Parallel Paths to a Unified Market

The Termination of the SWIX Indices

The stock market can be read like a living story, shaped by shifting economic, political, and structural chapters over time. At its core are indices, which act as a compass for investors by bringing together hundreds of JSE-listed companies into a single, coherent measure of market performance. The recent termination of the SWIX indices marked the beginning of a new chapter in this story: one that reflects a market that has gradually settled into a more stable and mature form.

For many years, South African equity investors navigated the market using two closely related benchmarks: the FTSE/JSE All Share Index (ALSI) and its counterpart, the Shareholder Weighted Index (SWIX). While both tracked the same universe of companies, they were shaped by different perspectives and were designed to answer subtly different questions about what “the market” really represented.

The ALSI followed a traditional market-capitalisation-weighted approach, with companies weighted according to the value of their freely tradable shares. This methodology aligned with global index standards and offered a simple, offshore-friendly representation of market size. As South Africa’s market evolved post-sanctions, certain large firms — including Anglo American — shifted their primary listings offshore prior to 2011 and were subsequently treated as fully and globally free-float within the ALSI, under “grandfathered” arrangements. This treatment naturally increased the weight of these companies in the index, alongside other dual-listed stocks, introducing a growing global bias. That bias became particularly pronounced during the 2000s commodity cycle, when resource stocks came to dominate index weights and concentration risk increased materially.

Thus, the SWIX emerged as a response to the growing gap between headline market capitalisation and the practical experience of local investors. By weighting companies according to shares registered on the South African share register, it offered a lens on the market that was more closely aligned with the locally investable universe. This approach naturally reduced the influence of companies with substantial offshore ownership, resulting in a less concentrated index that many asset managers viewed as a more balanced reflection of domestic investment conditions.

These differences were not merely academic. Over time, they led to meaningful divergences in index composition, sector exposure, and performance outcomes. As a result, the industry adopted both benchmarks for different purposes. Many active managers, particularly within the general equity category, gravitated toward the Capped SWIX as a way to further manage concentration risk and pursue what they viewed as a more appropriate universe. At the same time, the ALSI remained the anchor for passive strategies, derivatives markets, and offshore investors, given its simplicity and global familiarity.

Source: Financial Markets Journal

However, as the market continued to evolve, the gap between these two perspectives began to narrow. Corporate actions, changes in listing structures, and the gradual unwinding of legacy treatments led to increasing overlap between the ALSI and SWIX. By the early 2020s, the majority of the differences that once justified maintaining parallel benchmark families had diminished, with only a small number of constituents still driving divergence.

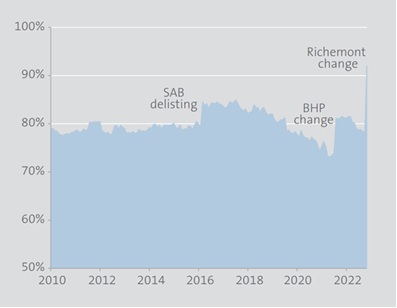

Overlap of ALSI and SWIX

Source: Camissa Asset Management, JSE

It was against this backdrop that the JSE’s index harmonisation initiative took shape. Rather than introducing a new methodology, the process acknowledged what had already occurred organically: the market had converged.

[BD1]

[BD1]

Source Allan Gray, PMX

Phase 1 of the project, implemented in March 2024, aligned weighting methodologies across the indices. Phase 2, effective from the end of 2025, completed this journey by formally retiring the SWIX indices and leaving a single, harmonised benchmark framework in place. This is not a break from the past, but a consolidation of it -pruning complexity while preserving continuity.

Implications for advisers and portfolios

The termination of the SWIX indices is viewed as a simplification rather than a shift in investment exposure or philosophy. The underlying equity market remains unchanged, and investors should not expect portfolio repositioning as a result. That said, the move brings clearer and more consistent benchmarking, reduces complexity in reporting and mandate governance, and improves comparability across funds and peers. While modest changes in individual stock or sector weights have occurred as legacy distinctions fall away, these are incremental in nature. For advisers, the transition enhances transparency without altering long-term risk or return expectations.