Returns return

The US equity market has led the rest of the world higher this year. The benchmark S&P 500 is up 18% in 2019, and 25% since the market bottomed on Christmas Eve last year. It slumped by 19% in the preceding eight weeks.

Markets trend up over time

The US market reaching a new all-time high is not a concern. After all, markets trend up over time and will naturally be breaking records along the way. The concern is whether the market has rebounded too quickly, pricing in too much good news. Most of the 18% returns this year have been as a result of multiple expansion, i.e. prices rising faster than earnings (with the price earnings multiple expanding). Expected earnings growth has slowed to close to zero, though a number of companies are beating expectations. At the start of the year, the S&P 500 traded at 14.5 times forward earnings, but it currently trades at 17 times forward earnings. The long-term median is 14.5.

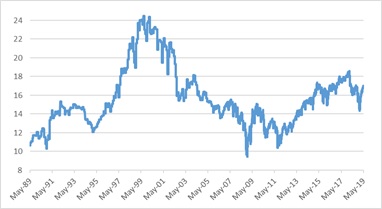

Chart 1: S&P 500 forward price earnings ratio

Source: Refinitiv

Patient Fed, impatient markets

What is behind this rapid rebound? First and foremost, the US Federal Reserve. The Fed, as it is widely known, somewhat abruptly changed course in its interest rate stance. It hiked rates in December, but a month later shifted to keeping rates on hold for the foreseeable future. This stance was affirmed at last week’s meeting of its rate-setting committee. It makes sense. The Fed has a dual mandate: low unemployment and inflation of 2%. On the former it can claim full marks, as unemployment is close to historic lows at 3.6%. The US economy added 263 000 new jobs in April, more than the monthly average of 190 000 since 2010. However, the Fed has failed on its inflation goal and is falling further behind. Though its preferred inflation measure (personal consumption prices other than food and fuel) was above 2% for five months in early 2012 and for one month last year, it has been below target for the rest of the time over the past decade. The recent trend has been heading in the wrong direction, with the March print coming in at only 1.5% year-on-year. While low inflation sounds great, the concern from the Fed’s point of view is that it becomes embedded in the inflation expectations of consumers and firms, and hence leads to changed behaviour, where sub-2% inflation becomes the norm. The South African Reserve Bank has the opposite goal. It wants inflation expectations to drift lower to 4.5% and will maintain high real interest rates until that happens.

Fed Chair Jerome Powell blamed temporary factors, expressing confidence that a solid economy would result in rising inflation in coming months. That is the theory of course. In practice, the red-hot jobs market in the US has resulted in very little wage growth (only 3% year-on-year in April) and a healthy economy has not resulted in consumer prices rising rapidly. In the end, workers and firms compete not only with global counterparts, but also against technological innovations and hence lack pricing power. The same is true locally of course, but we don’t have the benefit of a strong economy, so there is very little demand pulling prices higher. It is only administered prices of items that consumers cannot substitute (like municipal rates and electricity tariffs) that are pushing prices up. Many market participants were clearly hoping for the Fed to signal rate cuts at last week’s meeting, but the Fed is a cautious institution and unlikely to swing from hiking to cutting mode so quickly in the absence of data that suggests it should.

The US economy is still posting decent growth numbers, even if the 3.2% growth in the first quarter was flattered by a large build-up of inventories (unsold production). Spending by businesses and consumers moderated somewhat, but with consumers still enjoying real income growth, the outlook for the rest of the year is still pretty good. Overall growth will probably be at a slower pace than last year’s tax-cut fuelled 3%, but fears of a looming recession, which contributed to December stock market swoon, are misplaced. Instead, the US market enjoys somewhat of a goldilocks environment – not too hot (with inflation low and interest rates on hold) and not too cold (moderate economic growth). The question is just whether investors are pricing in too much of a fairy-tale ending while ignoring the risk of bears showing up.

Dollar and trade war risks

One risk is persisting trade tensions. Over the weekend, US President Donald Trump unexpectedly threatened to increase tariffs on Chinese imports again. This was a surprise as trade talks between China and the US seemed to be progressing well, and markets opened lower on Monday.

Another risk is the rising dollar. With one central bank after the next signalling lower for longer interest rates, and with the Fed ruling out rate cuts for now, there seems to be little chance of interest rate differences between the US and the rest of the developed world narrowing. A strong dollar tends to hurt the US multinationals that dominate the S&P 500 by reducing the value of foreign sales and by placing downward pressure on commodity prices. It is the stronger dollar, and not Wednesday’s looming election, that has seen the rand lose ground recently.

Chart 2: US trade-weighted dollar index

Source: Refinitiv

US sets the tone

The US sets the tone for global markets, including the JSE. Therefore, while South Africans’ attention has been focused on the election, the local market has gained 14% in the background this year. Most of this has been due to the JSE’s global companies, including Naspers, BAT, Anglo American and BHP. However, April saw some locally focused firms do well. For instance, general retailers gained 10% in the month but the subsector is still negative year-to-date, while banks jumped 9%. It is not because the latest local economic data is particularly strong; the recent data is mixed at best.

Local data mixed

The Bureau for Economic Research’s (BER’s) long-running Consumer Confidence Index declined in the first quarter, but remains in positive territory. This in contrast to its Business Confidence Index, which remains depressed. The BER’s Manufacturing Purchasing Managers’ Index rose two index points in April but remains in negative territory. Retail sales growth was positive in real terms on a monthly basis in January and February, but underlying activity in the sector is weak. On an annual basis, real growth was only 1.1% in February. More notably perhaps is that nominal growth was only 3.6%, implying retail inflation of slightly more than 2%. This picture of low volume growth and very little price growth is also reflected in the results and trading updates of the JSE-listed retailers (though several have reported price deflation). Household borrowing growth continues to gradually increase, with March’s number rising to 5.9% year-on-year. Though it is the fastest pace since October 2013, it comes after almost five years of lagging income growth. There was an uptick in new vehicle sales in April, but the average number of vehicles sold locally in 2019 is still below 2018 and 2017. Vehicle exports are doing well though.

Chart 3: South African new vehicle sales

Source: NAAMSA

South Africa posted a R5 billion trade surplus in March, but this was not enough to push the trade balance for the first quarter into surplus territory. However, the R3.8 billion deficit for the first three months of the year is much smaller than for the same period last year. Export values rose by 7.5% over the past 12 months, slightly faster than import values.

Returns seem to be returning

All in all, it is worth repeating the fact that returns for local investors are a lot better this year, especially after last year’s disappointment. The average balanced fund returned 8.5% year-to-date at the end of April (according to Morningstar), ahead of inflation. Global markets have rebounded from the late-2018 sell-off and local markets have followed higher, all of this ahead of the local elections. This highlights two points: global factors matter more than local political and economic developments for domestic investors. Two, waiting for certainty (in this case waiting for the elections outcome) before investing could mean missing out on a boost to returns. Markets turn long before there is clarity. The biggest impediment to wealth accumulation and preservation is therefore not market volatility or political uncertainty, but how investors respond to it.