Past, present and future

September is Heritage Month in South Africa. As a diverse but also divided society, building a shared view of our heritage is very much a work in process. Nonetheless, all South Africans have an interest in sharing in a more prosperous economy with more jobs and less poverty. So what is South Africa’s financial and economic heritage, and what can this tell us about our future?

Inequality

The defining characteristic of the South African economy is extreme inequality of wealth and income, among the worst, if not the worst, in the world. This inequality still has a strong racial dimension to it even three decades after apartheid was abolished. This is visible not only in the data, but also with the naked eye.

In response, South Africa has a progressive tax system, which means the more you earn, the more you contribute proportionately. From this income there is substantial redistribution in the form of social grants (which are very effective in reducing abject poverty) and public services such as near-free health and education (though the quality is very uneven and often poor).

Unemployment

However, none of the post-1994 policies have succeeded in reducing unemployment, which is a key reason why inequality is high. The income gap between any two people will by definition be large if one person earns nothing. And without an income it is almost impossible to accumulate assets that appreciate over time such as a house or a pension. Poverty is then transferred from one generation to the next.

Unemployment reached a record high of 34% in the second quarter of this year on the narrow definition that excludes discouraged job seekers. Unemployment among young people is much higher. It remains a crisis, and as in many other countries, both unemployment and inequality were worsened by Covid-19.

Chart 1: South Africa unemployment rate, %

Source: Stats SA

Related to the above, a notable feature of the local economy is spatial inequality. South African cities are still scarred by apartheid urban planning, which put black people on the outskirts, away from economic opportunities. Today, it is still usually the case that the poorer you are, the further away you live from where the jobs are. Urban low-income workers often spend around a third of their wages on transport, often in the form of crowded minibus taxis. For the unemployed, the cost of looking for work can be prohibitive, which is probably a key contributor to high unemployment.

Other emerging markets like Brazil and India have much lower unemployment rates even though they share many of the same problems we do, including underperforming schools and inefficient state bureaucracies. But the poor in these countries are not physically separated from economic activity to the same extent. At a macro level, spatial inequality together with poor public transport also act as a massive drain on productivity as well as wellbeing.

Transport constraints

The other spatial legacy is the fact that Gauteng, our industrial heartland, is hundreds of kilometres away from the nearest port. In almost every other country, major industrial centres are located next to a navigable river, lake or the sea. This is because transporting goods on water is significantly cheaper than doing so over land. In fact, the only river in South Africa that is navigable by cargo ships is a very short stretch of the Buffalo River in East London.

Industry in South Africa largely developed around the gold mines, hence Gauteng’s inland location. This drives up transport costs substantially, negatively impacting global competitiveness. Overcoming this requires top-notch rail networks, but South Africa has not invested nearly enough in rail freight, partly because it is a state monopoly. The dominance of key network industries including electricity, rail, ports, telecoms, and air travel by state-owned enterprises (SOEs) stretches back decades and is a major constraint to economic growth today. This seems to be changing, however. Transnet announced that it is working on ways of allowing private players to operate trains and port terminals. Eskom is also steadily losing its monopoly on power generation.

A place of gold

Speaking of the gold mines, the next obvious feature of South Africa’s modern economic heritage is our dependence on windfalls in terms of mineral resource discoveries and global commodity price swings. This took off with the discovery of diamonds in 1871 in what is now Kimberley. Fifteen years later, the Witwatersrand gold rush would turn South Africa (then a region, not a country) from a backwater to an important cog in the global economic machine. After all, in those days the world ran on the gold standard and gold was money.

A century and a half later, South Africa is no longer the leading producer of gold or diamonds. Gold production peaked in 1985 and has declined steadily as ore bodies have been mined out. Gold is still a major source of export revenues, but its impact on the local economy and its financial markets are nowhere near where they were in the first hundred years. Today platinum group metals and coal dominate exports, as well as iron ore. South Africa is also the largest producer of chromium and manganese, and export sales have increased substantially over the last few years.

The share of mining in our total economic activity has declined over time as service industries have increased in importance. But raw materials continue to generate most of South Africa’s export earnings, and commodity price cycles therefore still matter greatly. We are currently in such a cycle, though it is far from clear whether it’s simply due to temporary Covid-related supply disruptions, or whether there is a longer-term demand due to greater global infrastructure shifting to green energy.

The chart below shows an index of the dollar prices of our seven main export commodities, coal (21%), iron ore (20%), gold (17%), platinum (15%), palladium (13%), manganese (11%) and rhodium (6%). The weights are based on Stats SA’s newly released 2019 mining industry census. The index is already well off its peak, and this explains much of the recent weakness on the JSE, but it is still some 50% above pre-pandemic levels. The fall in the iron ore price in the past few weeks has been severe as investors fret over China’s cooling economy, in particular its property sector.

Chart 2: US dollar price index of South Africa’s main commodities

Source: Refinitiv Datastream

The biggest problem with commodity price cycles is that many people forget that they are, in fact, cyclical. Incorrectly assuming that prices will remain high, companies typically borrow to expand production, while government raise spending levels expecting that taxes will keep pouring in. When the previous cycle turned sharply between 2011 and 2015, the government spending could not be pared back as tax revenues declined. As a result, debt levels shot up.

Original sins

Fortunately, most of this borrowing could be done in the local bond market and in the local currency. This is another key feature of our economy, and sets us apart from other emerging markets. South Africa has deep and liquid bond and equity markets and a sophisticated and strictly regulated financial system of banks, insurers and asset managers. Unlike many peers, it is not subject to the ‘original sin’ of emerging markets that have to borrow in foreign currency. Even in the context of massive capital outflows during the Covid panic of early last year, the government was still able to fund its deficit in domestic markets.

The history of South Africa’s capital markets starts with the gold mines, which required substantial funding. The Johannesburg Stock Exchange (JSE) was founded within a year of the discovery of gold in 1887.

The South African Reserve Bank was founded in 1921, and has played a key role in managing and regulating the financial system over the past century. In 1996, its prime objective of protecting the value of the currency (i.e. its purchasing power) was written into the Constitution, along with the operational independence to achieve this. Today it is highly regarded by international investors and credit ratings agencies, and seen as a key economic institution and source of stability. This became even more important over the past decade when other state institutions were weakened.

Smokestacks

Finally, another key feature of the local economy is its dependence on fossil fuels for electricity. Since being established in 1923, Eskom has generated electricity by burning coal, with only a small smattering of hydroelectricity (it is an arid country, after all). Koeberg, Africa’s only nuclear power station, was built in the early 1980s.

South Africa’s coal addiction makes it the 12th biggest carbon emitter in the world, despite having only the 23rd largest population and 33rd largest economy. Eskom alone is responsible for 40% of South African carbon emissions. While the share of renewable energy has grown rapidly over the past decade, it is still less than 10% of the total. Apart from the health and climate concerns of burning coal, there is an increasing risk that our trading partners in Europe and elsewhere will shun South African goods due to their high carbon footprint. ESG-conscious investors could increasingly avoid local bonds and equity. The world is moving on, whether or not we like it. The future is renewable.

Grounds for optimism

In 2002, London Business School academics Elroy Dimson, Paul Marsh and Mike Staunton published a book called Triumph of the Optimists, detailing global asset class returns since 1900. The title refers to the fact that equities outperformed bonds over the century, rewarding those who were optimistic about the future, which an equity investor by definition has to be.

Updated returns are published annually by Credit Suisse, and these show that between 1900 and 2020, South African equities generated higher real returns in local currency than any other country at an average of 7.2% per year. In dollar terms, South African equity returns were third (behind the US and Australia). This is remarkable considering the recessions, wars, unrest, political upheaval, distorting economic policies, corruption, commodity price cycles and international isolation South Africa endured over this period.

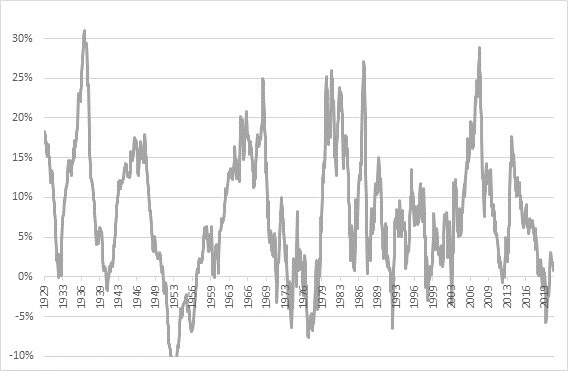

There are two further things to note. Firstly, to earn this 7.2% you have to be in the market for a long time because returns can be below that for years. Returns are cyclical in other words. The chart below shows rolling five-year real returns since monthly returns data starts in 1925. There are clear long-term cycles, and we’ve been through one such period of underperformance over the past few years.

Chart 3: 5-year rolling real SA equity returns, %

Source: Refinitiv Datastream

Secondly, the structure of the economy and the market has changed. While it was initially dominated by gold miners and then banks and industrial companies, today the biggest companies on the JSE are global players like Naspers (through its shareholding, now via Prosus, in Tencent), whose recent struggles have also weighed on the market. This is the case globally too. Dimson, Staunton and Marsh also show that railroad shares constituted 60% of the US equity market in 1900 and 50% in the UK. Few of these structural shifts are predictable, highlighting the importance of having broad diversified equity exposure in a portfolio.

Looking ahead

Will the next 100 years also deliver 7% average real returns? We simply don’t know, but it is safe to say that returns will be cyclical in future too. There will be lean years and fat years. Unlike in the past, South African investors are fortunate to have the option of global diversification today, even if it is capped at 30% in retirement funds. However, they should be careful not to throw the baby out with the bath water. There is a strong historic inverse relationship between starting valuation and subsequent longer-term returns. Buying expensive markets tend to result in below-average returns over the next five to 10 years, and vice versa. Today, the local market trades at a substantial discount, while global equities (particularly the US) trade at a premium. If history holds, local equities should deliver above-average returns, while global equity returns might disappoint.

By contrast, many argue that extreme inequality and high unemployment will lead to a major socio-political catastrophe, for which the July unrest and looting was only a forerunner, and that now is the time to get all your money out. This a risk, but not an inevitability. Political uncertainty and unemployment are likely to remain a feature, but this has been the case for decades and decades and the country still stands. Diversification is the best way to deal with such risks, and also helps to take the emotion out of managing money.