment course for the year ahead can be tricky when the investment environment is undergoing deep-seated changes that will fundamentally impact where returns originate from in the future. While no-one knows what this landscape will ultimately look like, we believe that it is especially important to ensure that you don’t overpay for assets at this critical juncture.

That is why it is important to partner with a manager who has a proven track record of navigating a variety of investment environments and who focuses on independent and in-depth research, aimed at uncovering opportunities suited to an evolving environment rather than simply replicating a benchmark. At PSG Asset Management, our proven?3M investment process?leads us to invest in overlooked assets that are trading at a discount to their intrinsic value. This approach has proven successful in the past, and we are confident that it will continue to reward our investors handsomely into the future.