Maybe There Is No Such Thing as Passive Investing?

Reframing a Debate That’s Gone on Too Long

The active versus passive debate has long been a fixture in the investment world. Often framed in binary terms, it suggests that investors must choose between costly human intervention and cost-efficient automation. But the reality is more nuanced. What if the difference between active and passive is not so much about method as it is about mindset?

While passive investing plays a valuable role in portfolio construction, it’s rarely as neutral as it’s made out to be. Even the most rules-based, index-tracking investment involves a range of embedded choices. Recognising those choices helps us use passive tools more effectively, not dismiss them.

Passive in Name, Active in Nature

Passive investing is often described as hands-off and objective. In practice, it's anything but. Every index is a human creation, designed with intention, shaped by assumptions, and revised over time.

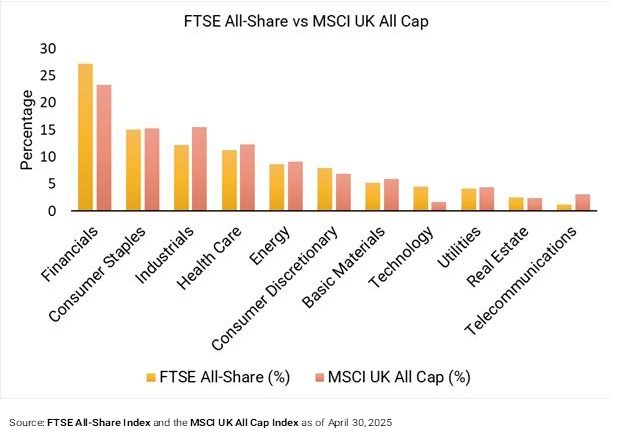

Take the FTSE All-Share and the MSCI UK All Cap. Both are designed to represent the UK equity market, yet they differ significantly in their construction. These differences arise from variations in index construction and stock inclusion criteria, leading to materially distinct allocations across areas such as financials, industrials, and consumer goods. What seems like a minor structural choice can result in very different investment outcomes over time.

Even within the same index, implementation choices matter. One provider may replicate fully, another may sample. Some may engage in securities lending, others may not. Policies around rebalancing, cash handling, and execution quality vary widely. None of this is passive.

Then there's the S&P 500, one of the most widely used indices in the world. It isn’t rules-based in the purest sense; it has a selection committee that decides which companies qualify for inclusion. These are decisions, made by people, that affect every investor tracking that index.

Understanding Market Concentration

One of the more frequently raised concerns about passive investing is rising market concentration. It’s true that many indices today are heavily weighted towards a small number of companies, particularly in the U.S. technology sector.

This isn't necessarily an error in the system. History suggests otherwise. Research shows that just 120 companies have accounted for over 60% of U.S. equity wealth creation between 1926 and 2022. Concentration, in other words, may be a feature of capital markets – not a flaw of index design.

Click here to read more...