Return rundown

Returns over the past year have been nothing short of spectacular, and some are worrying that it’s been too much, too soon. So here is a whistle-stop tour of the main asset classes South Africans invest in. The conclusion is that return prospects for a diversified portfolio still look reasonable.

Ace of base effect

It’s worth reminding readers that most investment statements and fund fact sheets you will have seen recently are dated to the end of March. A one-year return will therefore be measured from the end of March 2020, which was close to the bottom of the crash in local and global equities and property, the rand, and local bonds.

The impressive growth numbers are therefore measured from this low point. However, there is no question that global and local markets have recovered strongly and even surpassed pre-pandemic levels. It’s only property that is not yet back to pre-Covid levels, which is unsurprising given the uncertainty around the adoption of ecommerce and the shift to working from home. As always, within each asset class there are many nuances and pertinent details.

Strong global growth

Let’s start with global equities. From a macroeconomic point of view, all the elements that continue to drive a bull market are still in place. The question is just whether the market has already priced this good news in (as it usually does), front-loading the returns.

The global economy is expected to grow at its fastest pace in decades this year. Again, this is from the low base of the lockdown-induced contraction last year. But most credible forecasts also expect 2022 growth to be robust. The most recent data we have – in other words, the situation on the ground now –is also very encouraging. To highlight just one statistic, the JPMorgan Composite Purchasing Managers’ Index jumped to 54.8 in March, with strength in both manufacturing and services. It’s the highest level in three years.

The fact that some equity indices, most notably the US S&P 500, are at all-time records is not a concern by itself. Equities are supposed to rise over time and therefore regularly set new records. The question is whether the current record is losing touch with the underlying economic reality.

One big concern from the global equity point of view is whether inflation and consequently interest rates will jump and not only choke off the economic expansion, but also cause equities to de-rate (reduce the price investors are prepared to pay for each dollar of expected earnings). This is because the decline in long-term interest rates during 2020 boosted price-to-earnings multiples. In simple terms, lower interest rates mean future profits become more valuable today. For those companies that have better long-term growth prospects – like the fabled Big Tech companies - lower interest rates delivered a bigger boost to their multiples.

It must be said though that some companies, notably banks, benefit from higher yields, while others benefit from the stronger sales growth in the climate that gives rise to higher yields. Nonetheless, the increase in long-term interest rates since the start of 2021 has therefore put a halt on the expansion in overall PE multiples.

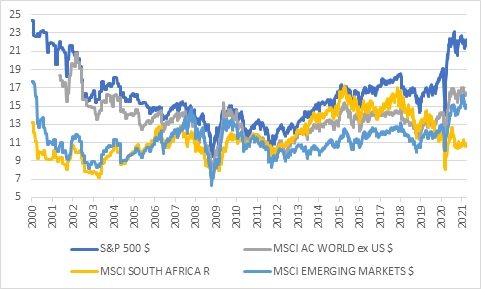

The US market has performed the best, and trades at the highest multiple (which is also historically the case). Its forward PE is high at 21, but has been roughly stable at this level for the past six months. The returns over this period have been from earnings growth, not because investors have been prepared to pay more for each dollar of earnings.

Outside the US, PE multiples are much more subdued, because other major markets have lagged the US. The 12-month forward PE on the MSCI All Country World Index excluding US is 15, lower than at the start of the year.

Chart 1: 12-month forward price: earnings ratios

Source: Refinitiv Datastream

Historically, there has been an inverse correlation between price-to-earnings ratios and subsequent returns over five years or longer. This suggests that the easy money has been made, especially in the US. However, these ratios can’t tell us about the shorter-term direction of the market in the next year or three. With the global economy in an expansion phase, returns should be positive as company profits can expand quickly.

Equity bull markets have historically been killed by overzealous central banks, the build-up of unsustainable imbalances or some external shock (such as a pandemic). The latter is inherently unpredictable. As for major global imbalances, speculative activity in SPACs, crypto, non-fungible tokens and ‘meme stocks’ don’t appear to have major systemic implications. Investors might burn their fingers, but not burn the house down. Household debt remains under control in the US and Europe, but the surge in government debt could have problematic implications years down the line. That leaves central banks.

The message from global central banks is that the current increase in inflation related to the reopening and base effects will be transitory. They plan to keep short-term interest rates low for an extended period of time. This pretty much guarantees negative real returns from cash in developed markets, but should support riskier assets as equities would still be attractive relative to cash and bonds.

Property still on good foundations

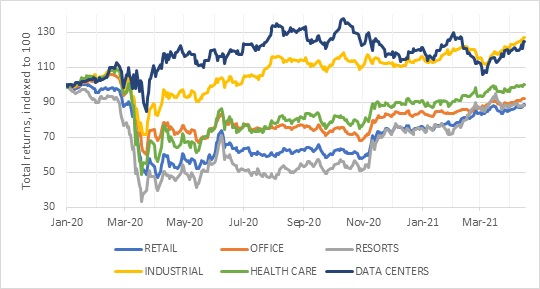

Global listed property has not fully recovered from the Covid-19 crash. The FTSE EPRA Nareit Developed Index is still dragged down by its office, retail and resorts subcomponents. The best performing categories have been data centres and logistics, both tied closely to the IT and ecommerce sectors respectively. On the plus side, valuations are reasonable with dividend yields above inflation (unlike bonds), debt levels are broadly speaking manageable and there has not been the kind of overbuilding that normally bedevils the industry. It therefore remains an attractive diversifier to global equity in an offshore portfolio.

Chart 2: FTSE EPRA/NAREIT Developed index subsectors

Source: Refinitiv Datastream

Local listed property, on the other hand, looks very cheap. However, the concerns about oversupply of office space and shopping malls are real, and local property is overexposed to these areas relative to global benchmarks. Companies are also still in the process of repairing their balance sheets. Complicating the outlook somewhat is that a large part of the local index is actually Eastern European. This brings some degree of diversification from the purely local sector, but it means JSE-listed property remains heavily concentrated in two emerging market regions: South Africa and Eastern Europe.

Local global and local local equities

Local equities, as we know, are also not quite “local”. The rally over the past year has been led by resources that have benefited from higher global commodity prices. Depending on how you slice and dice it, only about a third of the JSE counts as SA Inc. Strong global growth is therefore more important than the local growth outlook. Nonetheless, the “local local” shares can benefit from better economic growth in South Africa over the next few years. The previous five years have been so poor from a growth point of view that it will not take much to improve on them. Even with the resource-driven rally of the past year, the local market trades on a low PE multiple, certainly compared to global indices including other emerging markets.

This is partly because the mining shares are extremely profitable with current high commodity prices. These will not necessarily last. The other factor is that long-term interest rates remain very high, for reasons discussed below. If low long-term interest rates mean global equities can trade at high multiples, then the opposite should also apply to SA. However, any decline in long-term interest rates can boost local financials and retailers.

Either way, the FTSE/ JSE All Share Index might be at a near-record high but our preferred benchmark, the Capped SWIX, is still below its 2018 peak. In dollar terms, both indices are well below record levels. After a long streak of underperformance, there is no reason to believe the current rally can’t last.

Rand recovery

The rand is not an asset class, but it influences the relative performance of local and global asset classes, as well as the returns of domestic asset classes. A strong rand tends to be good for bonds and interest-rate sensitive shares, while a weak rand tends to boost the offshore plays on the JSE. At the end of last week, the rand had fully recovered its pandemic-related losses against the US dollar.

The rand has exhibited typical volatility, but has in fact moved sideways over the past five and a half years, contrary to the view that it always depreciates.

Beware Brazilians bearing bonds

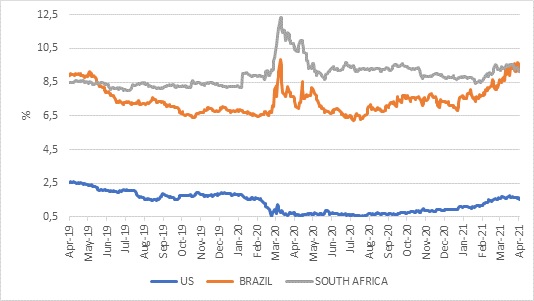

The main drivers of the rand are the direction of the dollar, US interest rates, commodity prices and sentiment towards emerging markets, with local factors less important. It normally tracks its commodity-producing emerging market peer group quite closely, but has outperformed them recently.

In particular, the Russian rouble and the Brazilian real have struggled since the start of the year. The rouble has been knocked by tensions with America, while investors are questioning Brazil’s commitment to economic reform and fiscal consolidation as the country is hit by a terrifying second wave of coronavirus infections. Brazilian bonds have also sold off, and the gap with South African long bond yields has closed.

Chart 3: 10-year local currency government bond yields

Source: Refinitiv Datastream

While inflation is rising in Brazil and its central bank has started hiking rates, South Africa’s inflation outlook is benign. Fiscal consolidation is so far going better than expected, but the real test lies ahead when salary negotiations with public sector unions kick off in earnest. Still, you’d expect our bonds to trade at lower yields than Brazil’s. The market does seem overly pessimistic and this presents an investment opportunity. Assuming inflation in line with the Reserve Bank’s 4.5% target over the medium term, 10-year South African government bonds offer 4.5% real yield.

Cash looks trashy

Finally, returns from cash are anchored to the Reserve Bank’s policy stance. When it cut the repo rate from 6% to 3.5% last year, money market rates soon declined to around 4%. So-called enhanced income or cash-plus products can hold instruments with a slightly longer duration, and therefore benefited from capital gains as shorter-term yields declined, while locking in the previous higher interest rates for a bit longer (no single instrument in a money market fund may be longer than one year). However, as instruments mature, they will have to be reinvested at lower yields and therefore investors should not expect recent attractive returns to persist. If they do, there is more credit risk in the portfolio than you think.

The Reserve Bank’s latest bi-annual monetary policy review report paints a picture of a muted inflation outlook, which suggests only a gradual rise in interest rates over the next few years. Things can change of course, but that is based on how it sees the world now. This suggests very low to negative real short-term interest rates for the next year or so. This is in contrast to the 2016 to early 2020 period when real short-term interest rates were high and investors could earn a decent real return from money market or cash-plus products without taking on risk.

In summary

In investment terms, this – return without risk - counts as a free lunch. Free lunches never last long. Therefore, investors will have to continue carefully weighing the outlook for each asset class, both risks and opportunities, and combine them in an appropriately diversified portfolio. Local assets are undoubtedly cheaper than their global counterparts, but come with a unique set of risks.

The average retail balanced fund returned 30.9% in the year to end March and 13% in the past six months, according to Morningstar. Clearly we shouldn’t expect a repeat performance over the next year or the year thereafter, but the combination of valuation (especially on local assets) and a supportive macro environment (especially for global equities and property) suggests that a balanced portfolio should outperform cash and inflation over the medium term.

The other point to note is that the long-term performance of such a portfolio is often made up of such shorter-term bursts, as the past year again demonstrated. Hence the importance of remaining invested.