Public benefit organisations must guard against economic volatility with reserve policies

04 April 2014 | Investments | General | Alan Wellburn, Citadel Wealth Management

The funding environment for public benefit organisations is under pressure, yet building a reserve fund can help minimise risk during tough times.

In his recent Budget speech, Finance Minister Pravin Gordhan announced the relaxation of the part of the Income Tax Act requiring philanthropic foundations to distribute 75% of the money they generate within a year. While this will allow philanthropic foundations to invest their funds in a more sustainable manner and provide ongoing funds for the public benefit organisations they support, these organisations still have a responsibility to ensure that their funds receive the best growth and minimum exposure to risk.

This is the view of Alan Wellburn, Operations Manager of Philanthropy at Citadel Wealth Management, speaking at a recent seminar on the importance of PBOs managing endowments and reserves effectively, hosted by the company.

"The funding environment for public benefit organisations and NGOs is under pressure. Given this uncertainty, a well-managed reserve fund is a necessary component of an organisation’s sustainability strategy. In addition, both large and small organisations with an established endowment need to regularly revisit their reserve and endowment policy to ensure that the organisation’s exposure to unnecessary risk is minimised,” says Wellburn.

Wellburn says that PBOs have a duty to be responsible stewards of public funding and trust – this means managing finances wisely. "A reserve policy should clearly define how the reserve should be invested and how and when it can be used. An investment approach which takes into account both inflationary risk and volatility risk is essential.”

Wellburn explains that the below examples show how investment decisions can make a major difference to the size of a reserve over time. In this example, two organisations have R10 million in reserves. Organisation A puts it in the bank, while Organisation B invests it in a diversified portfolio.

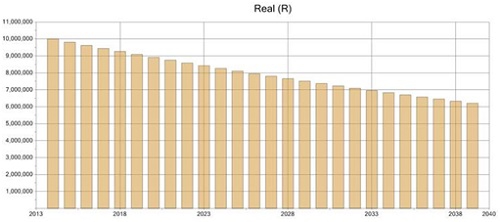

GRAPH A: Organisation A chooses an interest-bearing bank account. The interest on the R10 million (4%) in an inflationary environment like South Africa, is less than inflation at 6%. After 25 years, this reserve is only worth R6m in real terms. In other words, the purchasing power of the R10m reserve will be eroded by inflation and will be reduced to R6m, despite the interest earned.

Modelling assumptions: Inflation rate: 6%, Interest rate at bank:4%

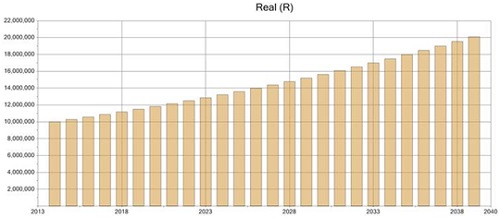

GRAPH B: The return over a 25 year period is more, at 9%, than the inflation rate of 6%. Based on a projection rate of 3% in excess of inflation, the value of their R10m reserve increases to R20m in real terms.

Modelling assumptions: Inflation rate: 6%, Projection rate: 3% in excess of inflation (9% nominal)

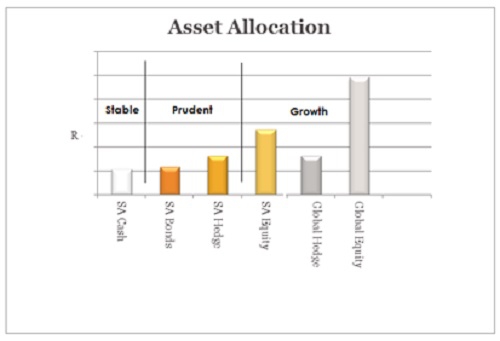

"In addition, cash-flow modelling is used to make sure an organisation has access to its capital if needed (short-term liquidity) as well as long-term growth (to stay ahead of inflation). Knowing what cash will be needed, and when the two major portfolio risks of inflation and volatility can be managed over time, is vital. This is achieved by allocating the reserve fund to three broad risk categories of stable, prudent or long term growth” says Wellburn.

GRAPH: Allocate specific amounts to the underlying funds within each investment category to provide real investment growth and protect against volatility over time.

Wellburn cautions against diversification if hedging is not applied. "Whilst offshore diversification can have a very positive effect on a portfolio, the fluctuating value of the Rand can have a significant effect on returns. Reducing currency risk through hedging, a technique to guard against foreign exchange fluctuations is a way to manage this risk.”

Wellburn acknowledges that building up a reserve can be a challenge in tough economic times, yet there are ways around this. "Operate at a small surplus each year and invest any of the surplus, rather than spend it in the following year. Although this requires a level of financial discipline, it is a strategy that pays dividends in the future. Another good source for funds for a reserve is unrestricted funding such as legacies, bequests, individual giving and self-generated income. Lastly, investment income (interest or dividends) generated by investing larger grants until the funds are needed for project implementation is a great source of reserve funding.”

Wellburn concludes with the two most common myths about reserves:

Myth: Having a reserve discourages funders because they think the organisation has enough funding.

Reality: Most major funders prioritise the sustainability and impact of the organisations they support and prefer grantees to have a reserve. Many specifically look for organisations that have enough in reserve to cover at least 3-6 months’ operating costs.

Myth-buster #2

Myth: It is more responsible to keep funds in the bank, rather than to risk it in an investment vehicle.

Reality: Funding not being used for immediate operating expenses that is kept in a bank account is losing value over time due to inflationary risk. Investing in the stock market can also be a risk due to short term fluctuation. Selecting an investment strategy that takes into account both of these risks so that surplus funds will grow over time and stay ahead of inflation is essential.