Misunderstood hedge funds neglected in portfolio construction

Otshepeng Sokhela, Portfolio Risk Manager at Novare Investments.

Because the gatekeepers to financial services in South Africa, including consultants and independent financial advisers, find it difficult to explain to investors and trustees the methods employed by hedge funds to extract alpha from markets, these funds are often excluded when constructing portfolios.

According to Otshepeng Sokhela, Portfolio Risk Manager at Novare Investments, “Hedge funds are amongst the most misunderstood funds in the asset management industry. Despite the diversification benefits they bring to a balanced portfolio, hedge funds are often left out when constructing portfolios for institutional investors.”

According to the Association for Savings and Investment South African (ASISA), as at June 2014 the collective investment scheme (CIS) industry had R1.7 trillion in assets, compared to the hedge fund industry which, according to the 2014 Novare Hedge Fund Survey, had R53 billion in assets - representing 3% of collective investment scheme assets.

“The biggest misperception about hedge funds is that they invest in risky assets. The fact is hedge funds invest in the same instruments available to traditional long only asset managers, the main difference being that hedge fund managers have more investment tools at their disposal.

“These include using short selling and leverage as alternative sources of return. When used appropriately these tools can help manage risk within a balanced portfolio to produce superior risk adjusted returns, and to protect capital during market downturns,” said Ms Sokhela.

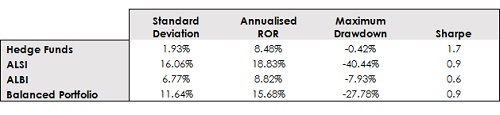

According to HedgeNews Africa, which tracks hedge fund returns, the South African single manager hedge fund composite index has proven over time to have provided less volatile returns while protecting on the downside.

This is evident from an analysis of historic annualised returns and risk statistics from March 2004 to August 2014 for the All Share Index, the All Bond Index, the HedgeNews Africa South African Single Hedge Fund Manager Composite index and a simulated balanced portfolio made up of 60% equities and 40% bonds.

Local hedge funds have a different risk return profile to equities and bonds, with the volatility in monthly returns of hedge funds lower than that of both the ALSI and the ALBI, resulting in the Sharpe ratio, which measures risk adjusted returns, being higher for hedge funds.

What happens in a balanced portfolio when introducing hedge funds is that there is reduced standard deviation (volatility) in the portfolio, improved maximum drawdown and a higher Sharpe ratio.

“According to Regulation 28 of the Pension Funds Act, retirement funds can invest up to 10% of their total portfolio in hedge funds. With the regulation of hedge fund products having been addressed, there is additional comfort for investors contemplating hedge funds. This, together with a better investor understanding of hedge funds, will result in greater investor interest in the diversification and risk reducing benefits of including these funds in a balanced portfolio,” said Ms Sokhela.