Rate hikes still loom

It was a busy week for central bank watchers. The US monetary policy body, the Federal Open Markets Committee (FOMC) reduced its monthly bond-buying programme by another $10 billion, and is set to completely end this programme by October. At that point its balance sheet will have increased to $4 trillion, reflecting the massive amount of bonds and mortgage-backed securities it bought in three rounds of quantitative easing (QE) since 2008. The FOMC’s statement reassured markets that interest rates will be kept low for a “considerable time” after the end of QE.

In practice, this suggests that the Fed Funds rate – the main policy interest rate – will remain at 0% - 25% until mid-2015, rising to around 1.5% by end 2015 and to around 3% by end 2016. This path was slightly steeper than the market expected but will depend heavily on how the FOMC reads the incoming economic data over the next two years. Fed Chair Janet Yellen has stressed that she wants a sustainable recovery in the labour market and the broader economy, and will not undermine that with aggressive rate hikes (unless forced to do so by substantially higher inflation). The Fed’s own projections show annual economic growth below 3% over the next three years, below historic averages.

Fed’s actions will reverberate around the world

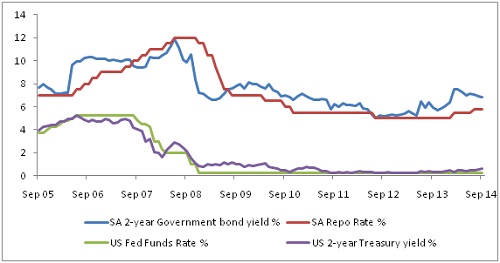

While the exact path of rate hikes in the US is uncertain, rates will rise and when they do, it will create potential problems in other parts of the world. Since virtually every financial instrument worldwide is directly or indirectly priced off the FedFunds rate, a shift – or expected shift – in the Fed Funds rate reverberates globally. Capital flows can change direction as investors reassess the returns they can earn for a given level of risk, and higher returns from safe US fixed interest assets will tempt many.

For Europe and Japan, where a weaker currency is welcomed and central banks are still adding, rather than withdrawing stimulus, shifts in capital flows are not much of a problem. The European Central Bank provided €82.6 billion in cheap loans to banks last week as part of its renewed efforts to spur credit growth and economic activity in the Eurozone. China’s central bank’s $80 billion liquidity injection into the major Chinese banks last week showed it is also in an easing phase, but the closed nature of the Chinese financial system means it is not really impacted by capital flows. It is the other parts of the emerging world that rely on external financing that are vulnerable. That brings us to the South African Reserve Bank (SARB).

No change to the repo rate

The context to last week’s Monetary Policy Committee (MPC) meeting is: South Africa’s current account deficit amounts to some R200 billion a year that needs to be funded by foreign capital. This deficit is large compared to our emerging market peer group. Our real interest rate, on the other hand, is low compared to our peers and history. The rand, despite having weakened substantially over the past three years, remains very vulnerable as a result. Inflation is above target (more detail below) and economic growth has slowed to a crawl. This is not an easy environment to conduct monetary policy, perhaps a contributing factor to Governor Marcus not making herself available for a second term at the helm of the SARB.

The rand is key

The SARB’s economists have downgraded their economic growth forecasts from 1.7% to 1.5% for 2014, from 2.9% to 2.8% for 2015, and from 3.2% to 3.1% for 2016. Their inflation forecasts are more or less unchanged, with lower oil prices being offset to a degree by higher anticipated electricity tariffs. The MPC also noted that expectation for future inflation, as measured by the Bureau for Economic Research’s third quarter survey, remained broadly unchanged at around 6%. Based purely on these forecasts, the case is strong for interest rates to remain unchanged. But this assumes that the rand remains fairly stable, and therein lies the risks. If the rand weakens substantially, it would almost certainly keep inflation above the 6% upper-end of the inflation target.

Higher real interest rates limit the likelihood of a speculative attack on the rand, and by weakening domestic demand, should help close the current account (a method used by the SARB in the past). Therefore, while the MPC did not hike rates last week, further hikes can be expected to be implemented gradually over the next year. In its own words, the MPC “is still of the view that interest rates will have to normalise over time”.

Chart 1: Policy and market interest rates, South Africa vs. United States

Source: Datastream

Inflation surprises in August

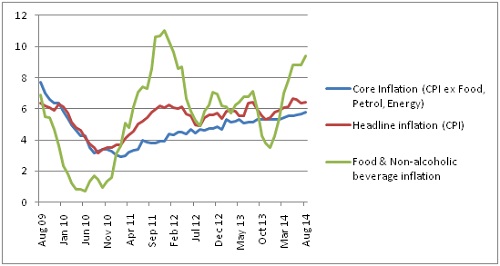

Consumer inflation unexpectedly rose to 6.4% year-on-year in August, from July’s 6.3%. The market expectation was for inflation to drift lower to 6.2%. Month-on-month the consumer price index (CPI) was 0.4% higher. Food and beverage inflation was the main contributor as it rose to 9.4% year-on-year from 8.8%, rather than moderating as was expected. Dairy, vegetables and meat prices rose fairly strongly during the month. In August, hot beverage prices rose by 2.1%. Bread and cereal prices also increased between July and August, but year-on-year inflation has slowed. Food inflation should slow in the months ahead, based on falling inflation at the producer level.

Lower petrol helping inflation

Petrol inflation continued to slow. Petrol prices were 5.8% higher in August compared to a year ago. After the price cut this month, annual petrol inflation should moderate to 2% in September. Based on the current average over-recovery of 13c/l, October’s petrol inflation rate could slow further.

The inflation rate of household appliances and equipment was unchanged at 4.1%. This suggests that the ‘first round’ impact of the rand weakness could be fading for certain items. Vehicle prices also rose at a faster annual rate of 6.4% in August. The gap between new and used vehicle prices widened further in August, with new vehicles costing 8.1% more than last year and used vehicles 7% less. The SARB forecasts inflation to average at 6.2% and 5.7% in 2015. The forecast for 2016 has increased to 5.8% due to the higher tariff increases granted to Eskom. Inflation is expected to fall below the 6% upper-end of the target range in the first quarter of 2015 instead of the second quarter as previously forecast. Falling used vehicle prices are limiting the extent to which dealers can raise new vehicle prices, illustrating how the weak economy and increased competition has resulted in a lower pass-through of exchange rate weakness.

Core inflation rose marginally to 5.8%, suggesting a limited – but persistent – ‘second-round’ inflation impact from the weak rand, as well as administered prices. Administered inflation excluding petrol and paraffin rose to 6.5% year-on-year from 6.4%.

Retail sales weak but not collapsing

In last week’s other notable local data release, real retail sales rose by 2.4% year-on-year, up from a revised -0.9% in June (previously 0%). Month-on-month seasonally-adjusted growth was 1.2%, up from -0.9% in June. The categories with the largest weights in the index are general dealers (39%) and retailers of textiles, clothing, footwear and leather goods (22%). Both were negative in June but growth turned positive in July, with the former growing by 2.3% year-on-year (from -1%), and the latter by 4.4% (from -1.9%).

The biggest annual decline was posted by specialist retailers of food, beverages and tobacco furniture, appliances and equipment, namely -0.5% in real terms due to higher food prices (growth was 6.6% in nominal terms).

Retailers of household furniture, appliances and equipment experienced very modest nominal growth (1.9%) and negative real growth (-0.3%). This chimes with the weak results recently posted by furniture retailer JD Group. The business rescue of Ellerines could lead to store closures and further declines in this category in the months ahead can be expected.

Outlook still uncertain

Overall nominal retail sales growth picked up to 8.5% year-on-year from 4.8% in June. This growth rate is slightly higher than the growth rates posted over the past year, implying that higher inflation is behind the slowdown in real sales. The pressure on household finances keeps building due to higher inflation, rising interest rates, as well as a general slowdown in job creation and income growth. Annual household credit growth is also below 5%. Retail sales growth is by no means strong, and the weakness of household spending is confirmed by other surveys and measures, including motor sales, convenience store sales, services and property. One notable area where South Africans are cutting back is in purchasing petrol. After accounting for fuel price increases, petrol sales have been declining for more than two years.

Chart 2: Local headline, core and food inflation

Source: Datastream