Reassessing our love of cash

It is easy to forget how much the investment landscape has changed since the Covid-19 pandemic has made its presence felt. We have certainly seen (and continue to experience) extraordinary times. To understand how profoundly things have changed, it helps to consider what investors would have seen when looking back from 31 August each year, over the past three years, for various reporting periods.

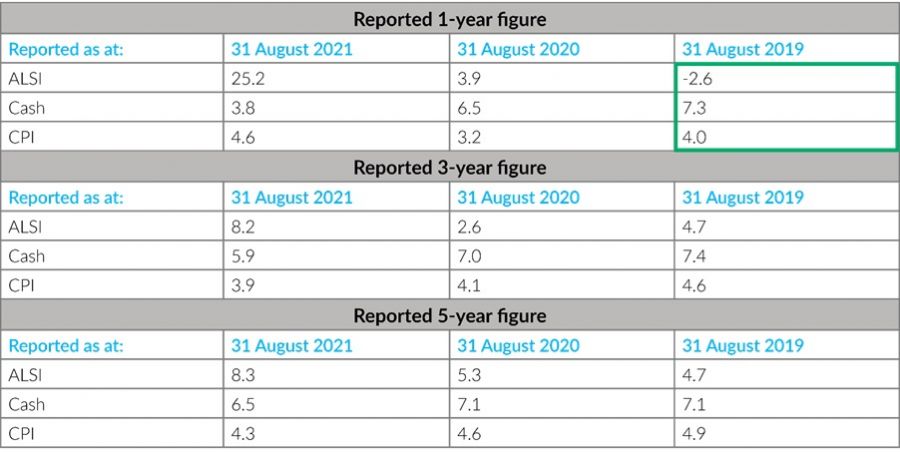

For example, an investor looking back in August 2019 deciding where to place their money, would have been faced with a negative return from local equities for the preceding 12 months, and a comparatively attractive (and inflation-beating!) 7.3% return from cash.

Over the 5-year period ending August 2019, putting your money in cash would have been the smart move, earning a 7.1% p.a. return, compared to 4.7% from equities. Why would any investor have wanted to take on the additional risk and volatility associated with an equity investment, when better returns were to be had at lower risk from cash?

Sources: PSG Asset Management and Morningstar. Synthetic CPI used to account for lag in CPI data. Annualised returns.

Of course, the hazards of reliance on past performance have often been pointed out. Fast forward to August 2021, and the picture looks very different. Local equities have delivered a stunning 25.2% return over the one year, while cash returns are lagging far behind at a paltry (and below inflation) 3.8%. Equity returns now also lead over cash over both 3 and 5 years, despite the impact of poor performance in previous years on longer-term cumulative return numbers.

For monthly contributors this picture looks even better as they bought into the market lows, lowering their entry price. In fact, trends in investment markets often reverse – which is why investment professionals often prefer to rely on long-term averages to guide their investment decision making (rather than a point-in-time) market snapshot.

Time to get selective about fixed income

Cash certainly has a role to play in most client portfolios. It provides much-needed liquidity to meet obligations, provides emergency funding and acts as “dry powder” while waiting to take advantage of market opportunities. However, cash was never intended as a long-term investment – as it tends not to outperform inflation by a significant margin, in the long run, making it a poor store for long-term value.

Unfortunately, the exceptional market conditions over the past few years have skewed South Africans’ perceptions of cash as an asset class. After all, for several years, sitting in cash was the ‘optimal’ investment decision and investing in equities (traditionally the preferred vehicle for long-term funds) delivered poor returns.

While money market funds may have been the first choice for many investors for a number of years, market conditions have changed. Following a cash-centric strategy, just because it worked over the years leading up to 2020, is sure to end in disappointment, not only for those with income generation needs but especially for long-term investors who have sought refuge in money market funds for the wrong reasons.

Considering the options

With interest rates likely to remain low, income investors would do well to consider diversified income type funds, as they are able to take advantage of fixed income assets further up the yield curve, and in some cases also equities (to a limited extent). Investors with longer-term investment horizons, however, should consider multi-asset funds, as these allow for a higher allocation to equities. Of course, there are also concerns about equities – with some pockets of both local and global markets looking expensive. However, we remain convinced there is value on offer to selective and patient investors, and that equities still make sense as part of a diversified portfolio.

South African investors have had something of a love-affair with money market funds over the last few years, and for some good reasons as highlighted above. However, in every relationship, there comes a time to reassess if the attraction is still as strong as it was at first, and for those invested in money market funds for the wrong reasons, now might be the time to take stock of where the ‘relationship’ is at.

The ‘right’ investment is one that suits your needs and goals and that fits in as part of a holistic portfolio. If in doubt, it is always best to consult a certified financial adviser, who can help you evaluate your investment ‘match’ objectively.