New Year, Same Problems?

While 2025 is in full swing for most of us, 1.4 billion Chinese are only starting their new year this week. The country celebrates New Year on Wednesday according to its ancient lunar calendar.

It will be followed by a week (or more) of celebrations, and tens of millions of people are traveling to their hometowns or other holiday destinations. Known as ‘Chunyun’ in Chinese, it is the largest annual human migration on earth. The fact that it mostly runs smoothly each year is thanks to the country’s remarkable transport network, including the fact that China has more high-speed rail mileage than the rest of the world combined.

This is clearly impressive, but also hints at a rising problem in China: overinvestment. Not all these trains necessarily generate an economic return if ridership is too low or if the construction costs were too high. And yet more are being built. The same is true of investment in general. When a country’s infrastructure is underdeveloped, upgrades generate short-term and long-term benefits. However, beyond a certain point, diminishing returns set it. For instance, connecting two towns with a tarred road for the first time will generate positive economic spillovers, which will probably pay for the road many times over. Connecting these two towns with a six-lane highway will also deliver a boost, but not necessarily enough to justify the construction costs. Adding a second road that shaves a few minutes off the driving time is throwing away money. While the rest of the world marvels at China’s investment spending, it is simply too high now given its level of development.

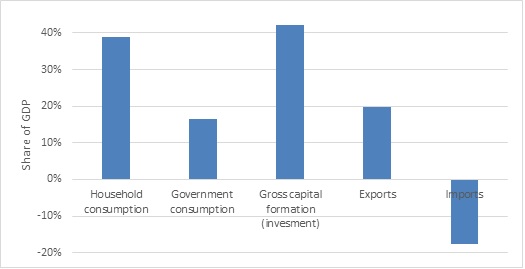

Chart 1: The strucuture of China’s economy by expenditure

Source: National Bureau of Statistics

Yet it continues to invest 40% of national income (GDP) annually, a higher proportion than any other country in modern history. This investment increasingly struggles to earn a return to justify the associated borrowing, and overcapacity abounds. This has been particularly acute in the property sector, where there are millions of empty homes and a swathe of bankrupted property developers.

The flipside is that household consumption is very low by global standards, around 40% of national income whereas it is around 60% to 70% in other countries. This is partly because Chinese households save a lot, but also because they receive a smaller share of income generated in the economy than in other countries. Instead, the public sector (government and state-owned enterprises) receives an outsized share. Redistribution of this income is unexpectedly low for a communist country, and social safety systems in China are relatively weak, partly due to the ‘hukou’ household registration system that ties people to their home provinces and denies many migrant workers social assistance in the cities where they work.

When thinking about the outlook for China’s economy, it is important not to lose sight of these facts. Despite the remarkable achievements in rapidly modernising the economy over the past 30 years – and in some ways overtaking more advanced Western countries – this is an unbalanced economy. It means that untangling cyclical from structural forces can be tricky.

On target

This brings us to the latest economic growth numbers and the outlook for 2025. The Chinese National Bureau of Statistics recently announced that the economy grew 5% in real terms in 2024, in line with the government’s target. The data showed some upward momentum in the fourth quarter, which is believable given a lower third quarter base, strong exports (perhaps due to some front-loading of purchases ahead of possible US tariffs) and the impact of several stimulus measures announced in the last few months of 2024.

However, the 5% number warrants some scepticism. As the economist Charles Goodhart famously noted years ago, “when a measure becomes a target, it ceases to be a useful measure.” The mere fact that Beijing implemented interest rate cuts and other stimulus measures towards the end of last year suggests that it saw signs of real trouble. If the economy was humming along, these steps would not be needed. For instance, the Rhodium Group, a consultancy, estimates that growth was probably closer to 2.8% in 2024.

The point is not to quibble about the exact number – GDP is always an estimate anyway, not an objective truth – but to think about the direction of travel. The economy has deteriorated in the past two or so years.

What makes it particularly painful is that after decades of consistently strong growth, many business models were built on the assumption that it would continue. Money was borrowed and investments made. People need to get used to lower growth. Think about it this way: no South African would be disappointed with real growth of 2.8%, but that is because our expectations are much lower.

The next question is whether things will improve from current levels, whatever they may actually be, especially given the potential headwinds from US tariffs. President Trump’s inauguration was followed by a flurry of executive orders, but we still have no concrete details on changes to trade policy.

Trump’s unpredictability will keep Chinese leadership guessing, but they probably also see Trump as someone who is transactional more than ideological. In fact, so far, he has been notably softer on China than expected, with neighbouring Mexico and Canada taking the full brunt of menacing tariff threats. Far from the 60% tariffs on Chinese imports promised on the campaign trail, he had conversations with President Xi and sounds open to deals.

Export boom

Chinese exports to the US are already lower than during the pre-pandemic era, and certainly much lower than where the pre-pandemic trend would’ve suggested it would be today. Mexico has overtaken China as the biggest importer into the US, though a fair slice of Mexican trade to the north probably originates from China and is simply rerouted. Nonetheless, it is very likely that China’s export machine will run into higher US import tariffs. It is just a question of time and extent.

The US is also unlikely to be the last country to object to ever-rising Chinese exports. Increased protectionist tendencies worldwide mean China will not be able to export its way out of trouble indefinitely. Even as exports to the US have been softer, overall export volumes have surged. As chart 2 shows, before Covid, China’s export volumes increased in line with global trade. Post-pandemic, it has risen much faster. This is partly because China emerged, almost out of nowhere, as the world’s leading exporter of vehicles.

Click here to read more...