Setting the stage for lower rates

For local investors, the main event of the past week was not the State of the Nation Address (SONA), though we will touch on it below. The main event happened thousands of miles away in Washington DC, when a man few South Africans have heard of said “we will act as appropriate to sustain the expansion”. With those words, Jerome Powell, Chair of the US Federal Reserve (the Fed), joined a growing number of central bankers who have cut or are expected to cut interest rates. The Fed, which as recently as December hiked its key policy interest rate, now falls in the latter camp. The expansion he referred to turned 10 years old this month, the longest in US recorded history. (Other countries have had longer expansions, with Australia holding the record of 28 years without recession.) But it has also been one of the slowest and dullest on record, without most of the usual excesses that build up during good times and eventually cause a recession and post-recession hangover.

Prevention is better than cure

So where does the Fed’s U-turn come from? The US economy is still in pretty good health, even though job growth has cooled and business investment is soft. It is expected to grow around 2% this year. That is down from last year’s tax cut-fuelled 3% rate of growth, but in line with the average growth rate since the Great Recession. The Fed’s concerns are threefold: inflation remains below its 2% target, and has in fact declined in recent months, raising the risk that people will start to believe that inflation will remain at these levels and adjust behaviour accordingly. Weaker commodity prices will only serve to put further downward pressure on inflation. Even the escalating US-Iran standoff did not raise the oil price much and it is 11% lower than a year ago. Secondly, the Fed is worried that weakness in the global economy could spill over to US shores, which is a departure from the past practice of ignoring the rest of the world. (Unfortunately, the rest of the world has never had the luxury of being able to ignore the Fed.)

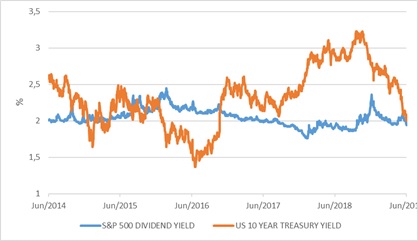

Finally, there is the risk management argument, which calls for cutting rates now rather than waiting for the economy to show real signs of weakness or, as Powell put it, an “ounce of prevention is better than a pound of cure”. The last point is important. If the Fed was reacting to economic weakness rather than trying to pre-empt it, stock markets should be falling, not rising. Instead, the US S&P 500 hit a new all-time high. Bonds also rallied, with yields declining even further after the meeting. The yield on the global benchmark sovereign bond, the US 10-year Treasury, fell to 2% for the first time since late 2016. Gold also shot up to its highest level in six years. Lower rates help equities in three principal ways: by lowering the borrowing costs of companies, by increasing the present value of future cash flows, and by making them more attractive relative to fixed income. The S&P 500 dividend yield is also at 2%, meaning investors can get the same income as a 10-year bond, but with the upside of growth.

Chart 1: US bond and equity yields

Source: Refintiv

Draghi low on ammunition

At least the Fed has some room to cut rates from current levels at around 2.5%. The deposit rate of the European Central Bank (ECB) is -0.4%, and its economy is in worse shape than that of the US (due to being much more exposed to global trade, Brexit uncertainty and the fact that Italy never really recovered from 2008). Core inflation remains stuck at around 1%, nowhere near the ECB’s target of close to 2%. Nonetheless, at the ECB’s annual conference in Sintra, Portugal, President Mario Draghi argued that rates could be pushed deeper into negative territory, and that the Bank’s bond buying programme (also known as quantitative easing) could be restarted. This earned him a rebuke from none other than US President Donald Trump, who accused Draghi of trying to push the euro down, giving European firms an advantage over American ones. This was also an implicit criticism of Powell, who was, ironically, appointed by Trump.

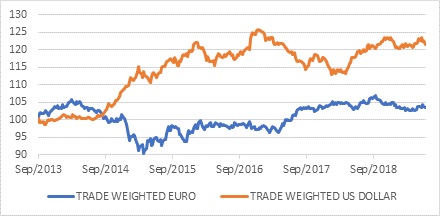

From trade wars to currency wars

This is an echo of the famous 2011 “currency war” comment of the Brazilian finance minister at the time, who complained that central bank stimulus in the developed world was causing capital flows into emerging markets, strengthening their exchange rates. A strong currency is a double-edged sword, as it increases the global purchasing power of consumers and businesses, but depresses the global competitiveness of exporters. Though Trump cannot tell Powell what to do, he will clearly maintain pressure on him should the dollar remain strong. Trump might also be tempted to slap tariffs on European imports, though this is only likely to strengthen the dollar more. If he wants a weaker dollar, backing off from all of his tariff threats would be a good start. Trump and Chinese President Xi Jinping are set to meet face-to-face at the G20 summit this week, which will hopefully lead to a restart of stalled trade negotiations.

Chart 2: Trade weighted dollar and euro indices

Source: Refinitiv

Search for yield reignited?

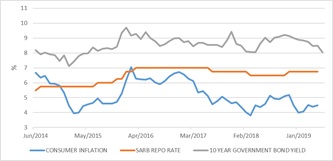

Provided there is no further escalation in the US-China trade battle, emerging markets could be major beneficiaries of the dovish turn of developed central banks, with the search for yield reignited. Already, $12.5 trillion of bonds from Europe and Japan trade at negative yields according to Bloomberg. Such flows could overwhelm the negative impact of further domestic fiscal deterioration and potential downgrades. Even if the SA Reserve Bank follows other central banks by easing rates by 0.25% to 0.5% this year – which it should do with a weak economy, inflation on target at 4.5% in May and the rand oil price 10% lower than a year ago – local rates are still high in a global context.

Chart : South African interest rates and inflation

Source: Refinitiv

This scenario of a stronger rand and lower bond yields could provide a window of opportunity for President Ramaphosa to implement reforms. One of the many dilemmas we have is that some of the key reforms needed for long-term growth can hurt the economy in the short term. Job cuts at Eskom to improve its financial sustainability is an obvious example. The best time to push through painful reforms is when the economy is doing well. Unfortunately, there are very few countries where this has happened. Usually, difficult restructuring is done only when forced by a crisis.

SONA, so close, so far

In the absence of a such a raging crisis, President Ramaphosa’s SONA did not deliver much new. There is still no sign of a much-needed restructuring of the portfolio of State Owned Enterprises, many of whom bleed the fiscus and impede economic activity. Government will instead be fast tracking a portion of the R230 billion bailout for Eskom, without providing details on its unbundling. The utility is still without a CEO or Chief Restructuring Officer. The positive aspect of the speech was not its substance but its tone. The National Development Plan – released long ago in 2012 – has made a comeback as “the centre of our national effort”. The focus is rightly on implementation rather than on new plans. Ramaphosa emphasised the need to stimulate economic growth and improve the ease of doing business. Importantly from a policy certainty point of view, he reaffirmed the Reserve Bank’s independence and mandate. Although he spoke at length of the great need to speed up land reform, including making state-owned land available, “expropriation” was not mentioned, nor were prescribed assets. Rather, he wants greater coordination between private and public efforts to improve the country’s infrastructure. Coming off a low base, even small changes can have a sizable impact. But it is delivery and not soaring oratory that will convince investors and business leaders to commit capital.

Eyes on the prize

Does all this necessitate portfolio changes? Nobody knows exactly how the future will play out. For this reason, appropriate diversification is important, with portfolios tilted towards cheaper – and by implication less popular – assets. If South Africa does become the beneficiary of emerging market capital flows, the resulting stronger rand will benefit interest-rate sensitive assets such as bonds, property, bank and retail shares. A weaker currency, whether due to domestic political uncertainty or global risk aversion, will support offshore assets rand-hedges on the JSE. In good times and bad, spreading the risk makes sense. The key thing for investors is not to react to every move the market makes and every newspaper headline, but rather to make investment decisions based on their goals and circumstances.