Shifting global dynamics still support the rand

Dave Mohr, Chief Investment Strategist at Old Mutual.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

After a record 63 days without a 1% decline, the benchmark US S&P500 equity index finally hit a wobble last week. After such a long winning stretch, a correction was inevitable. The catalyst appears to have been doubts over President Trump’s ability to deliver on his stated aims of cutting taxes and upgrading infrastructure, following his failure to convince the Republican Party to unite behind healthcare reform (and this is apart from the other controversies swirling around his presidency). Equity markets rallied after his surprise election in November, betting that lower taxes and more spending would boost company profits. The trailing price: earnings ratio on the S&P500 jumped from 19.6 to 22.3, an indication of increased investor optimism.

Apart from the equity market’s rethink of the “Trump trade”, the bond market had doubts about the prospects of sustained higher inflation. Bonds sold off initially after the Trump election, but have been trading in a narrow range since the start of the year. Here the catalyst has been a “dovish hike” from the US Federal Reserve, a weaker oil price, and depressed inflation expectations. The yield on the benchmark 10-year government bond fell to 2.4% from 2.6% prior to the Fed’s hike. Much of the big increase in headline inflation in the developed world is due to the oil price. Core inflation rates, which exclude volatile food and fuel prices, are increasing much more slowly in the US while being stuck below 1% in the Eurozone. In January, the year-on-year change in the dollar oil price was 91%. However, it now sits at 31% and will reach 0% in July if the current price holds.

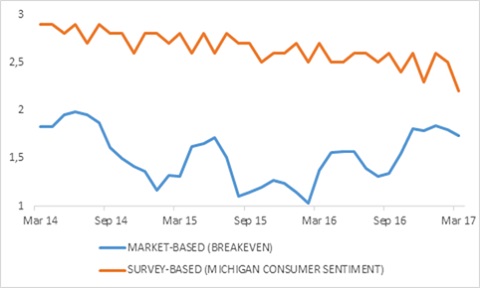

Expected inflation matters as ultimately, price and wage setting is a function of what people anticipate future inflation will be. Expected inflation can become actual inflation. Inflation expectations can be measured by looking at the difference between bond yields and inflation-linked bond yields (so-called breakeven inflation), or it can be measured through surveys. Chart one shows how both measures of expected inflation over five years have pulled back.

Stronger rand

How does this impact South Africa? Most importantly, as at Friday, 24 March 2017, the rand strengthened to the strongest level against the US dollar since July 2015 as the greenback pulled back.

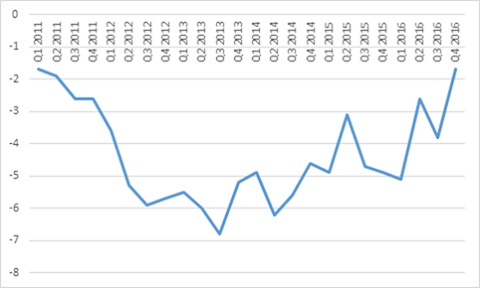

The rand was further supported by SA Reserve Bank data showing the current account deficit narrowing to 1.7% of GDP in the fourth quarter from 3.8% in the third quarter (or from R166 billion to R76 billion). The 2016 deficit was 3.3%, down from 4.4% in 2015. A large current account deficit has to be funded by foreign capital, and potentially leaves the exchange rate vulnerable. The smaller deficit implies a reduced vulnerability to capital flight, and will be a factor when ratings agencies review our sovereign rating mid-year.

There are two main components to the current account – the trade balance and the service and income balance. The trade balance has benefited from stronger commodity prices and a pick-up in mining export volumes (mainly iron ore and coal). The value of imports also declined during the quarter due to sluggish domestic demand and a firmer rand. The fourth quarter saw a R56 billion trade surplus, compared to a R7 billion deficit in the third quarter. South Africa’s terms of trade – export prices relative to import prices – improved substantially throughout 2016.

The deficit on the services and income account tends to be stickier (between 3% and 4% of GDP) since it reflects the cost of South Africa doing business with the rest of the world, as well as the fact that foreigners are significant holders of local bonds and equities, and therefore persistently repatriate large amounts of interest and dividends. However, as domestic growth has slowed, dividend payments have dwindled, while South African ownership of foreign companies has increased over the past few years, resulting in more dividends flowing our way. It remains to be seen whether this trend will hold. Stronger domestic growth could lead to more dividends being paid, while the stronger rand could result in South African investors and businesses deciding to keep their foreign dividends abroad while they wait for a more favourable exchange rate.

Inflation outlook still improving

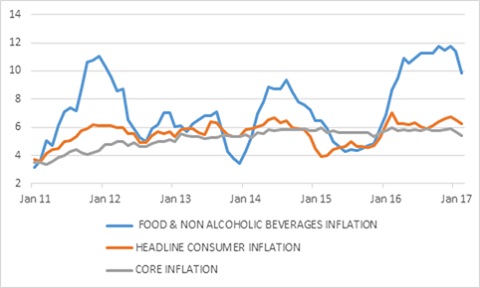

The combination of a stronger rand and softer oil price is positive for the inflation outlook. Food inflation has also turned. Consumer inflation slowed to 6.3% year-on-year in February, with food inflation declining to 10%. Meat is the only main food item whose inflation rate is still increasing; the other items (vegetables, dairy and grain products) are experiencing much slower inflation than a year ago. At the producer level, prices are falling, which should feed into further declines in consumer food inflation.

Core inflation, which excludes volatile food and fuel prices, declined to 5.2% year-on-year in February. Many of the core items are rand-sensitive, and are starting to show the effects of the stronger rand.

All this bodes well for the interest rate outlook. Forward Rate Agreements (FRAs) are already pricing in interest rate cuts in the fourth quarter, and the government’s benchmark R186 bond yield has declined to 8.4% last week, the lowest level since August last year (lower yields, which reflect expectations for lower interest rates, imply bond prices have increased). Bond yields are still attractively high in real terms and compared to what is available globally.

Reserve Bank reluctant to cut

However, the Reserve Bank has made it clear that the bar for rate cuts remains high. More specifically, it is not enough for inflation to move within the 3% to 6% target range, but inflation expectations must also move deeper into the target range. Currently, surveyed inflation expectations are close to 6%. Breakeven inflation rates for periods longer than six years are still above 6%. The Reserve Bank wants consumers, unions and investors to believe that it will keep inflation within the target range over time, since that is the purpose of inflation targeting. Therefore, it is unlikely to be in a hurry with rate cuts, but it might start by softening its generally hawkish tone at this week’s Monetary Policy Committee (MPC) meeting. If rates do decline, it will support consumer spending. Households spend on average 9.5% of disposable income on making interest payments.

Where does this leave investors? The local equity market takes direction from global markets, which in turn tend to follow the US. Investors appear to have been overly optimistic on the prospects for US stock. However, history shows that the US market only experiences a major bear market when the economy enters a recession (corrections are common and unpredictable) and the US economy is doing quite well at the moment. Trump policies or not: industrial activity is picking up, the housing market is still quite strong, unemployment is declining and confidence is high.

For emerging markets it is a case of pessimism fading. Like South Africa, other emerging markets are benefiting from stronger currencies, lower inflation, a declining interest rate outlook and better expected economic growth. This combination is increasingly attractive. Data from JPMorgan shows that capital flows into emerging market equity and bond markets had the best start to a calendar year since 2013, and year-to-date flows already exceed the total flow for three of the past four years.

However, certain JSE-listed companies might struggle, given significant increases in global exposure over the past five years, turning the strong rand into a headwind, instead of a tailwind. Since the rand is historically volatile and unpredictable, appropriate diversification across asset classes and within asset classes remains key.

Chart 1: US expected inflation over five years, %

Source: Datastream

Chart 2: South African consumer inflation

Source: StatsSA

Chart 3: South African current account balance, % of GDP (negative value indicates deficit)

Source: SA Reserve Bank