SA property sector, what happened and where to from here?

It’s no secret that 2018 was a difficult year for investors with most asset classes declining in value both locally and abroad. However, one asset class does stand out amongst the rest – SA’s listed property sector. The listed property market experienced substantial volatility and share price decline during 2018, caused by company specific issues combined with local economic concerns.

Some of the company specific issues include the Viceroy report around the Resilient group of companies, which prior to their collapse, comprised over 40% of the South African Property Index (SAPY). The more recent research around NEPI Rockcastle (also part of the Resilient group of companies); and a potential take-over bid for INTU properties falling through, resulted in the stock losing more than 45% in November alone.

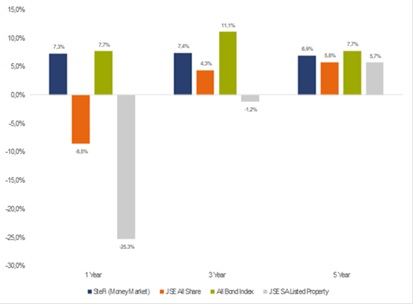

In the past few years prior to 2018, the property sector managed to outperform all other local asset classes, but the impact of stock specific declines in 2018 combined with a low growth environment resulted in listed property experiencing its worst calendar year return since inception of the index in 1993. The asset class delivered -25.2% for the twelve months ending in December 2018, taking the three-year return to a mere -1.1%. Compared to a three-year return ending in December 2017 at 11.7%!

Unpacking these numbers, it is important to have a closer look at the listed property space and how it has evolved over the last couple of years.

The listed property sector is a relatively small sector by global standards, at roughly R540 billion AUM as at end December 2018 (that is approximately 3% of the total assets listed on the JSE). Historically the widely used South African Property Index (SAPY) was used as the measure of the property sector performance but this index has significant shortcomings including, only 21 counters were included int eh calculation of the index. Additionally, the index is disproportionate in index weights, with heavyweights Growthpoint and Redefine comprising 37% of the index. During 2018, a broader property index was introduced, the All Property Index (ALPI), which incorporated dual listed property counters such as Capital and Counties, INTU and Hammerson to name a few. It is argued that this index is more representative of the investable universe and reduces concentration risk. However, this index does have a higher exposure to offshore counters, specifically the UK, which is likely to change the return profile of the sector that SA investors have historically had a love affair with.

Going forward the listed property sector can be broken down into three broad categories:

1. The Resilient group of companies (Resilient, Greenbay, NEPI Rockcastle, Fortress A and B, Sirius Real Estate Ltd). As at end December 2018, this equated to roughly 24% of the ALPI.

2. SA focused property counters including heavy weights Growthpoint and Redefine Properties. These would be property companies that generate most of their earnings in South Africa and are therefore reliant on SA economic growth. Roughly half of the ALPI as at end December 2018.

3. Foreign listed counters including INTU, Hammerson and Capital & Counties. These counters are merely listed in SA, with their operations and properties siting elsewhere in the world. As at end December 2018, the foreign listed counters equated to approximately 30% of the ALPI

In addition, each distinct part of the listed property space faces their own unique risks. These include:

• Resilient group of companies: Ongoing investigation into the Resilient group of companies and the valuation methodology used;

• Locally focused stocks: low growth environment in the SA market combined with uncertainty created by land expropriation;

• Offshore listed stocks: aside from the volatile rand affecting the return profile of these counters, global property markets are facing uncertainty around Brexit, rising interest rates (especially in the US), as well as a rise in online shopping, pointing specifically to Sears bankruptcy and its likelihood of creating jitters in the US retail sector.

Looking forward, the SA Listed Property sector has experienced an extremely volatile period which could continue until the Resilient group of companies shows signs of stability and hope for certainty. While overall valuations (price/NAV as well as on a yield-relative basis compared to SA bonds and equities) look very attractive, distribution growth expectations have been scaled back due to subdued domestic conditions, rising vacancies and an over-supply of space, especially in specific nodes within the office and retail sector. Investors should look at a number of factors when considering an investment in this sector:

1) What is my current yield and is it sustainable? Currently the sector is yielding 9.3% which is a very decent yield in absolute terms and when compared to history. The question is around the sustainability of this yield.

2) Fundamental risk and quality?

3) How will currency impact my returns? Close to 50% of the earnings on the ALPI are derived outside of SA. The sharp manner in which our currency experiences deviations can have a material impact on our asset returns and income stream.

2018 was a largely disappointing year for investors with large allocations to the listed property sector. Despite this, investors are encouraged to remain calm and rational when making investment decisions. Asset class behaviour can be volatile in the short-term, however, history has taught us that investors with long time horizons need decent allocations to risk assets in order to generate inflation beating returns.