Reducing the impact of tax on your investments

Hugo Malherbe, Executive of Product Development at PPS Investments.

Several tax changes have been introduced in recent years. This year, dividend withholding tax (DWT) was increased to 20%, tax brackets were not adjusted for inflation (only by 1%) and a 45% tax bracket was introduced. Last year, the capital gains inclusion rate was increased to 40% for individuals.

The impact on investment returns is becoming an important consideration for investors and smart investment decisions can boost returns.

Saving tax efficiently - long term

Retirement funds remain the best option for long-term savings, allowing contributions of up to 27.5% of taxable income up to a R350 000 limit. Provided investors reinvest the tax deductions received from SARS on contribution, retirement funds provide a tax-efficient option for long-term savings.

Tax free investment accounts also offer a tax-efficient way to supplement retirement savings due to compounded growth and no tax on income or gains, and no DWT being charged. Contributions to a tax-free investment account are limited to R33 000 per tax year and R500 000 in total, and cannot be replenished if withdrawn. The structure is therefore not ideal for short-term savings given the restriction on lifetime contributions.

Saving tax efficiently - short term

An investment option best suited to short-term savings (less than five years) is a normal discretionary investment. It provides unrestricted access to savings and investors benefit from interest exemptions and capital gains tax exclusions. Annual interest exemptions are R23 800 for those under 65 and R34 500 over 65, while the exclusion amount is R40 000 capital gain.

This benefit is best explained by example. If you own a R200 000 investment which earns 10% interest returns per year, the interest exemption will provide a significant benefit to after-tax returns if you consider that investors will be charged interest at their marginal tax rate. See table illustrating the impact of exemption on interest below.

And if you invest R250 000 in an equity unit trusts providing 12% growth per year (no dividends assumed for ease of example), and switch equity unit trusts yearly (realising gains), the capital gains exclusion provides a similar benefit on after-tax returns. See table illustrating impact of exclusion on gains below.

The regulator has indicated that interest and capital gain exemptions will not be adjusted for inflation going forward so while they hold value in the short term, the benefit will diminish in the long term. Retirement funds and tax free investment accounts are thus better options for long-term savings.

Alternative options

Investors that are already utilising their annual exemptions and exclusions or have sufficiently contributed to a retirement fund and tax free investment account, should consider the potential tax benefits of an endowment for investment terms exceeding five years.

An endowment is taxed in the hands of a life company and not the investor, removing any tax reporting responsibility from the investor. Tax is charged on the investment at 30% for income, 20% for DWT and the capital gains inclusion rate is 40%.This provides a tax-efficient option for investors with higher marginal tax rates and trusts where underlying beneficiaries are individuals.

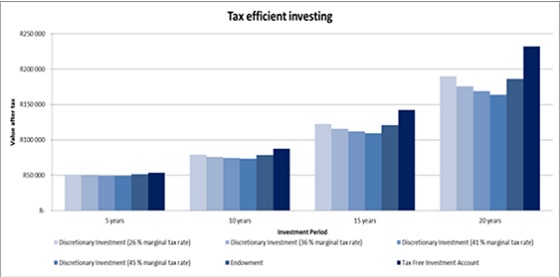

The graph below illustrates a R33 000 investment over four terms into discretionary investments for individuals with various marginal tax rates (exemptions and exclusions already utilised), an endowment and a tax-free investment account. The first graph illustrates the returns for an investment that earn 10% interest per year.

The benefit of a tax-free investment for long-term savings is clearly illustrated, with an endowment providing a benefit for individuals with higher marginal tax rates in the long term.

Suitable advice is of course important to ensure all decisions are made with clients’ financial situations and goals in mind.