Portentous 2014 developments

After persistent trends and low volatility since the financial crisis, 2014 presented market dislocations and structural changes that we believe have important implications for the course of financial markets, whose participants seem somewhat complacent since ‘momentum’ has been the winning strategy for so long. We highlight some of these dislocations and changes below.

The US passed on the QE baton

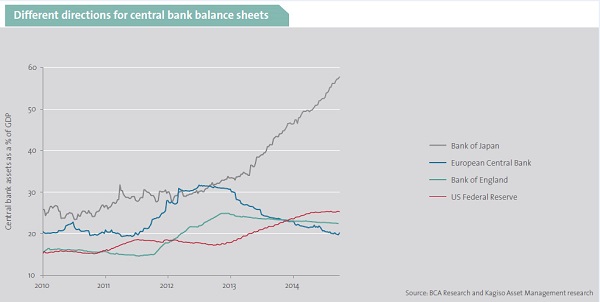

Quantitative easing (QE), injecting liquidity into the economy via the purchase by central banks of financial instruments from the private sector, has been executed on a grand scale since the financial crisis (see chart below) - at a time of near zero interest rates in the world’s largest economies.

The US Federal Reserve has purchased US$3.7 trillion between November 2008 and October 2014 (QE3’s conclusion). The magnitude of this intervention is staggering, given that the US economy (GDP is US$17.6 trillion) and bond market (103% public debt: GDP) are the world’s largest. The real economy benefits of US QE have, in our view, been mixed and of diminishing effect through time, but the impact on asset prices has been massive.

In 2013, the Bank of Japan began its enormous QE programme and the European Central Bank tentatively began asset purchases in 2014, with widespread expectations of significant sovereign bond purchases to come. This significant structural change highlights the better state of the US economy and has precipitated a sharp strengthening of the US dollar against the yen and the euro. The net effect should be a tightening of global liquidity conditions, given the relative magnitude of the QE programmes, which should be negative for asset prices.

Foreigners began selling SA bonds

After many years of foreign inflows into our bond market, foreigners sold R71.7 billion of bonds in 2014. Coinciding with these outflows, the rand depreciated by 9.3% (to the US$) to its worst level since 2001. Receding foreign liquidity will make our government’s budget deficit more difficult to finance.

Emerging market equities also saw foreign outflows of US$25 billion in 2014, while, in contrast, foreign equity inflows into SA, at R13.3 billion, were positive. However, this may have had more to do with internal problems in our emerging market peers (Russia, Brazil, Turkey, Thailand) than the absolute prospects for our companies.

China’s economy decelerated further

Having grown GDP at rates of 8%-10% pa for over a decade (slowing to below 8% in 2013), China’s growth rate headed towards the 7% level in 2014. Growth is likely heading lower as the economy needs to absorb excess capacity, deleverage and rebalance away from fixed investment. China’s property activity slowed in 2014, housing prices declined and new residential construction fell. Limited fiscal policy (infrastructure investment) and monetary policy (lower bank reserve requirements and an interest rate cut) stimulus measures were introduced.

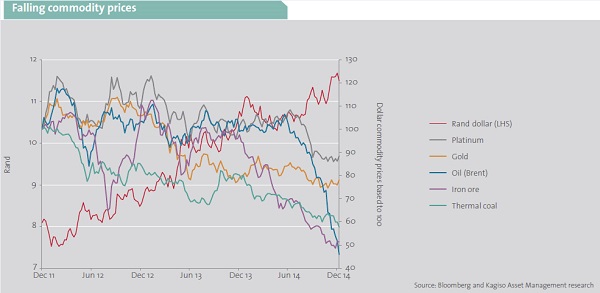

Commodity prices fell sharply

The growth deceleration in China, the world’s largest non-oil commodity consumer, came as 2014 saw an increase in supply of many of the commodities it imports. The result was large commodity price falls, with iron ore and oil prices almost halving and thermal coal down 22%. Precious metals were little changed in 2014 off already low levels as supply was curtailed.

The oil price decline is particularly important for the world economy as it is the largest commodity traded by value. The cause of the price decline was increased production from North America at a time of weak demand from Europe and China and growing use of substitutes (natural gas and renewables), with OPEC making no change to their production intentions.

These material commodity price declines will have significant implications for their respective consuming and producing countries and companies. Iron ore producers, eg Brazil and Australia, will see export revenues decline. Large net oil exporter economies such as Saudi Arabia, Russia, Nigeria, Angola, Columbia, Mexico and Venezuela will struggle as they are very concentrated around oil production. Oil price falls will particularly benefit large net importers, such as Europe and Japan.

South Africa’s exports are dominated (roughly 60%) by iron ore, thermal coal, platinum group metals and gold, while oil makes up some 20% of imports. The large relative oil price decline should result in a slightly positive trade balance impact and, together with lower maize prices, will dampen price inflation, enabling the SARB to raise rates more slowly.

In South Africa

Local developments of particular importance for financial markets were:

• the start of the SARB rate hiking cycle;

• National Treasury announcing ‘austerity measures’ in its October mini-budget in the form of an expenditure ceiling and imminent tax rises;

• major splits in organised labour with the NUMSA expulsion from Cosatu and the emergence of non-aligned AMCU, whose perceived success with its platinum mine strike is fuelling a major recruitment drive from established unions in various other sectors; and

• the demise of African Bank Investments, which should serve to reduce the extortionate returns earned by unsecured credit providers in SA, to reorganise the furniture retail industry and to remind bond and preference share investors to consider credit risk.

Given these structural changes, 2015 has begun with raised market volatility and our clients’ portfolios are therefore positioned for a very different environment to the one that has prevailed in recent years.