Markets are ruled by fear

Kokkie Kooyman, portfolio manager at Denker.

It has been a bear market for most major world indices for some time and added volatility has sent stock markets tumbling. With increased geopolitical events impacting the world, Kokkie Kooyman, portfolio manager at Denker Capital (previously SIM Global) attempts to make sense of what events are impacting institutional investors globally.

Global markets

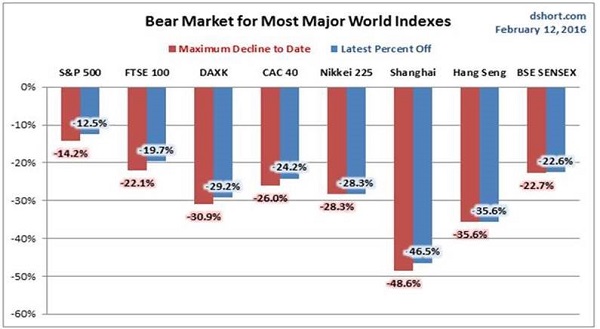

At the start of January 2016, the Dow Jones Industrial Average had its weakest start to the year since 1897, and fell by more than 5% in its first four days of trading in 2016. The Nasdaq did even worse, down more than 7% (the last time it did as badly was in 2000, the year the dot.com bubble burst). It was also the worst time in history for both the Dow Jones and S&P 500 index, with losses beating the previous lows of 2008. Now a month later, markets are not faring much better.

(Period: January 2014 to February 2016; source: Sanlam Private Wealth)

Using major world indices as a means of comparison, the graph above illustrates the pressure that equity markets worldwide are under. Global headwinds remain, and it seems 2016 is going to be a tough year.

But before you think about selling, you might want to stop and think, says Kooyman. Don't panic. As fiduciaries responsible for the wellbeing of your fund members, you may feel like pulling your money out, but put things into perspective: remember that most of the market’s ten best days over the last 20 years occurred within two weeks of the ten worst days…

This is why fund managers welcome negative sentiment. It is during these sell-offs that the best investment opportunities present themselves.

What is driving the relentless fall of the market?

Panic and euphoria

According to popular behavioural finance, human beings have an innate belief that the current status quo will continue and find it difficult to accept change. Hence we find it difficult to make decisions and initially default to doing nothing, but then act when it is too late (“status quo bias”). This behavioural bias is typical in financial bear markets. Widespread pessimism causes negative sentiment to be self-sustaining and increases as the selling continues. Eventually, when investors anticipate only more losses they react and sell at the bottom.

Warren Buffett correctly says it’s not intelligence that counts with investing, its emotional strength. He says: the best time to invest is when everyone assumes a bad outcome and the negativity has become pervasive. Why?

Because actual outcomes are seldom as bad as expected

The excess liquidity glut of the past 20 years (thanks to low interest rates and to quantitative easing) has led to poor capital allocation. Now markets are grappling with how much damage is hidden, how many Enrons, Lehmans and others are lurking below the sea of liquidity.

We don’t understand deflation where the absolute value of debt stays the same while asset prices deflate. We don’t understand negative interest rates, and we don’t know how to price assets in such an environment.

What we do know is that historically markets always recover after a significant correction (or bear market). In the cold light of day, it becomes apparent that the large sell-offs were driven by the combination of leverage (investors who purchase on debt) and panic (investors worry irrationally that the market fall will continue forever).

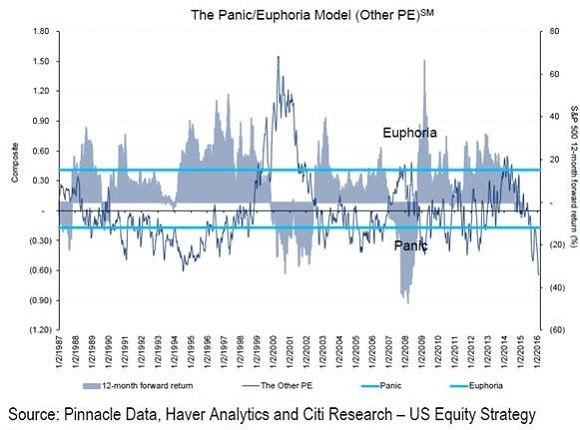

The panic/euphoria graph below highlights that, just like in 2008, panic is currently pervading the markets:

We can identify 4 fears that are fuelling the bears:

1. China’s growth slowdown

China has been a source of angst for everyone in the global financial markets for several years. China’s economic deceleration and shift to a consumer-driven economy is putting the brakes on the global business cycle. While both are part of a natural evolution, this nevertheless still poses structural challenges to emerging markets and commodity producers. Risks, including that of a remnimbi (or yuan) devaluation, are rising.

What effect will this have on the rest of the world?

For years China managed to grow its economy at a rate exceeding 10% and even last year managed 7%. This growth was powered by massive infrastructure projects and large cities were built. However, this era of infrastructure spending has come to an end and, with it, the demand for commodities. Unfortunately, however, the mining and related industries continued their expansion as if the demand from China would last forever. This has resulted in a global oversupply of many commodities, such as cement, steel, copper, oil and platinum.

As a consequence, we have seen a high debt burden in China, which is a major problem for the Chinese government and banks, and also a problem for the mining industry. Secondly, the remnimbi has become too expensive and could depreciate by some 15% to 20% during 2016, making their exports more competitive and thereby helping to ease the pressure on the economy. The impact of this (China’s slower growth and lower remnimbi): global deflationary pressures. And global deflationary pressures mean continued pressure on bank interest margins (NIMs).

2. The pain of the mining and oil & gas industries

The knock-on effects of the movements in oil prices and the US dollar are critical. Falling oil prices have dragged down long-term global inflation expectations, bringing into question the credibility of central bank inflation targets. On the other hand, the dollar’s rise has led to some tightening in financial conditions.

Initially many producers reacted to lower prices by increasing their outputs, particularly oil producers. Ultimately however, the collapse in oil and other resource prices will eventually start to affect supply and should therefore increase demand.

So how long before prices rise?

Nobody really knows. In all probability we’ll first see defaults (e.g. by energy companies) and bankruptcies, which eventually will help to normalize price levels; bad news for high-yield debt investors and banks.

3. Quantitative easing has had the opposite of its desired effect

For years now, financial markets have been dominated by the world’s central bank policy of extraordinary monetary stimulus (QE). Designed to stimulate demand, consumer spending, bank lending and mild inflation (and also inflate asset prices), it had an unintended consequence: aging populations are choosing to rather pay off their debt and increase their retirement nest egg. Despite lower interest rates (negative in Japan, Sweden, Denmark and Switzerland) and lower unemployment, the savings rate in the US has actually increased. Low interest rates means that retirees need a larger savings pool to retire.

4. Europe’s persisting banking problem

At the end of the 2008 financial crisis, the US took immediate action, forcing banks to put in place measures for questionable loans and ensure capital adequacy. Europe’s reluctance to follow suit, however, has resulted in the fact that 7 years after the 2008 crisis, Italian banks have a significant percentage of bad debts on their books while banks like Deutsche, Barclays, Credit Suisse, Commerzbank, etc. remain in restructuring mode.

The end game? Governments will eventually be forced into long-overdue structural reforms like unloved austerity measures, reducing red tape, lowering tax rates (which means reducing government spending) and making labour more flexible.

Until then, we continue to brink on a deflationary, low interest rate, low-growth world.

The positives:

- Compared to history and 2008, the banking system is significantly better capitalized,

- It has improved cash reserves,

- non-performing loans have decreased,

- and the sector is better regulated and supervised.

Since 1 Jan 2009, banks have grown their loan books by less than 2% compounded - meaning the risk of new asset bubbles on bank balance sheets is low.

Oil and gas and high-yield debt exposure make up a manageable 1% - 8% of banks loan books (the average of the global top 50 banks is 1.9%). This could affect the profitability of a few individual banks, but again, the loans have collateral and the exposure does not present a systemic threat.

In summary, the above events present challenges to bank profitability, however the banking system does not present a systemic risk to world growth (with the exception of Chinese banks).

Uncertainty brings price falls:

- The combination of lower interest rates (which means continued pressure on net interest margins and return on capital) and the risk of higher bad debts, has brought about uncertainty.

- Until we see debt defaults, the market doesn’t know which banks have the high risk exposures (although past track records do give a good clue)

However, by virtue of the 25-28% YTD price falls, it seems the bad news is largely priced in. Relative to the past, banks are now attractively priced, particularly emerging market banks. Throughout the crisis years the better quality banks have continued to deliver a high return on capital and are well positioned to continue doing so.

What should investors do in these markets?

We’ve had a panic sell-off. Will markets fall further? We don’t know. But what we do know is that when there is panic, good companies are pushed to their current low valuation levels, which is a long-term win for investors.

Good companies are managed by innovative, competent managers, well versed in market volatility. They are paid to react to challenging circumstances. Market panics and dramas come and go and it is almost impossible to time the markets successfully. Right now, while your instincts may be shouting that it’s time to sell, the question remains: will you be able to identify those subtle signals correctly and at the right time when the market suddenly recovers? History has proven this unlikely.

It is noticeable that 2016 is following the 2008 pattern: During the sell-down the market is largely indiscriminate in what it sells in its flight to cash. However, in the subsequent rebound investors are selective in what they buy.

Financial shares in both developed markets and emerging markets have been sold down to more than 50% discount to intrinsic value and, in many cases, more than 50% discount to tangible book value. When the mood changes the reversal can be dramatic.

Summary:

The outlook is troubling, but this was also the case in 2008.

1) Trust your asset manager to invest in businesses with rational managements, good business models and strong balance sheets

2) Think long-term: the outlook is troubling, but remember that this is not dissimilar to the events that sparked the market crisis in 2008.

Now is the time to start thinking about how a portfolio should be positioned when the spate of selling subsides.

The objective of this article is to give insight into the numerous fears that have been driving the equities sell-off and not to “talk you in or out of the market”. But over time, a value-based approach has outperformed growth. The outperformance of “growth” versus “value” in recent times has been extreme. Certainly, recent events have alerted investors to the risks of too high expectations but at least expectations have been re-set and value stocks have started outperforming again.