Pockets of Opportunity in Europe, Emerging Markets

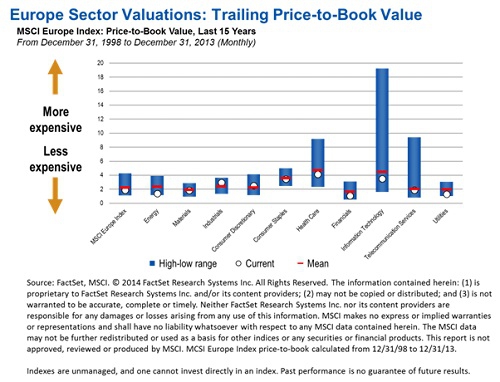

In early 2014, there seemed to be a few more areas of concern than we saw in late 2013. There has been some questioning of the stability of the US economic recovery, and of course, worries about prospects for emerging markets. That said, we are still finding plenty of reasons to be optimistic about the global equity outlook this year, and we are still finding values. We feel confident enough in the story of the US economic recovery from the 2007–2009 financial crisis that it almost sounds strange to us to still call it “recovery.” It feels pretty stable, considering the revival we’ve seen in the housing market, the improvement in household incomes, the deleveraging on the private sector side, and the impressive amounts of cash US corporations have on their balance sheets. That being the case, US valuations have come up, and while we still like the United States, as value investors we feel more strongly about European equities. European equity markets also performed well in 2013, but according to our analysis, Europe appears generally more compelling than the United States in terms of where earnings are, where margins are, and the amount of catch-up European companies continue to do in relation to the United States.

As our team comes together to discuss opportunities for our portfolios, we still feel that the most compelling opportunity set lies in Europe. We have been particularly interested in European financials on the equity side for a number of years, beginning at a time when it was considered quite contrarian. While not as inexpensive as they were a few years ago, we think there is still plenty of value in European financials, as some European banks are still trading below one times book value. A large French bank is one example of the kind of value we are seeing today. The company has rebuilt its capital base and has been paying back shareholders through dividends. Today, it has a sizable amount of excess capital on its balance sheet and has been bolstering holdings in existing subsidiaries throughout Europe.

Additionally, cash on balance sheets is generally high for many companies both inside and outside of the United States, and we think many companies may funnel some of that cash into technology. When we see heightened volatility in the economy overall, it can keep CEOs on the edge of their seats, hesitant to commit to spending. However, as we look at technology, on the hardware side, PCs and desktop technology are aging; the average age of equipment is quite high. While PC sales have fallen off a cliff due to sales of tablets and other devices, we have seen a lot of data to suggest that we should see some PC replacement coming through. And, as companies become more cloud-based, it should bode well for companies engaged on the software and service side.

We also continue to like pharmaceutical companies, which have rerated to some degree over the past year or so—that is, awarded a higher earnings multiple—but believe they still do not fully reflect secular tailwinds ahead such as aging demographics in many countries, the implementation of the Affordable Care Act ("Obamacare”) in the United States, and growing numbers of health care users in emerging markets. In some cases, we’ve been shifting our focus from large pharmaceutical stocks to biotechnology and healthcare equipment companies.

Lastly, energy is an area that’s been fairly contrarian. Yet, our analysis shows that oil service companies are being penalized for, and their valuations reflect, near-term supply and demand dynamics without consideration for numerous longer-term trends, which we believe could support sustained growth of oil services. More deep-water discoveries, the shale revolution and fracking, oil sands and the increasing importance of national oil companies all portend a higher concentration of oil services over time, in our view.

When we look at allocations, our equity and fixed income teams consider and discuss the respective asset classes from a bottom-up perspective with a view to how rich we believe the opportunity sets are in the respective markets. Valuations in the respective asset classes are fundamental to defining opportunity, and both the Templeton Global Equity Group and the Franklin Templeton Fixed Income Group maintain disciplined investment frameworks that they rigorously apply with a patient willingness to be contrarian. We think the ability to move freely between asset classes as the opportunities and/or risks present themselves through an active, unconstrained approach is key.

On the equity side, we continue to be enthusiastic about what we’ve seen in Europe. However, as emerging markets have come down over the past couple of months, we believe they could be the next pocket of opportunity for us as Europe turns the corner and its recovery matures. There are investors who are upset about what’s happening in the emerging markets; naturally, investors want to see all markets go up at the same time. But we tend to be contrarians, so when we see markets pulling back, we roll up our sleeves in search of opportunities. However, we also believe it’s critical to be stockpickers in emerging markets as not all fundamentals are equal. The markets are what we might call bifurcated, and so are the potential opportunities.

Lisa Myers’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. The risks associated with higher-yielding, lower-rated debt securities include higher risk of default and loss of principal. Focusing on particular countries, regions, industries, sectors or types of investment from time to time may subject one to a greater risk of adverse developments in such areas of focus than investing in a wider variety of countries, regions, industries, sectors or investments. Current political uncertainty surrounding the European Union (EU) and its membership may increase market volatility. The financial instability of some countries in the EU, including Greece, Italy and Spain, together with the risk of that impacting other more stable countries may increase the economic risk of investing in companies in Europe. Investing in derivative securities, such as swaps, financial futures and option contracts, and use of foreign currency techniques involve special risks as such may not achieve the anticipated benefits and/or may result in losses.