Sleep easy: take a dose of absolute return to manage your investment insomnia

As we head into the remainder of 2022, the major question for fund managers is how to allocate investors’ capital in a macroeconomic environment that appears to be screaming “caution” due to the considerations below.

Fernando Durrell, an Absolute Return portfolio manager at Sanlam Investment Management (SIM*), says, “We are acutely aware of the implications of higher inflation and rising interest rates on risky assets. Moreover, geopolitical tensions (including the war in Ukraine), uncertainty around further regulatory changes in China and still expensive (in our view) US equities, add to our cautious stance. Rising interest rate environments (or more generally, reduction-in-liquidity environments) have historically been those in which capital protection is key, giving fund managers the best opportunity to achieve clients’ longer-term targets, when these challenging environments pass.

“In the current environment, we still like South African equities and prefer emerging market over developed market equities,” said Durrell, adding that he believes that many asset managers were unlikely to max out the Regulation 28 offshore limit, which was recently increased to 45%.

Investors in absolute return (AR) funds have weathered recent market volatility thanks to active fund management decisions taken to minimise the impact of short-term market fluctuations on their capital values. Durrell says that active managers had an advantage over static asset allocators in navigating equity market drawdowns (and thus avoiding negative return), because they implement their tactical, shorter-term asset allocation views as needed.

Tactical asset allocation adjustments are made to ensure that a fund has an optimal exposure to cash, bonds and equities (including listed property), both domestically and offshore, to achieve its stated return target, while reducing potential downside risks.

In the case of the SIM* Medium Equity Fund, the mandate and approach is to deliver CPI +5% (after fees) over a rolling three-year period, with less volatility and drawdowns than a multi-asset high or pure equity fund, resulting in smooth, positive returns over the longer term. “The key promise in our mandate is to deliver an inflation plus return without causing unnecessary anxiety to investors during market corrections,” said Durrell.

The SIM* Absolute Return funds look to increase exposure to inflation-linked bonds, but these instruments are expensively priced at present; they are thus waiting for better buying opportunities in this segment. As for listed property, the manager maintains a preference for more diversified offshore property exposure as opposed to a more concentrated domestic sector. Local property companies continue to struggle to normalise following the pandemic-induced lockdowns, including high vacancies and negative rental reversions. “Since we experienced drawdowns in domestic property in 2020, and before that in 2018, our preference is to avoid the undesirable risk characteristics of this asset class, hence we remain underweight,” said Durrell.

Using the maximum offshore allowance in a cautious fund such as the SIM* Inflation Plus fund, which has a CPI+4% return mandate (after fees), would result in taking on far too much currency risk. It would also mean missing out on attractively priced SA government bonds that are yielding as much as 11% in nominal terms presently. Added to this, assuming 6% domestic inflation, these bonds are expected to deliver a 5% real return with much lower risk when compared to equities. Developed market bonds meanwhile, despite the recent rise in these yields, still offer virtually guaranteed negative real yields to maturity. This explains the SIM* Absolute Return team’s minimal exposure to offshore government bonds, preferring offshore equities and the dollar-denominated bonds of SA corporates instead,” said Durrell.

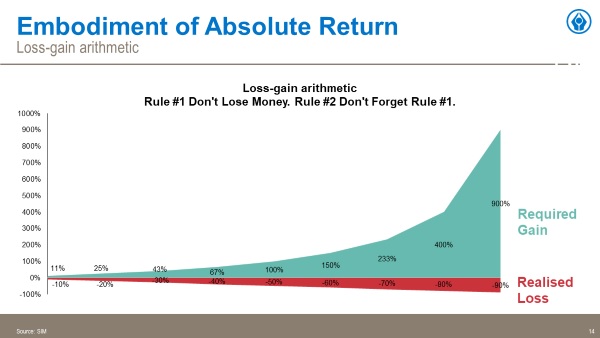

The importance of not experiencing negative returns is depicted in the Figure 1 below. For every loss of a particular percentage, an investor needs to generate a corresponding positive return that is an order-of-magnitude greater than the loss, just to get back to where the investor initially was, let alone the growth that was missed out on. So, if one’s portfolio loses say 10%, then it has to make +11% to break even; a loss of 30% requires a gain of +43%, and a loss of 50% requires a return of +100% to get back to its original value.

Figure 1: Importance of minimising drawdowns (or negative returns). Source: SIM*, May 2022

Durrell commented on the extreme volatility exhibited across asset classes prior to, and during, the pandemic correction of 2020. An obvious example is that of the tech-heavy Nasdaq index, which fell 30% from its pre-pandemic high to its 20 March 2020 low, before staging a staggering 90% rally by the end of that year. It rewarded investors with another 25% between January and mid-November 2021, with many ups and downs along the way, before correcting 20% between mid-November 2021 and mid-March 2022.

“Our job is to manage returns without taking investors on a rollercoaster ride, and we do that by being very selective about how we invest clients’ funds across various asset classes,” said Durrell. “In our case, allocations to asset classes must reflect appropriate risk appetite subject to limits including Regulation 28 (of the Pension Funds Act) and ASISA (The Association for Savings and Investment South Africa), inter alia.” Regulation 28 for instance, introduces maximum allocations on total equity exposure and offshore assets, and ASISA provides various limitations within its defined fund categories.

The way forward in 2022

The funds’ tactical positioning for the remainder of 2022 favours equities over bonds over cash, with the outlook for local equities edging out offshore equities. “We still expect solid returns from local equities, which explains our preference for these over bonds. Despite the increase in local cash rates, we maintain a preference for bonds over cash domestically. Our ranking of offshore asset classes is consistent with that of domestic ones,” concluded Durrell.

“Our portfolios are still structured for an optimal combination of return and risk, with about 50% exposure to fixed income and cash, and the balance to risky assets, including offshore assets. We believe this will provide our investors with solid potential upside performance, but without them having to lose sleep over unexpected downside shocks.”