Midpoint musings

At the midpoint of an eventful year, what does the investment landscape look like? Though there will always be some areas of weakness and lurking risks, broadly speaking, the environment seems positive.

Known risks tend to occupy investor’s minds and are therefore also largely discounted in markets. It is the unknown or surprise outcomes that cause real market volatility. The string of recent unexpected election outcomes is a case in point. While it was common knowledge that France has high government debt levels and a rising political right, few worried about it until the prospect of a populist government suddenly emerged following President Macron’s unexpected calling of a snap election.

Getting to grips

The most important thing for investors, however, is the global growth, inflation and policy picture. More precisely, it is the United States (US) outlook that matters most, given that it makes up a fifth of the global economy but more than half of global financial markets. Other major economies – Europe, China, Japan – are not irrelevant, the US just counts for more.

At a high level, US growth is still solid, and indeed its performance has been remarkable. As the International Monetary Fund (IMF) pointed out last week, the US is the only G20 economy that is bigger than what the pre-pandemic trend would have predicted. The others have mostly recovered Covid-related losses but are still smaller than they would have been had there been no pandemic.

American consumers continue to benefit from rising real incomes as a tight labour market supports wage growth while declining inflation means those dollars can buy a bit more than before.

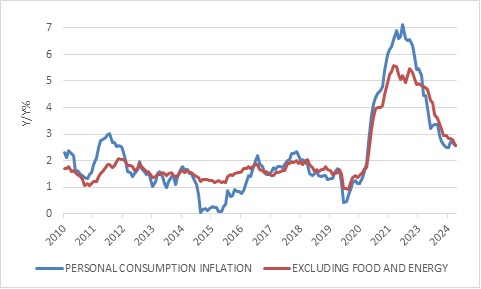

This doesn’t mean that everyone is happy. Though inflation (the rate of change of prices) is down from a peak of 7% to around 3% today, the price level is more than 20% higher than before the pandemic. Goods and services cost much more than before, and this matters more to the Average Joe than economists rambling on about lower inflation.

Chart 1: US inflation

Source: LSEG Datastream

Moreover, there is a distinction between haves and have-nots. People who own assets such as houses and equity portfolios have seen these appreciate in value. Overall household net wealth (assets minus debt) is near record levels. Since mortgage rates tend to be fixed, most homeowners are unaffected by the surge in interest rates. On the other hand, people who don’t own a home have not only missed out on rising house prices but are also forced to rent in a market where rentals have surged. Those who were hoping to buy a house have been locked out by the combination of high interest rates and high house prices that has left housing affordability at record low levels.

It means that housing activity, one of the US economy’s key cyclical sectors, is running unusually low. In other words, though the overall economy is resilient, high rates are clearly squeezing certain areas. This includes durable goods orders, which are not growing, while the problems in commercial real estate are well known. Another area is small business. Many large businesses could lock in low interest rates by issuing bonds. Smaller firms rely on banks and often pay variable rates. High interest rates hurt them, as do rising staff costs. If sales growth starts cooling, many could face problems.

So, while the S&P500 has had a good first half of the year, driven mostly by a handful of large technology companies, the small cap Russell 2000 index has moved sideways. Outside the US, developed markets are positive for the year, but lag the S&P500. Ditto for emerging markets. This is partly a dollar story, with the trade weighted dollar index 4% higher in the first half.

Click here to read more...