Not enough yield and nowhere to go? Multi-asset income funds offer a compelling solution

We believe multi-asset income funds, like the PSG Diversified Income Fund, offer an all-round solution

Investors seeking sufficient income yields are having to digest the impact of the low interest rate environment and the need to take more risk to achieve a sufficient yield. We believe multi-asset income funds, like the PSG Diversified Income Fund, offer an all-round solution. These funds still have capital preservation at their core, but can also access a wide investment toolkit, offering fund managers more latitude and holding several advantages for investors:

• Flexibility: access to multiple asset classes and instrument types (fixed, floating, inflation-linked, credit) and the ability to dynamically allocate capital to the best areas at advantageous points in the cycle.

• Tools to hedge and mitigate risks in the fixed income market (e.g. use of offshore cash).

• Ability to opportunistically sweeten returns with small but valuable allocations to growth assets such as appropriate equities, listed property, commodities or preference shares.

Interest rate cycles and market yields

The low repo rate has significantly lowered return expectations, impacting many fixed income instruments which benefit from a higher repo rate. This does not look likely to change very quickly in the near term. Despite near-term inflation printing at 5.7%, the outlook over the longer term appears in line with a new normal long-term target for the South African Reserve Bank (SARB) of 4.5%. Given the SARB generally applies a measured approach, the data does not imply an aggressive rate hiking cycle is very likely.

However, government bonds offer the best value for income investors, as these bonds have not followed the typical bond market rules: historically, cuts to the repo rate and falling inflation resulted in falling bond yields. While we acknowledge the deterioration in the South African fiscal situation, additional revenue from commodity companies, combined with fiscal restraint by the Finance Ministry, means the outlook is less bearish than what was outlined in the October 2020 Medium-Term Budget Policy Statement (MTBPS) or the February 2021 Budget. Government bonds are cheap and no longer a non-consensual trade in the market. Clients have reaped the rewards for taking a long-term view on government bonds. We are seeing clients struggle with how much risk to take to earn a decent yield, leaning to bond funds to take advantage of the value in bonds. However, we see multi-asset income funds as better positioned to balance risk considerations while also seeking a steady income.

Flexibility – comparing risk management in these options

Multi-asset income funds are able to actively use interest rate risk when appropriate – when government bonds are cheap. Typically, the use of duration is far less than in bond-only funds. Multi-asset income funds are also able to actively allocate to a wider array of corporate bonds at opportune times in a cycle, diversifying your credit risk exposure. In addition, these funds can use a selection of local and global equity and property stocks, as well as preference shares, when the fund managers see value. In contrast, bond funds face some potential constraints:

• Duration exposure is required within a range of the index, currently around 6.3 years.

• The All Bond Index is made up of exposures to an array of state-owned enterprises (SOEs, including Transnet, Eskom and SANRAL).

• The index does not contain inflation-linked bond exposure.

• Typically, bond funds may not have the ability to access offshore ideas.

In short, while bond funds provide direct exposure to attractive bond markets, they have potentially much higher duration risk, with fewer opportunities to diversify and manage it.

Solving for the yield conundrum in a risk-adjusted manner

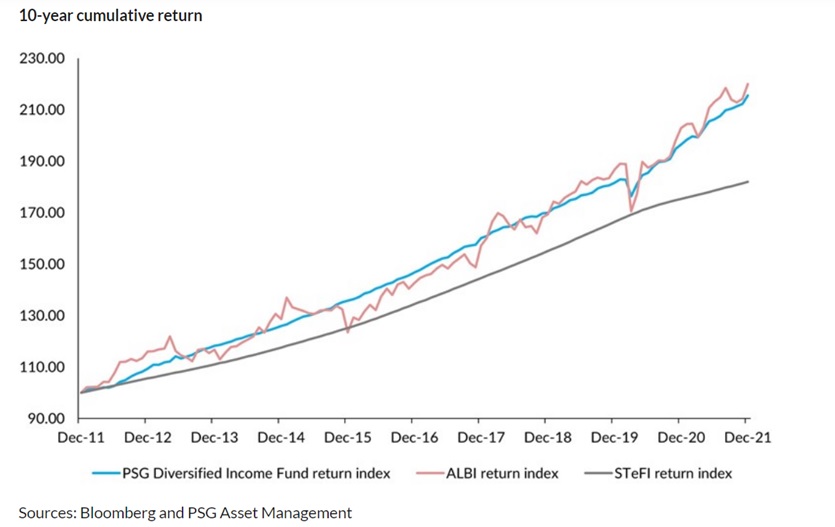

We see capital preservation as core to an income fund with investors needing to outperform cash and maximise income yields. In the graph below, we show a simple comparison of the PSG Diversified Income Fund to the All Bond Index and STeFI (cash benchmark) over a 10-year period.

On a cumulative and an annualised basis, the PSG Diversified Income Fund has performed in line with the ALBI over 10 years, and importantly, outperformed the STeFI benchmark (beating cash over long periods of time) illustrating its ability to meet both objectives.

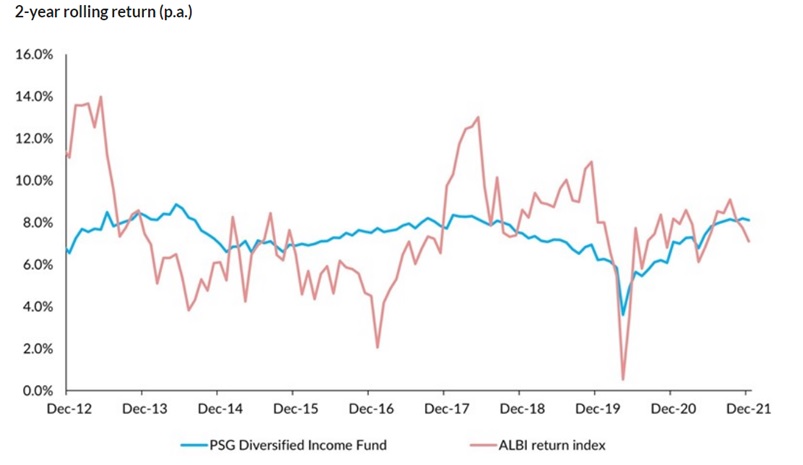

Further, as the graph below highlights, this performance has been achieved at much lower levels of volatility than those of the bond index over appropriate periods of time.

In short, multi-asset funds, with their more extensive investment toolkit, can yield a better all-round result over appropriate time frames with significantly less risk and volatility.

We foresee higher than average returns from multi-asset funds going forward

We believe that higher than traditional exposure to bonds will be required to generate inflation-beating returns. Multi-asset income funds provide attractive risk-adjusted return prospects, especially at this point in the interest rate cycle. These funds allow us sufficient scope to allocate capital to the current attractive yields in the bond market, while offering broader access to sources of risk and return for income-seeking investors.