Missiles, markets and murk

In summary

• The oil price has surged in the wake of US and Israeli attacks on Iran.

• This will put downward pressure on global growth and upward pressure on inflation, but the impact depends on how long prices stay high.

• Markets are likely to be very volatile until there is some indication of the conflict easing, meaning investors will have to be vigilant and patient.

The Middle East is ablaze again. The US and Israel have attacked Iran, and it has retaliated by launching missiles and drones into neighbouring countries. This is first and foremost a humanitarian crisis, but it also has implications for the global economy. The longer the war drags on, the more pronounced the impact on economic activity. Though it seems increasingly unlikely, a speedy resolution should leave little lasting scars on key international financial metrics. Either way, Iran itself will never be the same again.

The reason why conflict in this part of the world matters so much is simply because the Middle East is the world’s biggest oil-producing region, and that includes Iran itself. Moreover, the geography of the Gulf creates a unique chokepoint in the Strait of Hormuz, a narrow maritime channel that carries about 20% of global seaborne crude. Around a hundred ships, mostly oil tankers, usually pass through the Strait every day. However, it is now effectively closed, largely because insurance companies refuse to cover vessels that travel through it.

This also impacts other goods produced in the region, such as plastics, fertilisers and aluminium. Moreover, the Gulf is a global hub for air travel, with around 500,000 passengers passing daily through the Abu Dhabi, Dubai and Qatar airports in normal times. This means that millions of travel plans have been disrupted, reaching the farthest corners of the earth. Nonetheless, oil is the key variable to watch.

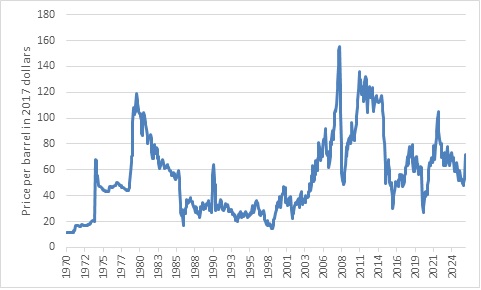

Chart 1: Brent Crude oil price adjusted for US inflation

Source: LSEG Datastream, as of 9 March 2026

Given the risks to oil supply, the spike in the price of crude is not surprising, though it is from a low base, since global oil markets appeared to be well-supplied around the start of the year. Brent crude oil jumped above $100 per barrel on Monday morning, a level last seen in 2022, but not yet extreme by historical standards when adjusted for inflation as chart 1 shows. Previous oil price spikes related to geopolitical crises were more severe, including in 1973 (Yom Kippur War), 1979 (Iranian Revolution), 1990 (Iraq invasion of Kuwait) and 2022 (Russian invasion of Ukraine). The biggest surge, leading up to 2008, was not due to war but part of the broader commodity super-cycle, and notably the narrative of “Peak Oil Supply.”

The outlook for the oil price remains very uncertain, but risks are tilted to the upside. Iran was already weakened militarily, politically and economically before the attacks and is fighting against the largest and most advanced force the world has ever known with depleting stocks of missiles. However, we’ve seen in Ukraine how an underdog can endure for longer than expected. When Iraq invaded Iran in 1980, the war lasted eight years. Moreover, even if Iran is defeated in the conventional military sense, smaller decentralised militias can carry on fighting with cheap drones, rocket launchers and speedboats, causing damage to energy infrastructure. From investors’ point of view, it is particularly worrying that there doesn’t appear to be clarity about the American war aims, making it difficult to gauge when and how the conflict might end.

This stands in contrast to the June 2025 “Twelve Day War”, when the US and Israel had the clear goal of destroying Iran’s nuclear capability and Iran chose not to escalate. An uneasy ceasefire was quickly priced in, and calm returned to financial markets. Today the market is looking for an offramp from this conflict, and none are yet in sight.

Pain at the pump

Higher fuel prices will weigh on global growth, since households and businesses will have less money to spend on other things. The longer the conflict drags on, the bigger the chance of serious damage to energy infrastructure in the region, ongoing price pressures and negative consequences for the global economy. The increased uncertainty might also result in spending decisions being postponed. As a rule of thumb, a sustained $10 per barrel increase in the oil price reduces global economic growth by about 0.1 to 0.2 percentage points. That doesn’t sound like much, but 0.1% of $100 trillion annual global economic output is a lot and will amount to lower earnings for a broad range of sectors, though of course there are winners and losers, both across industries and countries. Moreover, this heuristic does not incorporate feedback loops from financial market distress. There is a difference between a smooth $10 increase in oil prices, and a sudden spike which triggers panic selling in financial markets (more on this below).

Click here to read more...