Many moving parts moving in different directions

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

The past few days have been unusually eventful, with a bunch of important economic data releases, central bank policy announcements and political developments. And of course, the usual market ups and downs, as investors respond to the above, and also because investors often just react to price movements, instead of to changes in fundamentals. They also like nice round numbers, as the hoo-ha over Apple becoming the first $1 trillion company showed.

Data deluge

Starting with some of the key global data releases, the JPMorgan Global Manufacturing Purchasing Managers’ Index was slightly weaker in July, but at 52.7 index points it is still in positive territory. Since the trade tensions play out in the goods sector (i.e. manufacturing) rather than services, this is significant. While there is some evidence of the new tariffs causing disruption in new orders and supply chains and global manufacturing growth has lost momentum since the start of the year (more so in Europe and Asia than in the US), overall it is still solid.

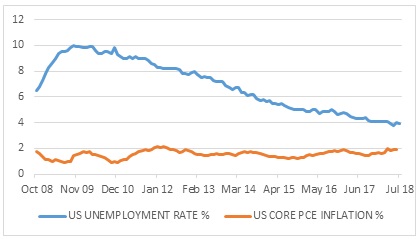

In the US specifically, payrolls data showed 157 000 new jobs created in the non-agricultural economy, somewhat below expectations, while the unemployment rate dipped to 3.9%, a two-decade low. Wage growth, at 2.7%, has not accelerated despite the low unemployment rate. There is a still a sizable group of people on the side-lines not looking for work. As they are lured back into the labour market (and the so-called participation rate rises), some of the upward pressure on wages will reduce. The other reason is simply that the power balance between workers and employers has been comprehensively tilted in favour of the latter.

Nonetheless, with decent growth in wages and employment, household disposable incomes are growing nicely (5.4% in the year to June), supporting personal consumption spending growth at a robust clip (5.1%). Importantly, the savings rate of households, which theoretically is simply the difference between income and spending, has been recalculated and at a reasonable 6.8% it is almost double what it was believed to be. A key vulnerability of the household sector is therefore less than previously thought.

The inflation rate on personal consumption and not the consumer price index is the Federal Reserve’s (the Fed’s) favoured measure of price pressures since it incorporates short-term shifts in spending patterns. It was 2.2% year-on-year in June, and 1.9% if volatile food and fuel prices are excluded.

Fed on hold, but not for long

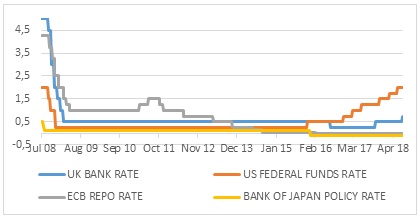

In other words, as we turn to the central banks, the Fed’s dual objectives have, broadly speaking, been met. Inflation is close to the 2% target and unemployment is about as low as it can go. While the Fed did not hike at its meeting last week, it is almost certain to do so in September, and this is what is currently priced in. This meeting will also provide an updated assessment of the economic and inflation outlook, which will inform investors’ perception of the path of future rate hikes. If this expectation changes, it could result in sizable moves in financial markets.

The Bank of England hiked rates for the second time in a decade. It faces the dilemma of above-target inflation on the one hand (partly due to a weaker currency) with the tremendous uncertainty surrounding the UK’s exit from the European Union next March on the other. As things stand, there is no post-Brexit arrangement, and in the absence of a deal, a “hard Brexit” will see customs barriers go up again for the first time in decades. There are already reports of medicines being stockpiled to mitigate potential post-Brexit supply disruptions.

The Bank of Japan (BoJ) quashed speculation of a major shift in its policy stance, which had put pressure not only on Japanese bonds (with yields jumping) but also on bonds in other developed markets. The BoJ pledged to keep rates at “extremely low” levels, but gave itself a bit more leeway in its aim of pegging the ten-year government bond yield around zero. This will of course be tested by traders and at the end of last week the ten-year bond yielded 0.12%. The US equivalent, probably the most closely watched yield in the world, touched 3% again for the first time since May, pricing in expectations of solid growth and rising rates, but clearly not runaway inflation or surging interest rates.

Finally, the Reserve Bank of India hiked its policy rate for the second time since June as inflation, particularly food inflation, rises. While Indian monetary policy does not directly impact South African markets in the way that the Japanese and especially American versions do, it does create a reference point for the South African Reserve Bank (SARB), making it more difficult to deliver the rate cuts the struggling local economy needs.

Mixed bag

Recent local data has been mixed, but generally weak. SARB noted a slight increase in borrowing by households and corporates, but credit growth is barely outpacing inflation.

The local manufacturing PMI moved into positive territory in July, hopefully signalling that the second half of the year will be an improvement on the dire first half. Apart from the fact that manufacturing production has been flat to negative in 2018, the sector shed 105 000 jobs in the second quarter. Overall, the unemployment rate rose to a staggering 27.2%, with 6 million South Africans involuntarily out of work, while another 2.8 million have given up looking for employment (and are therefore not captured in the unemployment rate).

New vehicle sales, a key indicator of consumer and business confidence, as well as credit conditions, picked up marginally in July from a year ago, according to industry body Naamsa. This was largely due to a 4% year-on-year increase in passenger cars. In contrast, sales of light commercial vehicles declined 2% from a year ago. In the low volume truck market, around 2 315 units were sold, which represents an encouraging increase compared to July 2017.

South Africa posted a surprisingly large trade surplus in June, narrowing the deficit for the first six months of the year to R1.7 billion. However, this still represents a R24 billion swing from the first half of 2017. While there are many moving parts to the trade balance (literally), the big change has been in the mineral products category, where oil imports have surged while exports of iron ore and coal have dipped, largely due to relative price changes. The other notable point about the trade balance is that South Africa has a R43 billion year-to-date surplus with Botswana, Namibia, Swaziland and Lesotho, our fellow members of the Southern African Customs Union (SACU), but a R45 billion deficit with the rest of the world. However, our exports to the SACU countries don’t necessarily earn us the hard currency we need to fund imports from the rest of the world.

Trump’s trade battles resume

On to political matters, US president Donald Trump appears to be mulling over an increase of tariffs from 10% to 25% on $200 billion of Chinese imports. The Chinese yuan lost 8% against the dollar since early April, largely neutralising the threat of the initial tariffs. The apparent thaw in trade relations has been short-lived. China has again promised to retaliate and this contributed to further wobbles on world equity markets.

Don’t bet the farm

Locally, the big political development was the announcement that the ANC intends to pursue a constitutional amendment to explicitly allow for expropriation of land without compensation. The proposed wording of the amendment is not known. As with the trade issue, the uncertainty this causes is potentially more damaging for the economy than the actual outcome. However, as far as the JSE, the rand and the local bond market are concerned, policy changes from the Fed’s Eccles Building in Washington are typically more important than anything emanating from Luthuli House or the Union Buildings. Our local markets are deeply intertwined with global markets.

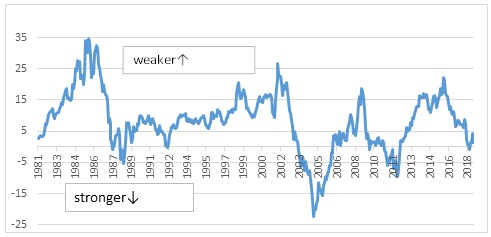

As with any other headline-grabbing development, overreacting would be a mistake. A thousand things that influence your portfolio in unpredictable ways could happen before any law is changed. Being appropriately diversified is the best defence against this uncertainty. This includes having plenty of rand-hedge exposure – as is the case with our Strategy Funds. Since being allowed to float freely in the early 1980s, the rand has often acted as a shock-absorber, and investors should use this to their advantage. Over this period, the general trend has been for the rand to weaken against the dollar, but there have been long periods (uncomfortably for some) when it appreciated. Since no one has perfect foresight, spread your risk.

Chart 1: Policy interest rates of the major central banks

Source: Thomson Reuters Datastream

Chart 2: The Fed’s twin targets: US unemployment and core inflation rate

Source: Thomson Reuters Datastream

Chart 3: Rolling three-year annual percentage changes in the rand-dollar exchange rate

Source: Thomson Reuters Datastream