Moving targets

The curveballs keep coming. The ongoing uncertainty surrounding US President Donald Trump’s tariff policies was ratcheted up again, after a federal court ruled that he exceeded his authority in imposing “reciprocal” tariffs on many countries.

Setting tariffs has always been the preserve of Congress, but legislation contains loopholes for the President to act in emergencies. The court believes the Trump administration overstepped the mark, however, the tariffs will remain in place while they appeal the judgement. The end goal of US trade policy remains a moving target.

Other loopholes remain open. While courts are unlikely to block all the tariffs, the judiciary is one of the factors that restrains Trump. Another constraint is political. Tariffs will be very unpopular once the impact starts hitting consumers, and this will make Republican politicians nervous ahead of the November 2026 mid-term vote. They will want him to steer his attention to the other elements of his agenda that are more friendly to both voters and the big donors that support their election campaigns.

The other constraint is the markets. The signals from investors have been clear: asset prices fall when tariffs are threatened and rise when concessions are made. However, it is possible that a degree of complacency will set in. Based on the pattern of the past few weeks, markets now clearly expect that Trump will always compromise. The unflattering acronym TACO (Trump Always Chickens Out) has been floating around in the financial media in the past few weeks. Perhaps that is why he made tough noises against China again on Friday. There is a “boy who cried wolf” quality to all this, and we should remember that Aesop’s fable did not have a happy ending.

Nonetheless, all of this suggest that the risk of extreme outcomes has diminished. We are not going to return to the status quo before Trump took office, but we’re unlikely to settle at tariff levels as high as was announced in that first week of April.

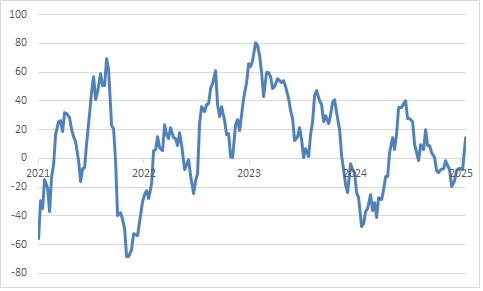

Meanwhile, US economic data has held up better than expected in the last few weeks, though it still does not capture the full extent of higher tariffs, given the amount of stockpiling by companies and households earlier in the year. The 90-day tariff reprieve has opened up another window for stockpiling, but much of this will be bringing forward demand. It still suggests that growth will slow into the second half.

Chart 1: US economic surprise index

Source: Citigroup

This creates a difficult backdrop for the US central bank, the Federal Reserve. Tariffs point to higher goods prices as well as downward pressure on economic growth, though loose fiscal policy relieves some of the economic pressures. Inflation also remains above the Fed’s target. Its preferred inflation measure, the personal consumption expenditure deflator, was 2.1% in April.

The Fed is also not just grappling with cyclical factors, but structural questions too. Minutes from the recent FOMC meeting show officials discussed the risk that a reduction in the safe haven status of US Treasuries and the dollar could have long-term economic implications. One example (of many) is a clause tucked away in the new budget bill that would allow the government to tax holdings of US assets by investors from countries deemed unfriendly to the US. It has yet to become law but could act as a disincentive for foreigners to invest in the US.

The more it is pulled in different directions, the less likely the Fed is to do anything. For now, at least. For central banks outside the US, it is a more straightforward story. US trade policy has little direct impact on inflation, but poses downward risks to the growth outlook. This is a demand shock that central banks know how to respond to. Fourteen cut rates in the month of May.

Repo rate reduction

One is the South African Reserve Bank. Its Monetary Policy Committee reduced the repo rate by 25 basis points to 7.25% in a five to one vote. The dissenting voice argued for a bigger cut, suggesting the door to a further reduction remains open. This is especially given that the Bank’s estimate of the neutral interest rate, the theoretical level of interest rates that keep the economy on an even keel, is around 7% based on the latest inflation forecast.

Click here to read more...