Sailing close to the wind

South Africa’s Budget 3.0 was tabled in Parliament on the same day President Ramaphosa met US President Trump in the White House.

The US Congress was also in the process of passing a budget – perfect timing to compare the fiscal policies of South Africa and the US.

Simply put, the two countries are moving in opposite directions. People with different political persuasions will disagree on which direction to take. Some will argue for tax cuts, others for higher taxes, especially on the super-rich. Many will argue for increased government spending, especially on social welfare, while others will prefer to reduce the size of the government. Viewed from the perspective of the market, however, it is clear. South Africa is trying to steady the ship, while for the US, it is a case of anchors away.

As for the meeting between Ramaphosa and Trump, expectations were quite low, and indeed there was a lot of bluster from the US president. The main thing is that a dialogue on trade has been opened, and this reduces the risk that US import tariffs on South African goods jumps to 30% again after the 90-day pause.

Uneventful

Compared to the fireworks of the first two proposed South African Budgets the third version was decidedly uneventful. However, in this context, boring is good, and the financial market response was muted.

The key thing from investors’ point of view is that fiscal consolidation remains the priority. The debt and deficit ratios are similar to what was presented in March, though they are somewhat worse, mainly due to weaker expected nominal growth (i.e. a smaller denominator, not a larger numerator). Due to the abrupt change in US trade policies, global growth is expected to be lower and the domestic real economic growth outlook has been cut to 1.4% for 2025, 1.6% for 2026 and 1.8% for 2027. This is broadly in line with private sector estimates. Inflation is likely to be somewhat lower, reducing nominal growth. Weaker nominal growth tends to put downward pressure on tax collection.

As expected, there will be no VAT increase this year. However, unspecified tax hikes are pencilled in from next year (around R20 billion per year), suggesting a small VAT hike could still be on the table, but Treasury will be sure to get political buy-in beforehand. If SARS improves collection, this might not be necessary. As might be expected given the decline in global oil prices, the fuel levy will rise by 16 cents per litre. The basket of VAT zero-rated items will not be expanded, and there is no bracket creep relief for personal income taxpayers.

Without revenues from a VAT hike, some of the additional spending proposed in the first two attempted Budgets will be rolled back. Nonetheless, there is still a R180 billion increase to the baseline over the medium term, compared to R233 billion in Budget 2.0. This will support frontline delivery and infrastructure spending. Treasury plans to spend R1 trillion on infrastructure over the medium term. This a big number, but implementation remains the challenge. Spending reviews have identified around R38 billion in savings from closing down ineffective or unnecessary programmes. This will be applied to future budgets and could possibly mitigate the need for tax measures in 2026 and beyond.

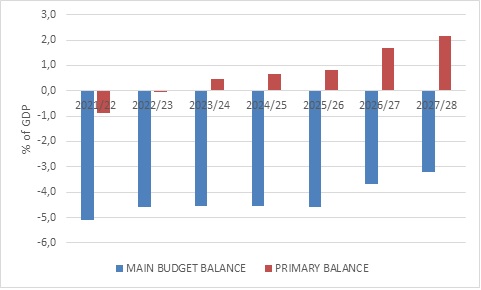

Chart 1: South Africa’s budget balance with projections

Source: National Treasury

Importantly, Treasury will maintain a primary surplus, meaning that tax revenue is projected to exceed non-interest spending. It will rise over the medium term from 0.7% of GDP to 2.1% in 2027/28. The main budget deficit, which includes interest payments, is expected to continue narrowing over the medium term, reaching 3.2% of GDP by 2027/28. In other words, the budget deficit now consists of interest payments.

As a result of running a primary surplus, the debt-to-GDP ratio is projected to peak in the current fiscal year at 77.4% and drift lower over time. A peak in the debt ratio has been promised for a decade, and never happened, but we are closer than ever.

Click here to read more...