Riding out the rollercoaster of investor emotions

Uncertainty in the global environment and domestic risks around the upcoming election have led to an increase in market volatility. What can SA fixed income investors expect when the election dust has settled? Ninety One Emerging Market Fixed Income portfolio managers, Malcolm Charles and Adam Furlan, share their insights.

Coming into 2024, market sentiment in global bond markets improved on a better outlook for inflation, fuelling expectations of a series of global rate cuts during the year. However, a more resilient US economy and stubborn global inflation have delayed the start of the US rate-cutting cycle, with lower rates only expected toward the end of the year.

With investors once again repricing in ‘higher for longer’ rates, we’ve seen an uptick in global bond market yields, which has also resulted in higher SA bond yields. Adding to this, local election fears have weighed heavily on our market, further pushing up SA bond yields. Foreigners turned net sellers of SA government bonds in February which abated towards the end of April following the release of more constructive polling results. Consequently, the SA bond market has clawed back 30 basis points of the underperformance relative to its emerging market (EM) peers, as can be seen in Figure 1.

Nevertheless, the chart still shows that approximately 60 basis points of extra risk premium have been priced into our bond market since the start of the year (9-year SA government bonds vs. EM peers). This comes at a time when South Africa has had a pragmatic Budget, a material decline in load-shedding and an improvement in Transnet’s operational performance. Our bond market’s underperformance versus our peers highlights SA election concerns.

Figure 1: SA election temperature on the rise

Source: Bloomberg.

What can we expect after the election dust has settled?

If the politicians manage to reach a pragmatic outcome after the election, the focus should return to broader macro issues. We’ve seen some positive developments that should help to support investor sentiment:

• Eskom: load-shedding continues to improve, thanks to better performance at some of the power stations and the growth in private generation.

• Transnet: the situation appears to have stabilised. We are seeing a material turnaround at the Durban and Cape Town ports, with the coal line and iron ore line back at pre-pandemic levels.

• The South African Reserve Bank (SARB) remains solid. The new appointments and term extensions signal institutional stability and policy certainty.

The green shoots that we are witnessing on the energy front and at the ports should also help to bolster our fragile economy.

SA inflation fairly ‘well-behaved’

CPI inflation remains contained within the SARB’s target band but continues to be sticky. We see headline inflation averaging 5% in 2024 and core inflation averaging 4.6%. With global rate cuts pushed out, we only expect the SARB to lower interest rates later in the second half of the year. This will be dependent on several factors including the SARB’s assessment of the sustainability of the downward trajectory of inflation towards the 4.5% target, and the timing of rate cuts in the US.

For now, we at Ninety One are riding out the rollercoaster of investor emotions, but we believe there will be opportunities for us to participate when market conditions improve. Our view is that the eventual election outcome is likely to be more pragmatic than some expect, and as such, there will be an opportunity to take advantage of this mispricing. Timing will be important as fears are likely to peak in the days ahead of the actual election.

While uncertainty prevails, we believe the high yields on SA bonds sufficiently protect against the risks and represent good value over the medium to longer term. Income will remain an important driver of return, with high yields offering investors the opportunity to earn returns well ahead of inflation. We remain cautious on positioning and continue to emphasise the importance of maximising yield and protecting capital.

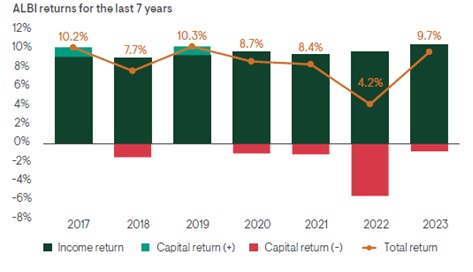

Figure 2: Higher yields will once again provide an income shield during 2024

Source: Bloomberg and Ninety One, 29 December 2023.