Municipal bonds: Not just for US investors any more

Jim Conn, Senior Vice President, Portfolio Manager at Franklin Templeton Fixed Income Group.

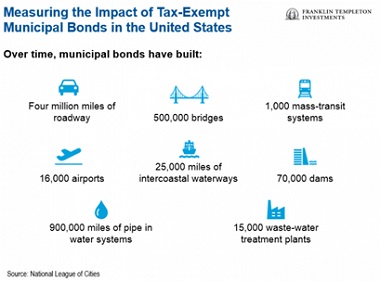

Municipal bonds have been the chief engine for infrastructure growth in the United States for more than 100 years. Today, roughly three-quarters of US infrastructure has been funded with the help of municipal bonds, making them the cornerstone of the country’s infrastructure strategy. Muni bonds fund the building blocks of a competitive, modern economy.

US municipal bonds represent state- or local-government issued debt which is generally used to finance public services or infrastructure projects including roads, schools, water and sewage systems, airports or energy transmission facilities. Bonds that a municipality issues to finance a public good are generally exempt from US federal and local income taxes, which increases the effective yield available to the US-based investor.

US taxpayers therefore have found favor in municipal bonds due to their tax-exempt status. Individual investors own the majority of US municipal bonds, either directly or through mutual fund products.

What are munis?

• A municipal bond is a debt security issued by a US state, municipality, or county to finance its capital expenditures.

• They are used to finance public projects and obligations.

• Most munis are exempt from US federal taxes and from most state and local taxes.

Certain US municipal bonds are not exempt from federal taxation. Although this market is smaller than the tax-exempt market, we believe it presents a fairly large opportunity set for investors. In 1986, the US federal government passed legislation limiting the types of bonds that were exempt from federal taxation to those funding what could be exclusively be considered a “public good.”

A bond funding a project that substantially benefits a private entity, such as a sports arena, could no longer offer tax-exempt income to investors. This newer class of taxable bonds is known as private activity bonds (PABs). While not an authorization to do so, the legislative changes in 1986 acted as a catalyst for municipalities to issue more taxable bonds.

In addition, in February 2009, as part of the American Recovery and Reinvestment Act, US President Barack Obama signed a law creating a new class of taxable municipal bonds known as Build America Bonds (BABs). Although these bonds are not tax-exempt, BABs included a federal subsidy in hopes of further boosting infrastructure spending.

This subsidy has helped to offset the effect of taxation to the investor, making them especially attractive to foreign investors. State and local governments issued nearly US$200 billion worth of BABs before the end of 2010, when the program ended.1 These bonds proved popular with foreign investors and by the end of 2015, US$85 billion worth of BABs were owned by investors outside the United States.2

Additionally, issuers have always been able to issue in the taxable municipal bond market to help expand their audience beyond the US taxpayer. We have seen a marginal increase in issuance over the past year.

More infrastructure spending could bring more muni supply

Since the 1970s, US federal and local government spending on public infrastructure has declined. As a result, critical infrastructure across the United States such as roads and bridges has deteriorated. Recently, partisan gridlock has hindered meaningful investment at the federal level, so most new municipal bond issuance has been left to state and local government.

However, one area of possible bipartisan consensus under the new US Trump administration may be a renewed emphasis on infrastructure spending. This could result in new public-private partnerships and the issuance of qualified public infrastructure bonds.

As a whole, investors continue to find the relative safety of US municipal bonds and tax-exempt income attractive. At the end of 2016, US municipal bond issuance hit a six-year high of more than US$420 billion, bringing the total size of the US municipal bond market to US$3.7 trillion.3 Of this total, investors outside the United States owned US$93.3 billion, as at 30 September 2016.4 Although this represents a relatively small slice of the total US municipal bond universe, that number is growing.

Taxable vs. Tax exempt

Nominal yields on taxable municipal bonds have generally been higher than similarly rated tax-exempt municipal bonds along the maturity spectrum, but there is no difference in credit risk between similarly rated taxable and tax-exempt bonds. In most cases, the issuers are the exact same.

General obligation (GO) municipal bonds are secured by the full faith and credit of a state or local government and are paid through the General Fund. In contrast, revenue bonds are secured by a dedicated revenue stream usually from a tangible asset such as an airport or toll road. In either case, historical defaults have been extremely rare, with the last state GO bond default occurring in 1933.

More generally, in the period 1970–2014, the one-year default rate for investment-grade municipal bonds was less than one tenth of one percent, with the majority of the defaults coming from issuers in the housing sector.

While investment-grade municipal bonds make up the majority of the total market, some investors buy lower-rated or even below-investment-grade (or high-yield) municipal bonds in their quest for greater yield. Investors in higher-yielding municipal bonds take on increased credit risk based on the financial strength of the underlying issuer in exchange for higher yields. This more aggressive risk-return profile tends to be more attractive to investors with longer time horizons and are therefore able to tolerate more short-term volatility.

Municipal bonds vs. Corporate bonds

While a government entity issues municipal bonds to finance primarily public projects, corporate bonds, as the name implies, are issued by a corporation to fund any variety of business operations or expansion projects as management deems necessary. Since corporate bond issuers fund their debt payments through business operations rather than through tax revenue—as is the case with GO municipal bonds—corporate bonds are subject to greater credit risk.

Any number of adverse conditions may affect the issuer’s ability to service the bond. As a result, average yields on corporate bonds tend to be modestly higher than municipal bonds with similar credit ratings and maturities.

Although the current difference in average yield between corporate and municipal bonds is somewhat modest, US municipal bonds are significantly less likely to default than corporate bonds with similar ratings and are therefore considered to be a significantly less risky investment from a credit perspective.

Additionally, the focus on more essential service-type financing helps provide a stronger credit profile for municipal issuers. In the unlikely event that a municipal bond does default on an interest payment, the recovery rate—the amount the bondholder ultimately receives relative to the outstanding debt—is usually very high.

In the case of GO bonds, the historical recovery rate is almost 100%, with many municipalities legally obligated to repay bond holders before fulfilling other debt obligations. In comparison, the recovery rates of even highly-rated corporate debt can vary widely in the event of default. During the period of 1987–2007, the average recovery rate across the corporate credit universe was slightly over 50%.4

Over the past 100 years, defaults have proven to be very rare in the municipal market. Looking at more regionalized corporate bonds, we can see a similar relationship between US municipal bonds and European corporate bonds.

The yields on taxable municipal bonds remain relatively attractive as compared to similarly rated asset classes such as euro-denominated investment-grade corporate bonds.

In addition to lower volatility than corporate bonds and generally higher yields than US Treasury securities, municipal bonds offer a low, and sometimes negative, correlation to stocks.6

Municipal bonds also offer a lower correlation to other fixed income assets, adding an additional layer of potential diversification to a portfolio. One additional benefit we have found for non-US based institutional investors has been the longer duration7 of the municipal bond market versus corporate bonds. This is due to the fact most municipalities are financing projects with long lives and hence want to have the financing match the term of the project.

No two muni bonds are the same

Although municipal bonds share many similar characteristics and can add stability to a well-diversified portfolio, it important to remember they may have different sources of security, even from the same issuing municipality. In fact, as at 30 June 2016, the US municipal bond universe was composed of over 117,000 state and local entities, with over 950,000 total municipal bond issues.8

Our municipal bond team focuses on maximizing income for each and every one of our portfolios. This focus is driven by the fact that, historically, income has been the primary driver of total returns in the municipal bond asset class.

In conclusion, we feel an allocation to municipal bonds can provide another source of attractive, high-quality income to a portfolio while also diversifying from a credit standpoint. We believe partnering with an expert is critical, given the nuanced nature of the municipal bond market.