Moving at warp speed

Capturing structural growth potential is not easy, but in uncertain markets, it’s essential. Today, investors are eager to understand more about the potential opportunities in Artificial Intelligence (AI).

Ninety One Head of Quality, Clyde Rossouw, explains why exposure to higher quality companies can successfully position investors for an AI-driven future.

AI – or machine learning – is not new. Humans have been automating work for nearly 300 years, with the industrial revolution supporting the transition from creating goods by hand to using machines. What has changed in recent years, however, is the explosion in the amount of data and computing power available, allowing researchers to build far more powerful models than previously thought possible.

AI will soon be able to do many things we thought only humans could do and do many things that humans simply cannot do. However, the difference between ‘tourist’ users and those that have been trained to use AI is profound. Proficiency at prompting is key; much like accessing a database, speaking the appropriate query language is vital to ensure accurate results.

AI is no longer just a tech story

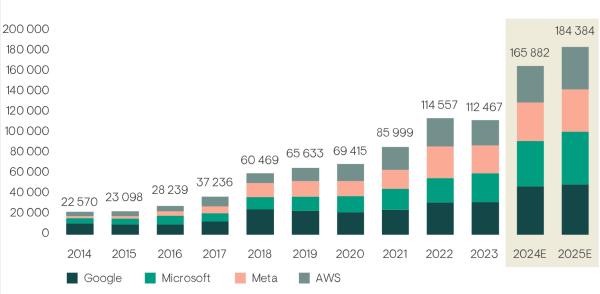

From an investment perspective, AI use cases have been relatively narrow and focused on the technology sector – the advent of targeted adverts, for instance – with the large incumbent tech firms the main winners to date. But open source – code that is more widely available – has allowed companies across many more sectors to make advances, and governments are also investing as they view AI as an engine of growth. Major tech firms are investing heavily to capture some of this growth potential, as illustrated by their respective capex expansion.

Figure 1: Hyperscale Capex (US$m)

Source: Ninety One, Bloomberg ¹

We find that investors typically overestimate technology in the short term and underestimate it in the long term. Valuations can therefore become disconnected from reality, as we saw most famously with the dotcom crash, and are arguably seeing today. With AI, financial markets are shooting first and asking questions later. Companies perceived as being at risk of disruption, e.g., those running outsourced call centres, have been derated significantly regardless of their earnings dynamics. In contrast, companies that are helping governments and businesses to implement AI today are seeing a re-rating.

There are many companies caught in the middle, at times viewed as victims of disruption and at times viewed as opportunities to tap into the AI theme, with market valuations oscillating accordingly. Looking further ahead, we think that uncovering the picks and shovels in addition to select software businesses that can monetise their products through subscription models will lead to the best outcomes for investors. Infrastructure companies are often persistent winners, as they are businesses that will benefit regardless of the ultimate destination. So far, for instance, returns have been concentrated into semiconductors – the likes of Nvidia1 which sells graphic processing units (GPUs) – but if history is a guide, returns are typically shared out over the longer term.

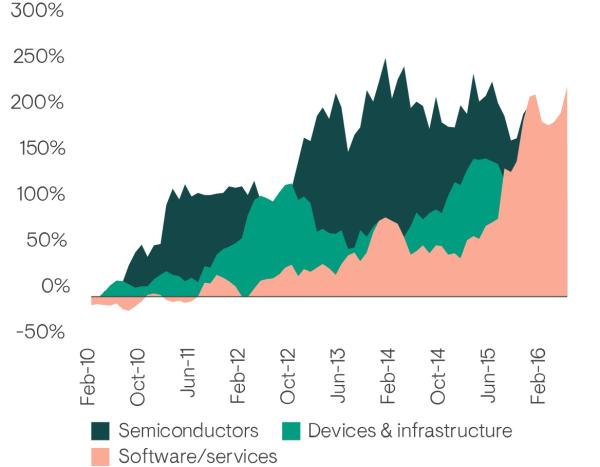

Figure 2: Is AI growth sustainable?

Mobile Cycle Relative Returns (%)

Source: Ninety One, Bloomberg, Based on analysis by Morgan Stanley. Semiconductors – based on equally weighted performance of ARM/QUALCOMM, Devices & Infrastructure based on equally weight performance of Apple/Samsung, Software & Services based on equally weighted performance of Alphabet/Amazon all in USD relative to MSCI ACWI, Feb 2010 – Jun 2016.

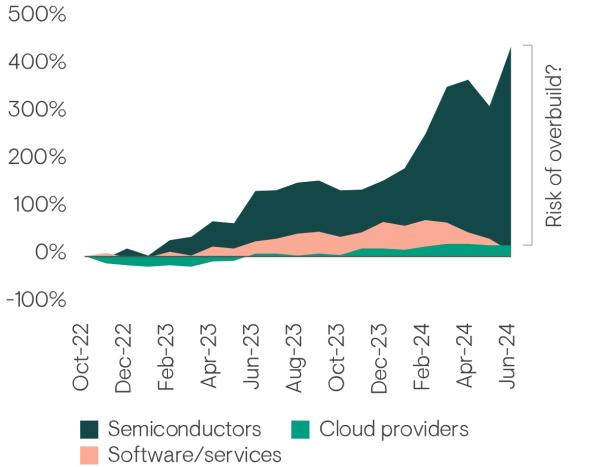

AI Cycle Relative Returns (%)

Source: Ninety One, Bloomberg. Semiconductors – based on equally weighted performance of Nvidia/AMD, Cloud Providers based on equally weight performance of Microsoft/ Amazon, Software & Services based on equally weighted performance of Adobe/Salesforce all in USD relative to MSCI ACWI , Oct 2022 – Jun 2024.

This is our approach to AI at Ninety One, while sticking to the quality characteristics that define our universe. A company must have high quality profits, attractive growth rates, superior profitability and low leverage for us to consider inclusion to our portfolio. Encouragingly, many of our holdings are exploring and investing in exciting ways to use AI, be it in payments and fintech, health and beauty or within the software space itself.

A few companies in the top 10 of our Global Franchise portfolio2, where we have meaningful positions and where AI is an even stronger theme, are worth highlighting. These include Microsoft as a clear leader in generative AI; Azure AI, which provides key cloud-based infrastructure and services for AI models; the monopoly provider of mission-critical equipment used by computer chip manufacturing companies, ASML; AI pioneer, Alphabet; and Google Cloud Platform, which provides infrastructure and services for AI models and, and through its own AI tool, Gemini, is integrating AI solutions across a wide range of applications.

Overall, therefore, we believe we have meaningful exposure to the AI theme. Importantly, we believe this exposure to be higher quality, more diversified and more sustainable than a concentrated bet in stocks entirely dependent on AI spending where performance has run hard recently.

¹ No representation is being made that any investment will or is likely to achieve profits or losses like those achieved in the past, or that significant losses will be avoided. This is not a buy, sell or hold recommendation for any particular security.

² The portfolio may change significantly over a short space of time.