Outlook 2022: Global credit

Credit investors are facing a more nuanced phase as we head into 2022. Fundamentals are strong, but valuations are elevated, and uncertainties are building.

Corporate bonds are sitting on sizable gains for the period since the March 2020 Covid-19 shock. High yield corporate bonds are up by over 25%. Central bank and government support, followed by the discovery of vaccines in late-2020, and the reopening and sharp snapback in economic activity, have combined for a powerful recovery.

We are now, however, in a more mature and nuanced phase of the recovery cycle. Fundamentals are strong, economic activity and consumer demand remain healthy, but valuations are elevated and there is uncertainty around inflation, the process of monetary policy normalisation and Covid-19.

Julien Houdain, Head of Credit, Europe, said: “Macro conditions, input cost pressure and tight valuations with low dispersion, are tricky to navigate. We expect volatility in 2022, and moderate, income-led returns. The key will be identifying opportunities for relative outperformance, particularly sectors and companies which can protect margins against rising inflation. A maturing cycle introduces greater risk of excessive shareholder-friendly measures, potentially detrimental to credit.”

Economic conditions remain supportive, but more uncertain

The Federal Reserve (Fed) has begun the process of tapering its asset purchasing programme, which it aims to do at a fairly gradual pace. The problem is inflation indices are at decade highs.

Rick Rezek, Global Credit Portfolio Manager, said: “Some of the current inflationary pressure appears temporary. Headline levels should ultimately settle closer to central bank targets. That said, the longer inflation remains elevated, the more challenged the Fed will become, potentially giving rise to nervousness in markets. The biggest risk is that inflationary pressure pushes central banks to tighten more quickly than expected, though this is not our base case.

“Even with the Fed’s withdrawal of support, monetary conditions will stay accommodative and liquidity withdrawal is not a material risk to credit unless it causes growth to falter. US economic fundamentals are decidedly healthy, notably consumption and end-demand, with household savings at good levels. This is a helpful backdrop for credit. Against this, momentum is slowing, and valuations reflect almost no potential negative news.”

Other potential challenges include shifts in the US labour market, with businesses struggling to fill vacancies and over-55s opting not to return to the work force. Likewise, inflation, particularly fuel prices, could impact consumption.

The emergence of the Omicron variant underlines all too clearly the continued significant risk from Covid-19. There are new restrictions in parts of Europe, while the US vaccination rate remains relatively low, in the mid-50% range.

Discussing macro risks, Julien Houdain said: “As well as Covid-19, inflation, and monetary policy, we are monitoring China’s slowdown closely, although even with current challenges, it should still see decent growth in 2022. We are a bit more optimistic on emerging markets. A number of emerging economies have taken a lot of pain already, tightening policy materially in response to inflation, so the policy backdrop could become a bit kinder.”

Angus Hui, Head of Asia and Emerging Market Credit, said: “The systematic risks from the Chinese property sector should stay contained as Chinese banks have little exposure. We expect a bifurcation of the real estate market, and consolidation. Not all developers will survive, and further defaults are likely, but some distressed issuers could rebound sharply if they can secure financing domestically or sell assets. The market is expecting 30% of all China high yield property developers to default in the next 12 months, which looks pessimistic.

“Asian economies have continued to recover from the pandemic, particularly in the south east. The region remains well placed, given its relatively low vulnerability to rising commodity prices and US policy tightening, resilient domestic growth, proactive central banks, and low reliance on external debt.”

Corporate sector is strong, but facing challenges

The rebound in company earnings since March 2020 has fed into substantial balance sheet strengthening, giving strong support to credit markets. Scope for further improvement is likely to be limited from here, however.

The key challenge for companies this year will be defending margins against cost pressures, while there may be some inclination to pursue more shareholder-friendly measures, which can compromise balance sheet strength.

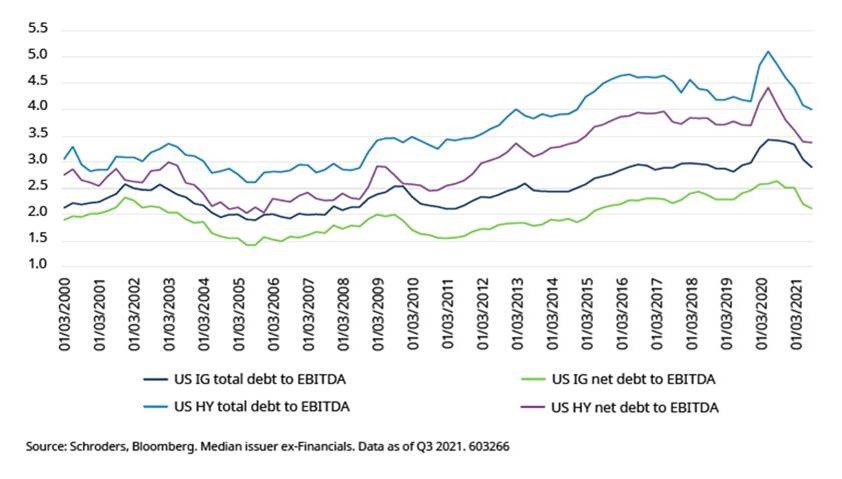

Image: Corporate balance sheets are solid and supportive

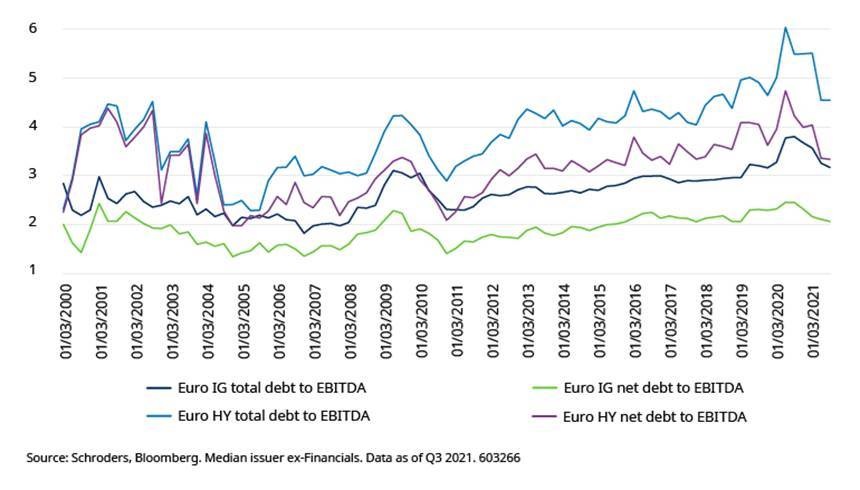

Image: European corporate fundamentals have strengthened since Covid-19

Julien Houdain said: “Earnings may see some further medium-term strength, against low year-ago comparisons, but the surge from reopening has largely played out. A key question is going to be how well companies withstand rising input costs, from labour and raw materials, and whether they can pass them on. Some automotive and materials companies are already managing to do so.”

Martha Metcalf, Head of US Credit Strategies, said: “Corporate fundamentals are healthy, and any deterioration will occur from very strong levels. Performance dispersion is likely to grow in response to companies’ varying ability to address rising input costs. This will present a bigger security selection opportunity than we have seen in the trending markets of recent years.

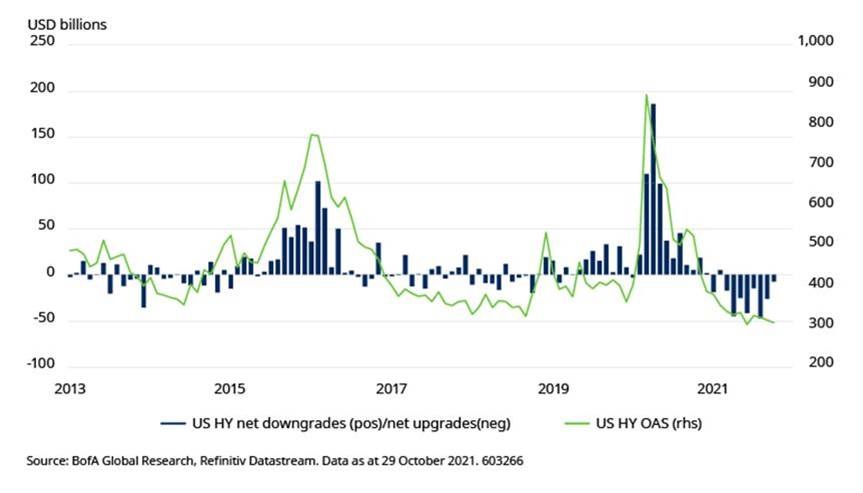

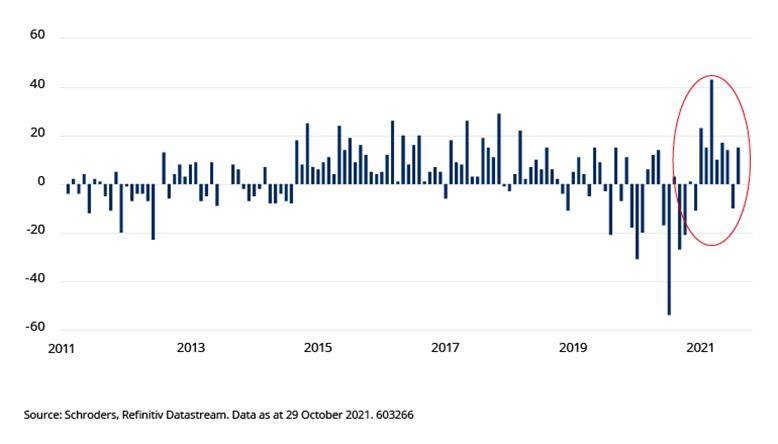

“The rating cycle has been increasingly positive, particularly for high yield. The increase in upgrades to downgrades has been supportive to the market as has the rising stars trend, as a growing number of fallen angel downgrades of 2020 complete the round trip back to investment grade. This process is quite advanced in the US, but Europe should start to catch up.”

Image: Ratings trends supporting high yield

Saida Eggerstedt, Head of Sustainable Credit, said: “The firmer commitments demonstrated at COP 26, from different corners of the world, underscore how environmental and climate disclosure and objectives are moving to the centre of companies’ financial planning. While markets have already moved in 2021 on social factors like the ‘Common Prosperity’ policy in China and the need for stronger supplier relationship, governance (the G of ESG) will remain an important driver of credit spreads. As our customers and regulators expect more ESG transparency, the growth of ESG bonds, coupled with engagement, can help differentiate companies on sustainability and social impact factors, as well help to find improvement candidates.”

Pockets of value in Asia, emerging markets and high yield

While investment grade corporate bond valuations are not cheap, they are well underpinned and should be stable, provided policy tapering and adjustments unfold as expected. US investment grade continues to offer reasonable income return, partly due to higher US Treasury yields, drawing interest from foreign investors. European yields are lower, but spreads offer more value.

Image: Foreign demand for US credit remains stellar

The most attractive pockets of value, however, are in Asia, emerging markets (EM) and parts of high yield. Euro and US BB spreads currently imply default rates of 3.7x and 1.9x five-year averages respectively.

Euro high yield offers value relative to the US, with the euro spread having fallen lower than the US, which is unusual. This may be partly because Europe is more exposed to China’s slowdown, cyclical forces, and supply chain issues, but these should start to dissipate. Drilling down, euro BB spreads are about 3.5x those of BBB, well above historical levels.

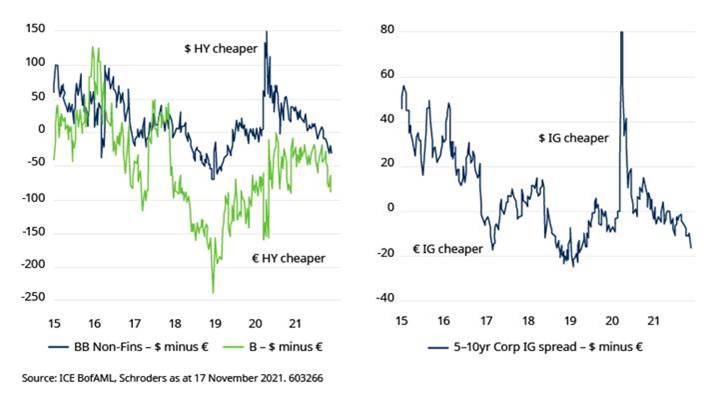

Image: European credit offers value versus US

Martha Metcalf said: “Ratings trends should stay supportive, with realised gains from rising stars re-deployed into high yield. This also reduces the overall duration or interest rate risk in high yield. But patience is needed, in readiness for when dispersion increases, and valuations are more compelling.”

EM high yield spreads are well wide of their developed market counterparts and there is greater dispersion, with a significantly higher proportion of EM trading at spreads of over 600 and even 800 basis points. This implies a greater range of opportunities at the security level.

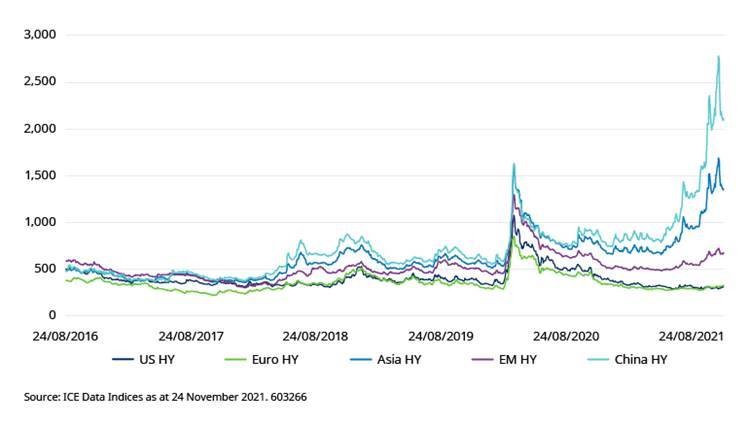

Image: Value in Asia and EM high yield

Angus Hui said: “Asian investment grade credit valuations are supported by stable and improving fundamentals, while high yield offers abundant idiosyncratic security selection opportunities. We see opportunities in renewable energy in India, whereas in Indonesia, new issue valuations are less compelling. Some sectors in China face risks from moves to reduce borrowing and we are particularly selective toward high yield industrials.

“Asian credit spreads should stabilise in the first half of 2022, but they may not converge to historical averages, at least near-term, as investors remain wary of policy risks from China.”

Julien Houdain said: “We see broadly improving EM corporate fundamentals, and potentially stabilisation at the macroeconomic level, but the picture is fairly idiosyncratic.”

Saida Eggerstedt noted potential opportunities in China from a sustainability investment perspective: “China has to catch up on decarbonisation, having spent years as a growth powerhouse. This will require large scale investment across the value chain. Green and ESG bond issuance picked up in 2021, but mainly from the property sector. In 2022 we will also look at ESG bonds from other sectors like renewables, that enable China to substitute coal for sustainable energy sources, or electric vehicle parts companies. On the social side, bonds that facilitate access to basic services will be welcome by impact investors like us.”