Polls, policy and petrol

Politics dominated the global market agenda last week, with the US mid-term election front and centre. For once, things went more or less according to script. President Trump’s Republican Party retained the Senate, the upper house of the Congress, but ceded control of the House of Representatives to the Democrats. This is a recipe for political gridlock, but it seems to suit most investors as it is likely to rule out major unsettling policy changes until the 2020 elections.

Global markets continue to recover from the October slump and jumped following the election. Unfortunately, the JSE’s November rally has lost steam, largely due to fresh declines in the Naspers share price, in turn due to Tencent falling in the Hong Kong market. But the local market is still positive in the month, which, given how terrible this year has been, says something.

Interestingly, the US market has historically performed strongly in the year following the mid-term election. The Wall Street Journal reports that the S&P 500 has delivered positive returns in the 12 months after the mid-terms every time since 1946, regardless of which party performed better, with an average return of 15%. It is not exactly clear why this is the case though, but if enough investors believe this time will be no different, then it won’t. But in general, it is better to focus on the underlying economic reality – which is still healthy – and sticking to a long-term strategy rather than trying to follow patterns.

Rates and trade

With the mid-term polls out of the way, attention is likely to return to other policy issues, namely US-China trade tensions and interest rates. On the latter score, the US Federal Reserve kept rates unchanged at its monetary policy meeting last week. This was as expected, but a hike in December is still likely given the Fed’s assessment that the US labour market has “continued to strengthen and that economic activity has been rising at a strong rate”. Importantly though, actual and expected measures of inflation remain stable around 2%, suggesting no need to accelerate rate hikes.

President Trump has of course complained bitterly about the Fed’s interest rate hikes, going as far as calling them “crazy”. This is highly unlikely to dissuade the Fed, whose independence is fiercely guarded. It is not the only central bank facing pressure from the government of the day though. The perceived lack of independence of the Turkish and Argentinian central banks was a key reason why these countries saw their currencies slump earlier this year. Turkish government bond yields which traded at the same yield as South Africa’s two years ago are now almost twice as high. More recently, the governor of the Reserve Bank of India (RBI) has clashed with the Indian Prime Minster over how much autonomy the RBI should have.

The other big uncertainty remains China-US trade relations. Ironically, Trump’s hard-line views on trade with China have always been closer to the Democrats than to his own party. It is an open question whether the election outcome will change how he approaches the trade war he launched. Despite the imposition of a range of tariffs on Chinese goods, America’s trade deficit with China has actually increased. In September it was $37 billion, the largest monthly deficit on record excluding March 2015 when trade was impacted by a strike at key US ports.

It is clear that trade tensions had a big impact on equity markets this year. New announcements of tariffs have seen markets sell off, while signs of a thaw in the relationship between China and the US have seen markets rally. The main thing is that trade tensions don’t escalate further. The impact of existing tariffs would have largely been priced in already. Trump and Chinese President Xi are scheduled to meet face to face at the G20 summit later this month. A comprehensive deal is unlikely, given the scope of the dispute, but any progress would be positive for markets.

Rome wasn’t built in a day

Speaking of unlikely deals, there is no sign of resolution in the stand-off between the new populist government in Italy and the European Union (EU). The EU has rejected Italy’s budget proposal, but Rome has insisted it won’t budge. The negative market response has seen the Italian government’s borrowing costs double since the March election. In absolute terms, Italian yields are still low around 3.4%, but given a 131% debt-to-GDP ratio, the margin of error is small. Compounding the situation, Italy’s economy stagnated in the third quarter as a promising increase in economic activity seems to be petering out. As we know only too well in South Africa, economic growth is a key ingredient in long-term fiscal sustainability.

Oil’s well that ends well

Elsewhere in the realm of geopolitics, the US sanctions of Iran have come into effect, but the oil price is down almost 20% from its recent peak. The decline is partly because eight countries have been given a temporary exemption by the US, including the biggest importers of Iranian oil, but also because oil production elsewhere has surged, spurred on by rising prices.

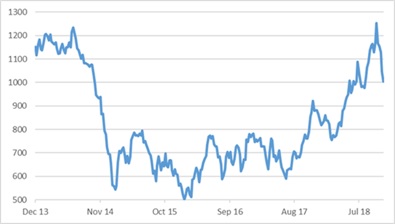

The lower oil price is good news for the world economy, particularly oil-importing emerging markets who faced the double whammy of a rising price and weaker currencies during the course of the year. In the case of South Africa, the rand price of crude oil shot up from R824 per barrel in January to R1 263 in early October and is now back at R1 000.

As a result, the price of unleaded petrol in Gauteng increased from R14.45 per litre in January to R17.08 currently (with an increase in the fuel levy along the way). Also helping is that the rand is somewhat firmer. The average rand-dollar exchange rate was R14.50 in October but R14.21 in November. All this adds up to a current R1.49 per litre over-recovery on the petrol price, and potentially a sizable cut in December, which would provide a boost for holiday season consumer spending. It also buys the Reserve Bank’s Monetary Policy Committee time to monitor both the inflation and growth outlook. A rate increase at next week’s meeting, the last for the year, is therefore unlikely. Given the still-fragile state of the domestic economy, every bit of good news helps.

Chart 1: Global equity indices in local currencies, rebased to 100

Source: Thomson Reuters Datastream

Chart 2: Rand per barrel price of crude oil

Source: Thomson Reuters Datastream

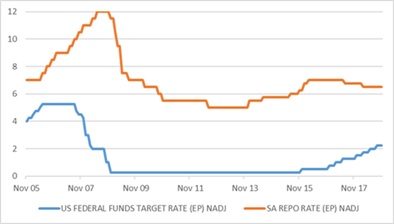

Chart 3: SA and US policy interest rates, %

Source: Thomson Reuters Datastream