Not over by Christmas

Remembrance Day is celebrated in November in many countries, commemorating the end of the First World War in November 1918. When the war broke out in July 1914, it was widely assumed that it “would be over by Christmas”.

Clearly that wasn’t the case, nor did it turn out to be the “war that ends all wars”. And to make matters worse, when it did finally end, the world was engulfed by the deadly Spanish Flu pandemic.

Today’s Covid-19 pandemic similarly drags on. Many of us assumed it would only last a few weeks or months when the first lockdowns were announced in March 2020. The good news is that vaccination and treatment options continue to expand, bringing the end date ever closer. But the virus continues to rage in many countries, most recently in central Europe, and the global economy is still massively distorted by this microscopic pathogen.

Millions are still out of work and many businesses closed for good. Companies that still operate face scarcities of several key items, ports are clogged, supply chains stretched, and food and energy prices have shot up. Demand for goods remains elevated and demand for face-to-face services is still below pre-Covid levels.

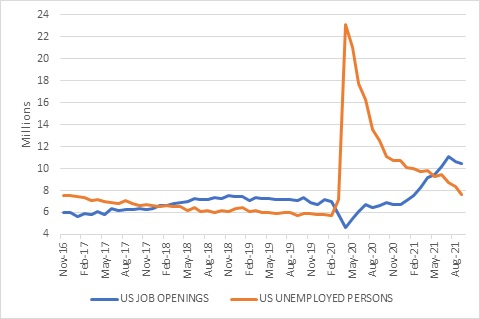

One of the stranger distortions is that there is simultaneously a lack of jobs and a lack of workers in many places. To use the US example, there are 10 million job openings, and 8 million unemployed people. Companies looking for workers can’t seem to match up with workers looking for jobs. There are a number of reasons for this, one being that for many people, especially in rich countries, the pandemic has been a period for introspection and many have reassessed when, where and how they want to work.

Chart 1: Job openings and unemployment in the US

Source: Refinitiv Datastream

It is in this difficult, fluid and uncertain environment that policymakers need to navigate, and since polices impact economies and markets, investors too are trying to anticipate where things are headed.

The US Federal Reserve is the world’s most important central bank and its decisions reverberate through all financial markets. When the pandemic hit, the Fed cut interest rates to zero and unleashed quantitative easing on an unimagined scale, eventually buying $120 billion a month in Treasury and mortgage bonds. With the economy firmly in recovery mode, this emergency support is no longer needed. The first step back to normality was taken at the recent monetary policy meeting where it was announced that bond buying would be pared back by increments of $15 billion per month. At this pace, the Fed will have completely stopped its purchases by mid-2022.

Importantly, the announcement went off without a hitch. The Fed had signalled its intentions over several months, and the market was not surprised. Moreover, it made it clear that it was in no hurry to hike interest rates.

Its big challenge is the surge in inflation, which hit a 30-year high of 6.2% in October. The Fed initially characterised the inflationary jump as “transitory”, a term it might be regretting somewhat now.

What is transitory?

Whether or not inflation is transitory depends on how that is defined. Transitory doesn’t mean that the prices that jumped will fall again. Prices for many items might be permanently higher, but the rate of change in those price rises can slow. To use an obvious example, the price of oil doubled in the past year. It is extremely unlikely to double again, so even if the price stays high, the rate of change of the price will come down rapidly. Transitory also doesn’t mean two or three months. It could take as much as 12 months for the current elevated prices to act as a high base to slow year-on-year comparisons.

The way central bankers think about transitory is broadly “as long as the pandemic continues to distort the economy”. Once life returns to normal, so too will spending (fewer goods and more services) and bottlenecks in the supply chain should disappear.

Overheating?

On the other hand, those who argue that inflation is not transitory, point out that the excessive demand for goods is not just because people in rich countries could not consume services, but because there was a massive fiscal injection, particularly in the US, that put money in people’s pockets. On top of that, record low interest rates make buying a house or a car cheaper.

In this view, developed economies (again, particularly the US), are overstimulated. Central banks need to cool demand by raising interest rates.

Which view of the world turns out to be right we will only know in time, but policymakers also need to judge the risks of acting too soon versus acting too late. The risks aren’t always symmetrical. Act too soon and a promising recovery is jeopardised and unemployment is higher than it need be. Act too late and higher inflation needs to be brought under control with higher interest rates. Patience may therefore be warranted even amid extreme uncertainty.

Patience is a luxury

Patience is not a luxury many emerging markets have. They cannot afford to let inflation rise, even temporarily. They have histories of damaging inflation spikes, even hyperinflation, and inflation expectations can quickly become unmoored. They are less productive, and therefore demand can often outpace supply, leading to inflation. Their currencies are also more volatile which can compound increases in global food and fuel prices. Therefore, a spate of developing countries has been hiking interest rates, aggressively in some cases like Brazil and Russia.

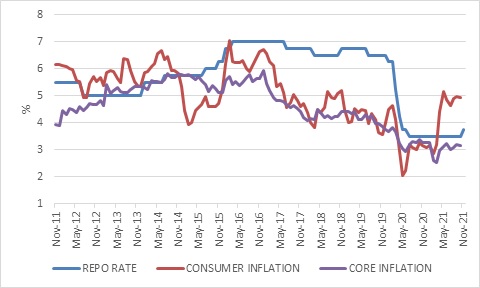

South Africa has a better inflation trajectory than many peers and can afford some patience. Consumer inflation was unchanged at 5% in October, with elevated food and fuel inflation contributing half of the total. Food inflation was 6.7% in October and petrol inflation 23.1%. These prices are set in global markets and then converted in rands at the prevailing exchange rate. While the rand has been volatile, it has basically moved sideways over the past year, neither adding nor detracting much to inflation. Therefore, half of domestic inflation is unconnected to domestic demand. Another big contributor is electricity tariffs that were 14% higher than a year ago. This is also unconnected to consumer demand, since it is set by the regulator based on what Eskom needs, not where a free market for electricity would price it.

Core inflation – excluding food, fuel and energy prices – was unchanged at 3.2%. This is arguably a better indicator of the lack of demand-pull inflation.

Chart 2: South African repo rate and inflation

Source: SA Reserve Bank and StatsSA

The cycle has turned

Nonetheless, the SA Reserve Bank’s Monetary Policy Committee (MPC) raised the repo rate by 25 basis points to 3.75%, in a decision that was split three against two. The September decision keeping rates unchanged was unanimous.

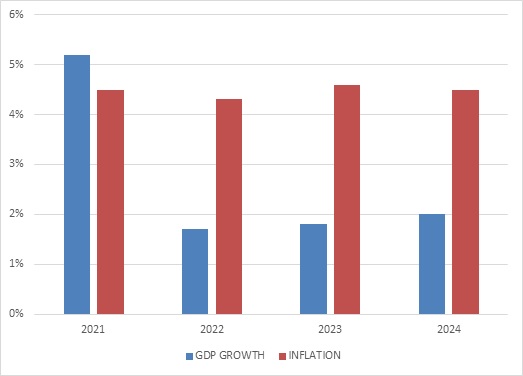

The Reserve Bank’s forecasts haven’t changed much and do not by themselves call for higher rates. The growth outlook was revised down a bit and the inflation outlook a touch higher.

Chart 3: Reserve Bank growth and inflation forecasts

Source: SA Reserve Bank

Reading between the lines, the MPC’s big concern is what happens globally, rather than the local outlook. It is nervous that interest rates in the US and other major markets will rise sooner rather than later and is keenly aware that emerging market peers are acting forcefully. Lagging behind risks placing downward pressure on the rand, and through higher import prices, upward pressure on inflation. Currency depreciation has a much smaller impact on inflation these days than in the past, but the risk probably remains.

The MPC’s hope is that by starting the hiking cycle earlier, it can hopefully end it earlier too, rather than waiting too long and then having to raise rates dramatically. The SARB’s quarterly projection model implies a 25 basis points rate hike at every MPC meeting next year, but the model probably overstates the extent of tightening that will be necessary.

Somewhat tighter fiscal policy, as announced in the MTBPS, takes pressure off monetary policy in two ways. Firstly, and most directly, it acts as a drag on demand and therefore limits what little demand-pull inflation there is. Secondly, it improves overall policy credibility in South Africa. During the ‘state capture’ years, the SARB often stood alone as a pillar of institutional strength. Arguably, it had to maintain higher interest rates than otherwise warranted. However, as with market participants, the Reserve Bank knows that talk is cheap and that the Treasury has to deliver on its promises to regain credibility.

The South African interest rate cycle has turned. Based on what we know now, it is likely to be a gradual upward trend. The economy still needs low rates, and there is a risk that the Reserve Bank is pulling the rug out from underneath too early. For investors, it means slightly higher returns from the money market, but for now you will have to squint to see it. The real returns (in both senses of the word) are still to be had at the longer end of the fixed income market. Ten-year bonds trade at double the Reserve Banks’ forecast inflation, a substantial margin of safety even if inflation turns out to be worse than expected.

Predictions are hard, especially about the future

World War 1 changed the world in ways that would have been impossible to predict at the time. Three European empires collapsed (Germany, Russia and Austria-Hungary) and a fourth, the British, was dealt a severe and permanent blow. The years after the war saw the birth of several new nation states. The US emerged as a new economic, military and financial superpower. Women were finally given the vote in several major countries. Union membership soared. An era of prosperity and technological advancement ensued (the roaring twenties), but its excesses would contribute to the economic collapse of the Great Depression. Policy mistakes probably played an even bigger role. One of these was that countries rushed to return to the gold standard after the War, without realising fully how the world had changed. For instance, in his first act as Chancellor (finance minister) in 1925, Winston Churchill returned the UK to the gold standard at the same exchange rate as before the war, as if nothing had changed in the dramatic inter-leading years. As a result, sterling was now fixed at a level that was way too strong for not only the British economy, but for the entire global system. When the Depression did finally arrive in 1929, the gold standard made things much worse. It was the biggest policy error in modern economic history.

With hindsight everything is easy of course. Churchill was convinced he was doing the right thing in the name of stability and prosperity and acted on the advice of the top experts of the day (though the great economist John Maynard Keynes was a vocal critic). In fact, at the time Churchill’s announcement was considered one of his finest speeches yet. But it turned out to be a disaster.

Similarly, a few years from now it will be obvious to us what should have been done today. We’ll either say “of course inflation would run away and the Fed was behind the curve” or “of course inflation would recede and the Fed’s patience was warranted”. Today, both those outcomes are still possible, as are others still unknown to us. Like World War 1 and the Spanish Flu, the Covid pandemic has probably changed economic norms and behaviour in ways we don’t fully comprehend yet.

While investors should form an idea of what the future might hold, they need to be prepared for all eventualities and not base their investment strategy on one single outcome.