Policy environment still positive for markets

Izak Odendaal, Investment Analyst at Old Mutual Wealth.

The Federal Reserve System marked its 100-year anniversary as the central bank for the US last week. It consists of 12 regional banks and a Washington-based Board of Governors (headed by Janet Yellen). Monetary policy is set by the Federal Open Markets Committee (FOMC).

Inflation forecasts cut

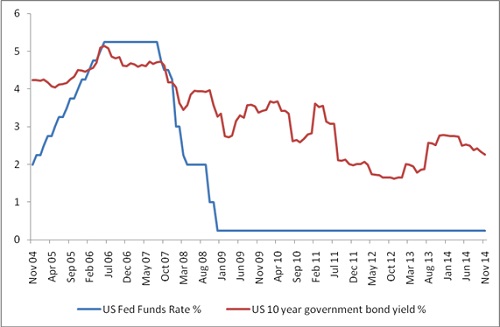

One of the regional banks, the Federal Reserve Bank of Philadelphia, publishes the Survey of Professional Forecasters, which last week showed that inflation is expected to stay below the FOMC’s 2% target throughout 2016. Forecasts were cut from 1.8% to 1.5% in 2014, 2% to 1.8% in 2015 and 2.0% to 1.9% in 2016. If this pans out as expected, there is little reason for the FOMC to jump the gun on interest rates. It would certainly take some time for US interest rates to turn positive in real terms. Although it is no longer buying bonds and mortgage-backed securities (quantitative easing), the Federal Reserve’s (Fed’s) overall policy stance is accommodative. In an apparent return of the “conundrum” identified by former Fed chairman Alan Greenspan, long-term interest rates have been falling in the US, instead of rising in anticipation of higher short-term rates. The yield on the 10-year Treasury is currently around 2.3%, having started the year at 3%.

The much older Bank of England has kept interest rates at 0.5%, the lowest levels in 310 years. Despite the UK economy doing quite well, expectations of the first rate hike are gradually being pushed out.

The Bank of Japan’s (BoJ’s) had zero interest rates for most of the past two decades and is now taking a leaf from its 1932 playbook, when it was the only major central bank to adequately respond to the Great Depression by funding the government deficit and pushing down the yen. The BoJ recently increased its quantitative easing programme to some $700 billion per year. As a percentage of the economy, the BoJ’s balance sheet is now the largest by far globally.

Hiking too early

Sweden’s central bank, the Riksbank, is the oldest and was established in 1668. The Riksbank, which sponsors the Nobel Prize in economics, learnt the hard way that premature hiking of interest rates on the grounds of financial stability is costly. It was the first western central bank to hike rates from 0.25% to 2% after the financial crisis in 2010. With inflation now hovering around zero, the Riksbank was forced to cut again and rates reached zero last month.

The youngest major central bank, the European Central Bank (ECB), was created along with the European Monetary Union. It is unique in having to set monetary policy for a diverse group of economies that share a single currency but not much else. The ECB has performed poorly in achieving its 2% inflation target, but this is largely a function of the incomplete institutional set-up and the fact that Germany holds so much sway. The Germans are fiercely opposed to anything that smells like money printing, i.e. quantitative easing. But ECB President Mario Draghi appears to be laying the groundwork for a proper round of quantitative easing, saying in a speech last week that purchases of government bonds would be considered. The current plan of buying corporate bonds and extending cheap loans to banks is not likely to amount to much since the European corporate bond market is small while banks are generally repaying old ECB loans and not taking out new ones (a case of leading the horse to the water).

Our own Reserve Bank, founded in 1922, kept interest rates at 5.75%. Although short-term interest rates have risen from 5% at the beginning of the year, they are still at levels last seen in the early 1980s. In real terms, the repo rate is still marginally negative. In this regard, South Africa is more like a developed economy than the emerging economies (read more below). Interest rates in several key emerging markets have risen (Brazil, Russia, Indonesia) but for the most part, the outlook for global interest rates and monetary policy more broadly, is to remain very accommodative.

Fiscal policy improving

The other side of economic policy is fiscal, which relates to the taxation and spending plans of the government. When economies are depressed and credit growth lacklustre despite interest rates at zero, expansionary fiscal policy (i.e. increased government spending or lower taxes) is theoretically the best option for recovery. But since 2010, large parts of the world have been gripped by the fear of exploding state debt and attempted to balance budgets by cutting spending and hiking taxes. This caused substantial economic pain, which loose monetary policy was only partly able to offset.

The impact of tighter fiscal policy is fading. In the US, the budget deficit was closed sharply from 9% of GDP in 2010 to 3% currently. However, recently government spending started adding to, rather than subtracting, economic growth. Europe, France and Italy recently had their budgets approved by the European Commission despite Germany’s objections that the deficits were too large.

In Japan, the sharp consumption tax increase in April has pushed the economy back into recession – the fourth in six years. The follow-up tax increase scheduled for next year has now been postponed to 2017 (pending a snap election).

Therefore, while global growth disappointed relative to expectations in 2014, the policy environment - both fiscal and monetary - looks set to be somewhat supportive in 2015. Along with the consumption boost from lower oil prices, this points to improved growth for next year. In such a scenario, the climate for risk assets such as equities should remain favourable.

South Africa forced to act

In South Africa we are not so fortunate. Years of running deficits means that interest payments are starting to crowd out other areas of spending, while the market and ratings agencies are increasingly asking for greater fiscal discipline. Our Treasury is being forced to close the deficit despite a weak economy and the Reserve Bank is under pressure to hike rates (albeit gradually).

Chart 1: US short and long-term interest rates

Source: Datastream

Rates and inflation unchanged

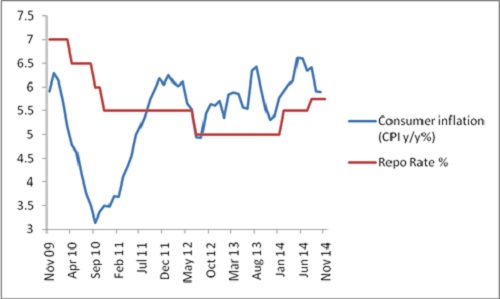

Consumer inflation was unchanged at 5.9% year-on-year in October, according to StatsSA data released prior to the Monetary Policy Committee (MPC) meeting. This was in line with market expectations. Inflation has fallen into the Reserve Bank’s target range earlier than expected, after spending six months above target.

Food inflation lower

Food and non-alcoholic beverage inflation declined further from 8.5% to 7.8% year-on-year. All food items showed slower price gains over the twelve months to October, except fruit prices. Falling inflation at the producer level, particularly grains and cereals, suggests food inflation should continue slowing. Inflation of alcoholic beverages accelerated in October from 5.3% to 6.3%, led by spirits and beer.

Because of a large petrol price cut in October 2013, annual petrol inflation rose to 2.4% from 1.1% in September. However, it should slow to 1.4% in November and turn negative in December (based on the current average over-recovery of 71c/l). Vehicle prices rose at a slower annual rate of 5.7% in October from 5.9%. New vehicle prices rose 7.2% year-on-year and used vehicle prices fell 7.9% in October. The decline in used vehicle prices is putting a lid on the consumer price increases of new vehicles, despite the imported prices of new vehicles rising by 11%.

In terms of items with high import content, the inflation rate of household appliances and equipment was lower at 3.1% compared to 3.3% in September. This suggests that the ‘first round’ impact of the rand weakness is generally fading (but not for all items: clothing and footwear inflation picked up to 5.9% from 5.5%). Core inflation rose marginally to 5.8%, suggesting a limited – but persistent – ‘second-round’ impact from the weak rand.

MPC meeting: lower growth and inflation expected

The Reserve Bank’s economists cut their forecast for economic growth in 2014 to 1.4% and to 2.5% and 2.9% for 2015 and 2016 respectively. Despite the growth outlook being downgraded at every single MPC meeting since September last year, the MPC statement emphasised that growth could continue to disappoint even these reduced forecasts.

The Reserve Bank’s forecast for headline inflation is also lower since the previous MPC meeting, mainly due to lower global oil prices. Inflation peaked in the third quarter at 6.5% and is expected to average 6.1% in 2014, 5.3% in 2015 and 5.5% in 2016.The forecast for core inflation, by contrast, is more or less unchanged.

Risks to inflation outlook are now judged by the MPC to be “balanced” rather than to the upside. The potential for rand weakness remains a big risk, as does above-inflation wage settlements. As the MPC noted, the extent to which higher US interest rates are already priced into the exchange rate is unclear. On the other hand, lower food and energy inflation, supported by lower global commodity prices, should keep headline inflation in check. A weak economy also limits price increases. Tighter fiscal policy in turn adds to economic weakness.

While the repo rate was kept unchanged at 5.75%, Governor Kganyago again emphasised that rates would have to normalise over time. This has been the MPC’s mantra all year, but only 75 basis points of hikes have materialised. The other interesting question is that if inflation continues falling, the normalisation will take place in real terms. If inflation surprises by falling to, say 4.75%, the real repo rate will be 1%.

Chart 2: SA inflation and interest rates

Source: Datastream