SA Medium Term Budget – low growth & high wage bill cause fiscal slippage

Sanisha Packirisamy, Economist at MMI Holdings.

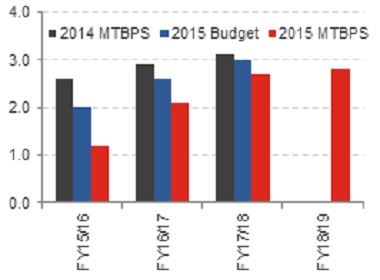

Against the backdrop of a more subdued global economic recovery and muted domestic prospects, National Treasury has had to revise down their real GDP growth forecasts between FY2015/16 and FY2017/18 by 0.5% (on average), leaving the three-year average close to our own internal forecasts projected at 2%.

Weaker growth punctures revenue prospects

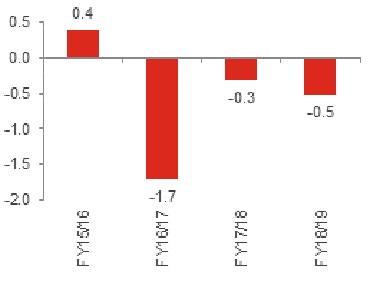

The largest growth revision has been to FY2015/16 where weaker commodity prices and energy supply constraints have prohibited higher rates of growth (see chart 1).

Chart 1: Treasury downwardly revises real GDP growth forecasts (%)

Source: National Treasury, Momentum Investments

Nominal GDP growth estimates over the same time period have been adjusted down by a lesser 0.4% (on average), given upward revisions to Treasury’s inflation profile. Treasury now expects inflation to average 5.8% between FY2015/16 and FY2017/18; 0.4% higher than their estimates in the February 2015 National Budget, on the back of electricity tariff concerns and a weaker currency, while they have kept their oil price forecast in a tight range between USD55/bbl and USD57/bbl over the next three years. Treasury warns that firms’ ability to absorb higher input costs may narrow if rand depreciation and shrinking profit share continues, resulting in upside risks to their upwardly-revised inflation trajectory.

Medium-term fiscal slippage partly a function of growth downgrades

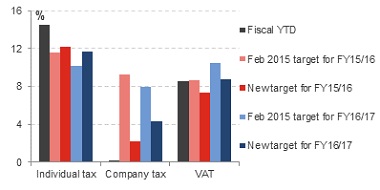

High public (and private) wage settlements were behind the higher-than-expected personal income tax (PIT) and value-added tax (VAT) collections so far in FY2015/16, allowing for a slight narrowing in the (consolidated) budget deficit-to-GDP ratio to 3.8% from the 3.9% predicted in February this year. Lower growth estimates have nevertheless shaved off R34.6 billion from gross tax revenues over the next three fiscal years, while total expenditure was ramped up by a further R37.7 billion over the corresponding period. The combination of a poorer outlook on growth and a higher-than-budgeted for wage bill suggests a delay in fiscal consolidation. According to government, the budget deficit-to-GDP ratio is expected to narrow to 3.2% by FY2017/18, relative to 2.5% estimated in February.

Weak consumer confidence, tight credit conditions and anaemic employment growth pose a threat to the relatively robust PIT buoyancy observed over the past year, while muted commodity prices and benign demand is expected to weigh negatively on corporate revenue collections, further threatening Treasury’s expected fiscal consolidation timeline. In particular, we see downside risk to government’s relatively optimistic expectations for an 11.7% y/y, 4.3% y/y and 8.7% y/y rise in PIT, company tax and VAT, respectively, in FY2016/17, given the pedestrian outlook for domestic growth and commodity prices (see chart 2).

Chart 2: New revenue targets set for FY2016/17 look too optimistic

Source: National Treasury, Momentum Investments

Although no specific revenue proposals were outlined, Treasury highlighted the Davis Tax Committee’s reports, commenting that an increase in VAT rates remains an option over the medium term. We remain of the opinion that the timing of a VAT rise would coincide with meeting the financing needs of a larger project such as the National Health Insurance (NHI) plan further down the line, while options such as closing existing tax loopholes or raising capital gains taxes, estate duties or income taxes for the country’s highest-income earners could be explored in the near term. Although we believe there is little appetite to raise corporate taxes (a deterrent to foreign inward investment), the proposed carbon tax will likely hinder corporate profitability further in the current environment.

Sticking to the expenditure ceiling despite wage bill overrun

Notwithstanding challenging economic circumstances, Treasury has committed to adhering to the expenditure ceiling, which when using the main budget figures implies real non-interest expenditure growth at an average of 1.9% p.a. between FY2015/16 and FY2018/19, or 2.5% using the consolidated budget numbers. Government noted that an adjustment to the ceiling would only be considered under two key scenarios, viz. a structural improvement in revenue or a large inflation shock eroding the value of real spending.

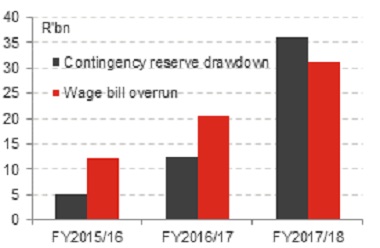

Government has drawn down on the contingency reserve in an effort to cover the higher-than-expected public sector wage agreement that led to a R63.9 billion shortfall. The R5 billion reserve set aside for FY2015/16 has been wholly absorbed, while a further R12.5 billion and R36 billion from FY2016/17 and FY2017/18, respectively, have been cut to offset a portion of the higher compensation bill (see chart 3). However, the implication is that SA’s fiscal manoeuvrability to deal with unforeseen revenue or expenditure shocks in the coming years has been compromised dramatically, a factor that is unlikely to go unnoticed by the credit rating agencies in their assessment of SA’s status as a borrower.

Chart 3: Drawdown in contingency reserve partially offsets higher compensation bill

Source: National Treasury, Momentum Investments

To make up for the remaining wage bill shortfall, Treasury warned that departments may be required to shift funds within their own portfolios away from goods/services and capital budgets to support compensation budgets wherever moderate declines in employment and overestimations in budgets are insufficient to fund the overrun. The resultant negative real capex growth budgeted for in the medium term to make up for the anticipated 2% real increase in compensation budgets is a worrying dynamic for the long-term growth potential of the SA economy.

Potential scaling back of infrastructure a risk to SA’s sovereign rating over the medium term

Although there was no detailed breakdown of budgeted infrastructure spend, Treasury projects over R800 billion worth in infrastructure over the medium term, which is to be accompanied by reforms to strengthen infrastructure implementation. Improved project execution is slowly materialising with local government underspend dipping to 9% in FY2014/15, from 14% in FY2013/14 and 23% in the prior fiscal year.

Nevertheless, the wage bill overrun still poses a risk to growth in public infrastructure spend, dampening prospects for higher, sustainable trend growth, particularly against the backdrop of economic policy uncertainty and dull domestic demand clouding the outlook for a further acceleration in private fixed investment spend. While we are not anticipating an imminent downgrade of SA’s sovereign debt to junk status, the rating agencies have been warning that the SA economy remains trapped in a low-growth environment, providing little hope of a significant improvement in its fiscal and debt ratios.

Tricky to match slowing cyclical revenue with structurally-high expenditure

In the absence of growth-enhancing structural reforms, SA will struggle to exceed or even return to its historical trend growth rate of 3.1%. Meanwhile, the number of social grant recipients has ballooned from 2.5 million in 1998 to 16.7 million today and is set to grow further to 18.1 million by FY2018/19. Similarly, wage demands eclipse a near 40% of the (non-interest) expenditure bill, which will be tough to reverse in an environment where nearly three-quarters of the public sector is unionised and where debates around higher minimum wages are still taking place.

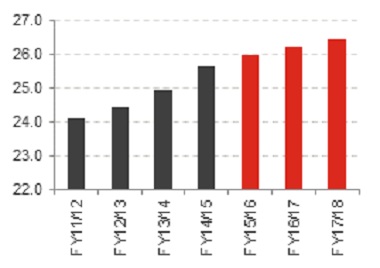

SA’s tax burden is set to climb from 25.7% currently to 26.5% by FY2017/18 and could likely rise over the longer term as government struggles to meet fiscal consolidation and debt targets (see chart 4).

Chart 4: Tax-to-GDP ratio edging higher (%)

Source: National Treasury, Momentum Investments

The rising tax burden accompanying fiscal consolidation implies that the budget is removing spending power from the economy on a net basis between FY2016/17 and FY2018/19 and as such can be construed as contractionary for the economy. Furthermore, the fact that spending growth (averaging 8.5% p.a. between FY2015/16 and FY2018/19) is expected to lag revenue growth (averaging 9.0% p.a.) over the corresponding period also implies a net drain on economic activity (see chart 5) over the medium term expenditure framework (MTEF).

Chart 5: Revenue growth outstrips expenditure growth over the medium term (%)

Source: National Treasury, Momentum Investments

Onerous debt costs crowd out more preferable forms of expenditure

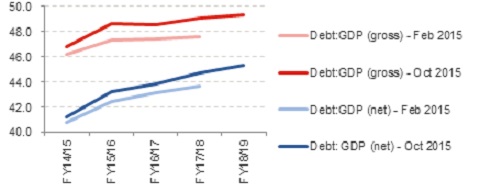

Government attributes the deterioration in the debt-to-GDP ratio to a weaker currency and lower growth leading to revenue shortfalls. The gross debt-to-GDP ratio is expected to climb further to 49% of GDP by FY2017/18 (1.4% higher than projected in the February 2015 National Budget), while the profile for the net debt-to-GDP ratio deteriorated by a further percentage point in FY2017/18 (see chart 6).

Chart 6: Deterioration in government debt profile (%)

Source: National Treasury, Momentum Investments

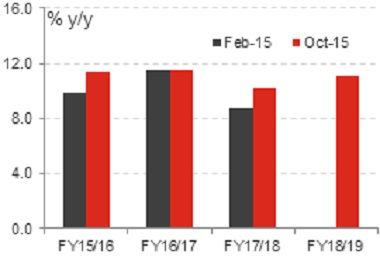

Due to the increase in government borrowing, debt-servicing costs are expected to remain the fastest-growing expenditure item, increasing at an average rate of 11.1% y/y p.a. (5.3% in real terms) between FY2015/16 and FY2018/19 (see chart 7). The rapid rise in debt-servicing costs is crowding out other (social and growth-enhancing) spending priorities and has been raised as a key concern by the rating agencies in the past.

Chart 7: Rapid rise in debt-servicing costs crowds out other spending priorities

Source: National Treasury, Momentum Investments

Financially-strained state-owned enterprises a risk to overall debt threshold

Treasury suggested that only R245 billion of the available R470 billion worth in guarantees are currently being employed, with Eskom utilising R162 billion from their R350 billion allocation. Although government insists that any additional support to struggling state-owned enterprises (SOEs) will be met with deficit-neutral financing, additional support could threaten the overall 60% debt-to-GDP (including contingent liabilities, provisions and guarantees) threshold that government has guided towards in the past.

High financing needs for longer-term spending projects

The high funding requirements associated with longer-term projects (e.g. nuclear) or structural increases in expenditure (e.g. NHI) are increasingly demanding in a low-growth environment. Treasury reiterated the NHI plan would be phased in over a fourteen-year period, reaching full implementation by FY2025/26. While the current pilot projects have not had a significant impact on the existing health budget (which is set to increase at an average rate of 8.3% p.a. over the MTEF), a rise in VAT rates could be on the cards to support the eventual rollout of NHI.

Treasury also announced a R200 million allocation over the medium term to support preparatory work for nuclear procurement, but admitted that more work has to be done to establish the costs, benefits and risks of building nuclear capacity.

Although no additional allocation was made to tertiary education for this fiscal year, government has formed an inter-departmental team to work through the financial implications of a white paper on post-school education and to determine how to fund the expected expansion in enrolments.