Separating the sizzle from the steak: Examining the need for diversification

What do Bernie Madoff, Barry Tannenbaum and Sharemax have in common? They started as credible organisations run by known people – people who also knew how to create allure and marketing buzz – SIZZZLE – and they all had an emotional hook.

A former Chairman of the NASDAQ, Madoff was a man of stature and clout in the community. The fact that his company was founded in 1960 created additional credibility. In 1992, the $740m average daily volume of trades executed electronically by the Madoff firm equalled 9% of the New York Stock Exchange trades.

Madoff built a Ponzi scheme by targeting charities, meaning he could avoid sudden or unexpected withdrawals. The 5% pay-out rule (a federal law requiring private foundations to pay out 5% of their funds each year), allowed his scheme to go undetected. For every $1bn in foundation investment, he was effectively on the hook for only $50m in withdrawals a year. If not making real investments, at that rate, the capital would last 20 years. His brokerage operation was very real, unlike most Ponzi schemes that are based on non-existent businesses. Instead of offering high returns to all-comers he offered modest but steady returns to an exclusive clientele – around 10% per annum. His returns were unusually consistent and he paid out quickly when cash was requested. He refused to meet with his investors and created such an allure that many investors refused to withdraw for fear of not being able to get back in.

He was arrested on the 11th Dec 2008 and sentenced to 150 years in prison. The size of the fraud committed is reported to have amounted to about $64.8bn (4,800 clients). In his plea he admitted to having not traded since the mid-1990s.

Barry Tannenbaum was also someone of perceived stature, having had a grandfather who was a co-founder of Adcock Ingram. Premised on an investment in AIDS drugs and backed by his family name, he offered investors 15% every 12 weeks for providing funds to purchase raw materials for sale to drug makers. People thought that the cause was noble, but they also liked the returns they were making. Both reasons were emotionally led.

About 34,000 people invested some R4.4bn in the various property schemes promoted and marketed by Sharemax. The initial attraction was the interest being paid to investors, which was above market-related rates, as well as the generous commissions paid to marketers of the scheme.

For the average investor, emotion is an important element of decision making. And emotion makes it harder to discern and follow the facts, let alone see through any deception.

Our examples clearly show there was so much sizzle but very little steak.

If one is emotionally invested, it isn’t always easy to identify the steak. And, sometimes, the sizzle is subtle, involving no illegal activity but rather misleading, misunderstood or misinterpreted info.

Examples of the market looking good, but not really being a great investment can be seen in the slide below:

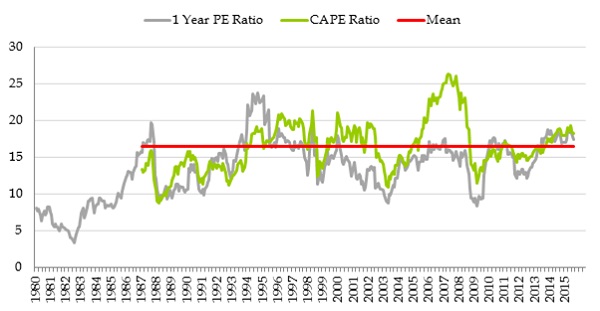

Chart 1: PE ratio, CAPE ratio and mean – JSE-FTSE All Share Index

Source: Data from Bloomberg, analysis by Cannon Asset Managers

The Price Earnings (PE) multiple in the slide above, shown on the gray line, represents price relative to one-year earnings. The green line represents the CAPE (Cyclically Adjusted Price Earnings) ratio, the current price to 7-year earnings (averaged out and inflated). The CAPE ratio affords a better reflection of the DNA of a stock, given that it looks at a full business cycle. In 2007/2008, it was quite clear that the All Share Index was overheated on a CAPE basis but not if one looked at the 1-year PE. Many investors were still piling into the market at that stage, assuming the PE multiple in 2008 represented fair value. Had they considered the CAPE ratio, they might have behaved differently.

This underscores the importance of using wealth planners and asset management professionals in situations where an investor may have limited access to such investment tools.

Even for the professional investor, assessing the market can be a challenge. The construction industry provides an excellent example. Construction firms were found guilty of “determining, maintaining and monitoring collusive agreements”. The Competition Commission reached settlement with 15 construction firms and a total fine payable, as per the Commission’s recommendations, was R1.46bn, which is the largest fine ever recommended by the Commission for a single industry.

Pinnacle Technologies is another example. Takalani Tshivase was accused of fraud and the directors were being probed for insider trading, because they took three weeks to announce these allegations publicly. While the charges against Tshivase have been dropped, and the insider trading investigation has been withdrawn, the stock price slumped by almost 60% in value at the time and still trades at reduced levels.

How could one have known about the collusion that resulted in massive fines or insider trading allegations, even as a professional or specialist asset manager?

Listed companies, while governed by many regulations, can and do apply aggressive accounting methods. So for the ordinary investor, who does not have the knowledge or research tools, the ability to separate the sizzle from the steak is sometimes almost impossible.

How can we avoid buying the sizzle?

There is no holy grail or one definitive answer. It is possible that we will be caught out if we do not apply ourselves. The following points are probably the closest we can come to protecting ourselves from ourselves.

• Consult specialists

These specialists have the tools to determine problems or possible re-ratings. While specialists will make mistakes and be “caught out” from time to time, the possibility of these risks are accounted for in their asset allocation processes. If their processes are robust and their portfolios are well diversified, the impact of an African Bank collapse or Pinnacle Technologies event will be minimised.

• Look around – if it appears too good to be true, it is

If those pensioners went to Sharemax for the best return, they did so probably out of necessity. But if other entities were offering well below that on average, it should have raised alarm bells. The Tannenbaum scheme offered equally unrealistic returns. At 15% every 12 weeks, why weren’t formal lending institutions clamouring for the business? Or why wouldn’t Tannenbaum borrow from the banks at a regular interest rate and pocket the difference himself?

If we simply open our eyes the answers are always there. There is always a red flag flying high – we just have to look for it and this sometimes requires asking questions or simply observing. And no one is a victim of anything – everything is a choice. The question we should always ask is: What level of risk is being taken for the return offered?

• Look inwards

Buy unemotionally and not from greed or necessity. How do we do this? Learn to observe ourselves so that we can identify what emotions drive our thinking process. By observing, we learn to acknowledge what our triggers are and how we play them out in our lives. And partner with specialists who can help us manage our emotions. How many times do we hear people saying “I knew.....?” Yet they didn’t trust that inner voice. And if you cannot hear your inner voice or do not trust it, partnering with specialists is vital.

• Diversify

And most importantly, diversify. The only free lunch is to diversify. If we are going to play the game, we have to make sure we know that it is possible that one element may go wrong while the other is going right. Every sound investment manager diversifies within the portfolios they manage. This principal should be extended to investors in their personal approach.

A portfolio of different kinds of investments will, on average, yield higher risk-adjusted returns than any individual investment found within the portfolio. Aside from a smoother ride, diversification also strives to smooth out unsystematic risk events such as the downfall of one stock or company. And diversification both within the stocks one holds and geographically is important. Different regions will have differing economic and business cycles which means diversification will cushion the ride.

It is seemingly easy to be enticed by the sizzle. But by keeping your wits about you, and confirming that there is steak to accompany it, your investment taste buds are sure to be satisfied.