Returns in perspective

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

The month ended on a fairly dramatic note after traders interpreted European Central Bank (ECB) President Mario Draghi’s innocuous comments, on the strengthening Eurozone economy, as signalling an approaching end to monetary policy stimulus. At the same monetary policy conference, statements by his Bank of England counterpart were also interpreted as talking up prospects of rate hikes. As a result global bonds sold-off, the euro and pound gained against the dollar and stocks also hit a wobble. But this does not appear to be a repeat of 2013’s ‘taper tantrum’ when markets sold-off sharply after then US Federal Reserve Chair Ben Bernanke suggested that stimulus could be pared back. While growth in Europe is indeed looking good, inflation remains very low – and is falling – and the ECB has no need to rush towards the exit.

Taking a slightly broader view, the half-year mark allows an opportunity to take stock of some difficult realities faced by local investors. The local economy remains weak and is technically in a recession, while there is widespread political uncertainty and anxiety over the implications of credit ratings downgrades. Compounding this situation, market returns over the previous three or so years have been disappointing, barely keeping up with inflation.

In terms of the last point, the most striking observations scanning across the main asset classes over the past year or so are: firstly, how well local government bonds have performed despite credit rating downgrades; secondly, how global equity markets have surged over the past 18 months in US dollar terms (but not in rand terms) after negative returns in 2015; and thirdly, how poorly local equities have performed in contrast.

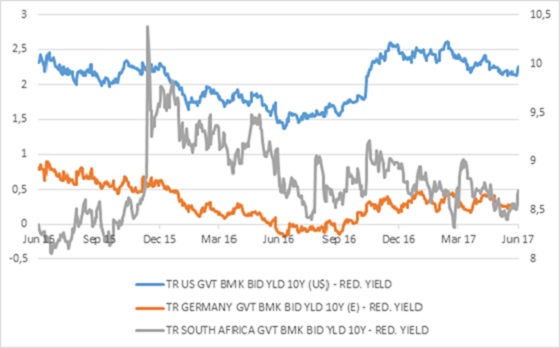

Local bonds did not escape last week’s global selloff but the All Bond Index returned 4.0% for the first six months of the year and 8.0% over the past 12 months, just ahead of cash (3.7% and 7.6% respectively). The10-year government bond yield initially declined from 8.5% at the start of the month before jumping to 8.7%. However, this is still below the 8.9% level at the start of the year. Therefore, investors have benefited from a high yield (much higher than available in developed markets and most major emerging markets) and some capital appreciation. Bonds rallied despite downgrades largely due to the fact that the downgrades were priced in already. Global demand for high-yielding emerging market debt remains high and inflation is expected to decline, which matters the most for local bondholders, helped along by a 12.0% year-on-year appreciation (5.0% year-to-date) of the rand against the US dollar.

Despite a somewhat turbulent end to the month, the US S&P500 is close to its all-time record high and returned 9.0% year-to-date and 18.0% over 12 months. US equities have responded to an improved global economic growth outlook, while a softer dollar allows multinationals to benefit. The prospect of corporate tax cuts is also still alive, though it is not believed to be a sure thing anymore. Other global markets have had a similarly strong gain over the past year (bearing in mind that the fall-out from the Brexit vote in June 2016 does create a very favourable base for one-year growth). The UK FTSE 100 returned 17.0% in pounds, benefiting from a weaker currency. Japanese equities delivered 31.0% in yen over the past year. And in continental Europe, where economic activity is enjoying a nice bounce, the Eurostoxx 600 Index returned 19.0% in euros over the same period.

Emerging market equities, which suffered negative calendar years in 2013, 2014 and 2015, returned 18.0% year-to-date and 24.0% over the past 12 months in US dollars. Despite outperforming developed markets over this period, emerging markets are still attractively priced relative to developed markets.

Local market has gone sideways

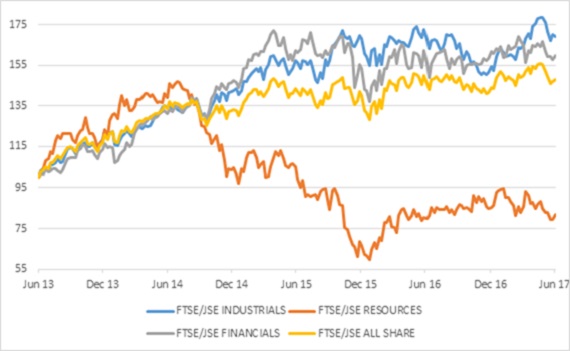

The FTSE/JSE All Share Index hit a record high closing price of 55,188 in April 2015 but at the end of last week, it was back at levels last seen in June 2014, after a 3.5% decline in June. In other words, over this three-year period, dividends have been the only source of return from local equities. There have been different drivers of the market over this period. As Chart 1 shows, from late 2014 there was a big divergence in the main sectors, with resources falling sharply and financials running ahead. In late 2015 financials fell sharply with the axing of Finance Minister Nene. Industrials, where the large rand-hedge shares are located, benefited from a weak rand in 2013 and 2014 but was held back by weak global markets in 2015 and a stronger rand from 2016 onwards. Resources turned in early 2016 as commodity prices bottomed but the rally ran out of steam at the start of 2017. This year has largely been an industrials story, driven by Naspers, British American Tobacco and Richemont, which have rallied in line with global markets. Both financials and resources are negative year-to-date.

Unlike in rand terms, the JSE All Share has almost kept up with global markets in US dollar terms in the past year, returning 13.0% compared to the MSCI World’s 18.0%.

The impact of the currency has become more pronounced on the local market. In the past, the main rand hedges were mining companies and Sasol. Today, not only is the JSE dominated by dual-listed global giants such as Naspers, but even some traditional ‘SA Inc.’ companies such as hospital groups, retailers and property companies have increased their offshore exposure. According to South African Reserve Bank data, South African companies invested R300 billion abroad over the past five years. This means the local economy has a much bigger built-in hedge against a weak currency. But it also means the exchange rate will have an even larger role in portfolio returns in the future, over and above the direct offshore portion. Given the unpredictability of the rand, this strengthens the argument for diversification.

Responding to disappointing returns

The net result of the above has been disappointing returns for investors. Local equities, where the bulk of most balanced funds invest in, have given below-inflation returns over the past year, while global equities have not contributed in rand terms. Does it still make sense to invest in a balanced fund? Many investors are considering moving into the stability of a bank deposit or want to take all their money offshore. Obviously everyone needs to assess their own risk tolerance with their financial planner but the general principle is to only change investment strategy when personal circumstances, not market conditions, change. Changes in market conditions call for tactical asset allocation shifts, which are best handled within a balanced fund.

Also remember that the global portion of most balanced funds (limited to 25.0% by Regulation 28) have performed very well in US dollars. This means that when the rand weakens again – which is bound to happen at some point – investors will benefit from a larger base of hard currency assets.

Given the weakness of the local economy, does it make sense for a balanced fund to have local equity exposure at all? In a typical balanced fund with around 40.0% local equities, exposure to domestically generated profits will only be around 20.0% of the entire fund, since more than half of JSE listed companies’ earnings are generated abroad. The return prospects for local equities have also improved, since the market now trades on a more reasonable valuation. The current forward price: earnings ratio of 14 (12 excluding Naspers) has historically offered an average annual real return of 4.0% to 5.0% in real terms over the next seven years. This is below the long-term average but decent. However, valuations have not reset to very attractive levels as in 2009 and 2011. This is another reason to retain a diversified portfolio – there are no valuation signals suggesting climbing boots-and-all into any single asset class.

The final general principle remains that appropriately diversified portfolios offer a more robust solution to a broad range of uncertain outcomes, than a concentrated portfolio that only delivers in a handful of outcomes. When it comes to markets, there are a lot of moving parts – politics, economic growth, exchange rates, fund manager performance – and obsessing about one area and ignoring others can be to investors’ detriment. It is our job to think about all these things, and build appropriately positioned strategies.

Chart 1: JSE All Share Index and major sectors, total returns rebased to 100

Chart 2: South African, American and German 10-year government bond yields, %

Source: Datastream