Outlook 2022: Japanese equities

The Japanese domestic economy is re-opening and stimulus is coming through, which could bode well for investors.

Japanese shares enter the new year against a much more positive backdrop than a few months ago. The eyes of the world were on Japan back in August when it battled a wave of the pandemic while also hosting the Olympic Games. Now, Covid-19 infections are very low, the domestic economy is opening up and companies are enjoying exceptionally strong profits growth.

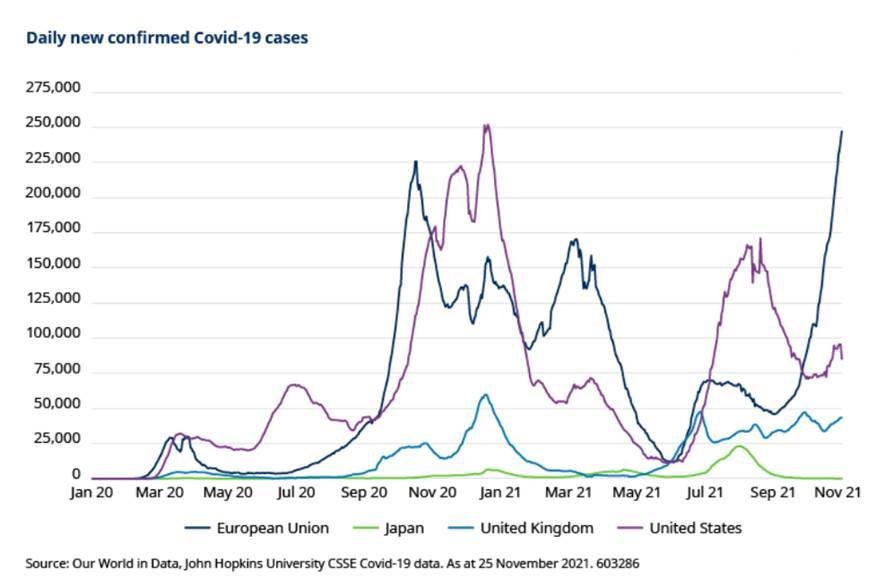

Japan’s rates of Covid-19 infections have always been below those of other major regions and the current level of new cases is very low, as the chart below indicates. After a slow start, almost 80% of Japan’s population was fully vaccinated by the end of November.

The new Omicron variant potentially poses a risk, and Japan temporarily reimposed a ban on foreign visitors in late November. However, prior success in containing the virus allowed the government to lift most domestic pandemic restrictions at the end of September 2021. While Japan has already benefited from the broader global economic recovery this year, we should now see the domestic economy re-open and recover.

Stable politics with stimulus to come

The re-opening of the domestic economy should receive a further boost from the government’s recently-unveiled stimulus package.

This is worth ¥43.7 trillion ($383 billion) and includes cash handouts for households with children, as well as for students and those on low incomes. The package also includes some subsidies and tax breaks for small businesses.

The stimulus package is the first major policy announcement from new prime minister Fumio Kishida. After the recent changes of leader, and the general election, Japan now faces a period of political calm. Elections for the Upper House are due next summer.

Small and midcaps to benefit

Timing-wise, Japan is behind other developed markets in terms of lifting restrictions and so the impact on corporate profits is also being felt with a lag. Earnings revisions are still trending higher while revisions have largely peaked in other regions.

This means the Oct-Dec 2021 quarter is likely to be very strong for company earnings, with the momentum set to continue into Jan-Mar 2022. Results for the quarter ending September saw around 40% of companies beat expectations, whereas a third is more typical. We expect corporate earnings to hit a new record high for the current fiscal year.

Looking within the market, we expect smaller companies in particular to benefit from the domestic re-opening. Many small caps are exposed to the domestic service sectors where we now anticipate a strong recovery. Japanese small caps have underperformed larger stocks for the last two years so we see this as an opportunity for them to play catch-up.

As a long-term fundamental investor, there is often a greater opportunity to add value given how under-researched some of the companies are, compared to the larger Japanese companies.

We also think the information technology sector is one that could do well in 2022, given the ongoing trends towards greater digitalisation.

Inflationary pressures subdued

One strain on corporate profits could come from rising input prices, particularly when it comes to energy costs. So far, many companies have not passed these on to customers, opting instead to absorb the higher costs themselves, but that won’t be sustainable for long.

However, inflationary pressures generally continue to be much more subdued in Japan than in other regions. The labour shortages being felt in some other markets and sectors are less of a concern in Japan. This is partly down to the success of former Prime Minister Abe’s policies to expand the workforce, especially by increasing the participation of women. It’s also partly due to Japan’s pioneering approach in terms of automating jobs.

We therefore don’t anticipate that inflation will be felt significantly on the consumer side. Japan’s consumer prices rose by just 0.1% year-on-year in October 20201, a far cry from both the Bank of Japan’s 2% target and levels in other markets (the equivalent US rate was 6.2%). As a result, we don’t expect to see any significant increase in wage demands.

Gradual improvements in governance

Meanwhile, the corporate governance picture in Japan has been improving slowly in recent years and we expect this to continue. Progress is never linear though and we should expect some bumps in the road.

The Toshiba saga indicates some of the challenges but also some of the advances made on corporate governance. The extraordinary general meeting this year, which saw shareholders defeat management and force proper consideration of the company’s future, was historic.

Managements’ greater consideration of shareholders should also be visible in the form of share buybacks. These were largely paused in 2020 as companies sought to maintain cash. However, with corporate Japan now recovering from the pandemic, buybacks have restarted and look set to remain an important feature of Japanese stock markets in 2022.