Some FOMO stocks to buy

FOMO (noun): Family-Owned and influenced or Management-Owned business.

FOMO businesses represent the majority of businesses in most industrialised economies. Adrian Saville, CIO of Cannon Asset Managers, finds some stocks that should be on your shopping list.

As part of our constant search for good investments, we always try to identify attributes of shares that repeatedly deliver better-than-market results. Some of the attributes that work are self evident. The most obvious is attractive prices based on the reality that, no matter what price an investment is sold at, you are never afforded the opportunity to go back and change the purchase price. Put simply, the price you pay for any investment is a primary determinant of your long-term return. We spend an equal amount of time looking at business and industry quality, a second key component in determining investment returns. As Buffett puts it: “When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”

But aside from price and quality, what about other, less obvious, factors?

One such desirable attribute are FOMO businesses. These are not stocks you rush out to buy because of “fear of missing out” on a hot tip that everyone is talking about at dinner parties – we’d seldom recommend that strategy. Rather, FOMOs are family-owned and influenced or management-owned businesses.

As our acronym suggests, a FOMO business exists where:

• The founder, or founding family, owns a meaningful share of the enterprise or has significant influence on the running of the business; or

• Key management has a large shareholding in the business.

Academic research varies in what defines a family- or management-owned or influenced business, allowing ownership to range from as little as a 10% minimum to as high as 50%; and there is also disagreement as to the level of board representation that is required to constitute “influence”. Cannon uses a more broad qualitative assessment of what defines a FOMO business.

Regardless of the exact definition adopted, FOMO companies represent the majority of businesses in most industrialised economies. However, as companies migrate from the unlisted environment to formal exchanges, the FOMO nature does not carry over to stock exchanges. Firms tend to become bigger, making family or management ownership financially more onerous and, by prescription, a business that migrates onto a formal exchange will issue equity to “outside” parties such as large investment institutions.

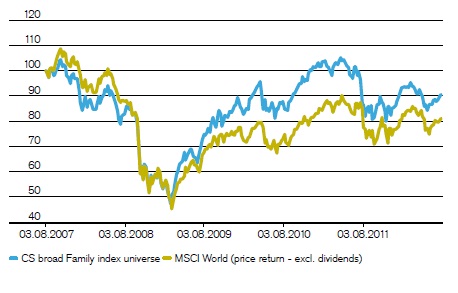

This dilution in the FOMO footprint is unfortunate, because FOMO firms generally tend to perform very well over time and, in the aggregate, much better than the market (see Figure 1 where Credit Suisse has created a Family Index versus the MSCI World Index).

Figure 1: Credit Suisse Family Index versus MSCI World

The reasons for FOMO businesses performing so well can be traced back to the work of Berle and Means (1932), who recognised that separating ownership from control of a company ushers in the so-called principal-agent problem. Under the principal-agent problem, the benefits of a FOMO firm are missing. The advantages that exist where ownership and management are the same include:

• A longer-term horizon in the business;

• Management is less likely to act selfishly in their own best interest at the expense of shareholders; and

• Greater concentration and focus on core businesses and inherent competitive strengths.

Despite some of the obvious risks to FOMO businesses, such as the family entrenching bad management, the use of elaborate control schemes or abuse of power at the expense of non-insider shareholders, the overwhelming evidence is that FOMO businesses outperform over time.

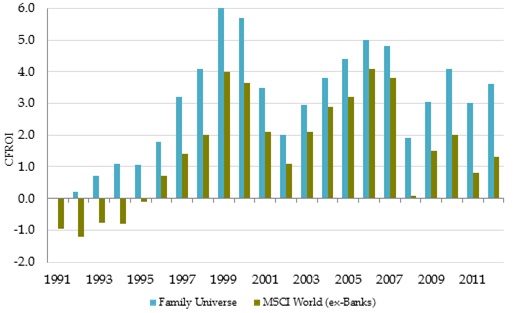

In fact, the family or management shareholders in FOMO firms act more like private equity players in terms of horizon, management guidance, corporate focus and value creation for shareholders. One way to measure this success is to consider the cash flow return on investment (CFROI) of FOMO businesses versus the market. (CFROI indicates the value of a company's capital investments in terms of how effectively those investments produce and generate profit – represented by cash flow – relative to the costs they incur.) Figure 2 below clearly demonstrates the sustained superior CFROI of FOMO companies compared to the MSCI World Index (ex-Banks).

Figure 2: Family Business CFROI versus MSCI World (ex-Banks) CFROI

For those interested in investing in FOMO businesses, some examples are:

Examples of South African FOMO Firms Examples of Global FOMO Firms

Altech FamousBrands AP Moller-MaerskJardine Matheson

ARB Grindrod Berkshire KSB

ARM HCI BMW L’Oreal

Aspen ISA Carrefour McGraw-Hill

Assore Net1 Dangote Microsoft

Atron Onelogix Dell Nike

Bell Peregrine Equity Bank Oracle

Bidvest Pick n Pay Estee Lauder Reliance Industries

Blue Label Pinnacle Tech Google Roche

Bowler Remgro Hermes Samsung

Crookes Richemont Holcim SAP AG

Conduit Royal Bafokeng Hornbach Thyssen Krupp

Datatec Sasfin Inditex (Zara) Walmart

Datacentrix Transpaco Investor AB

ELB Trencor

EOH Value

Exxaro

Note: The shares in bold are owned by Cannon Asset Managers in various portfolios

In our houseview global equity portfolio, 14.3% of the portfolio is invested in FOMO firms, while domestic portfolios are about one-third invested in FOMO stocks, which is substantially higher than the overall figure for the JSE of around 11%.

The attractive attributes of family-owned or influenced businesses, when combined with value multiples and other quality factors, is a powerful and desirable combination. There are some FOMO stocks that are definitely worth owning, and not for flavour of the month reasons.