Short-term uncertainty versus long-term certainty

Roné Swanepoel, Business Development Manager at Morningstar Investment Management SA

The danger of letting short-term market moves drive your decisions

“If I ask you what’s the risk in investing, you would answer the risk of losing money. But there actually are two risks in investing: One is to lose money and the other is to miss an opportunity. You can eliminate either one, but you can’t eliminate both at the same time.” – Howard Marks

During January we saw a healthy rebound in asset prices as inflation numbers globally started to ease, China began reopening and Europe seemed to be more resilient than what the market initially expected. Fast forward to March when the world was faced with a wave of headlines about the biggest US bank failure since the global financial crisis, a takeover of Switzerland’s second-largest bank and the possible contagion to the rest of the markets.

Volatility is once again on the rise, with markets suffering a few large down days in the latter part of March. The S&P 500 has faced a daily decline greater than 1% for 16 days year-to-date and the All-Share Index (ALSI) has seen 15 days - both on track to exceed more than the average year. Coupled with this, the Volatility Index ($VIX) rose above 30 on 13 March for the first time since October 2022, signalling increased fear and uncertainty.

The stock market has quickly, and once again, reminded us that one of the few certainties in markets is that there will always be uncertainty.

Most investors claim to be unphased by uncertainty but in reality, we all strongly dislike the possibility of losing money. When we think about our behavioural biases this fits into the “loss aversion bias”. In short, loss aversion means that we feel the pain of losing about twice as much as the pleasure of gaining in the markets. It’s one of the reasons that negative headlines seem to make more sense when uncertainty is everywhere.

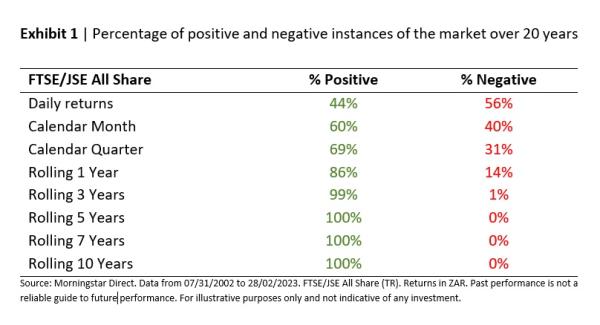

It is, however, very important to put these feelings in the right long-term perspective. The graph below shows the percentage of times the local market has been in positive territory over various time periods as well as the percentage of times the market has been in negative territory over the same periods.

If we consider these different periods for the All-Share Index (ALSI), we can see that daily returns in the market are (more or less) a 50/50 occurrence. Since we know that being loss averse means that losses (or negative periods) make us feel twice as bad as gains make us feel good, it simply means that if you look at the value of your investment portfolios daily, you will feel bad just about every single day. Any positive sentiment gained from the returns received will get completely wiped out by the terrible feeling created by the down days.

If we lengthen the time horizon to just three years, the effects of loss aversion slowly start to fade and the market is positive on a rolling three-year basis almost 100% of the time since 2002.

Loss aversion can have a big impact on our behaviour

A mistake investors frequently make is paying too much attention to our investment portfolio moves over the short term. The more frequently we look at our investment portfolio, the more likely we are going to see losses and, in turn, the likelihood increases of suffering from loss aversion.

With a wealth of information so readily available, it’s extremely hard not to pay attention. However, for most of us, our most meaningful investment milestones are years away and it is a good reminder that paying too much attention to those daily moves can put us at risk of missing our goals that are years away.

Investing is a long-term pursuit

Consistent, top-quartile performance over the long term to match your investment objectives should be the main goal when assessing your investment portfolio. Focussing too much attention on the short-term market moves can only lead to stress and future pain from chasing the wrong types of investments.

So, when you find yourself worrying about the uncertainty and volatility in markets, reach out to your financial adviser and ask yourself these questions:

1. What sources am I using for my financial advice? Is it my financial adviser or news and social media headlines?

2. Has the market volatility and uncertainty changed my time horizon or investment goals?

3. Has my risk tolerance changed?

4. Have my circumstances changed?

Building a strong portfolio foundation is one of the most important things you can do to maximise your odds of investment success. That means setting an asset allocation appropriate for your risk tolerance and making sure your portfolio is cost-effective, broadly diversified and that you invest for the long term.

It’s hard to predict when the market will make these big moves. So, it’s best to find an allocation that lets you sleep at night and stick with it. Uncertainty is a certainty, so don’t get caught off guard by it.