Making America Guess Again?

The past five to ten years have seen tremendous change across the world, politically, economically and socially. Wars, pandemics, election upsets, disruptive new technologies, we’ve apparently seen it all.

One underlying theme, however, has been the relative strength of the US economy, the world’s largest.

The US was at the epicentre of the 2008 global financial crisis and was devasted by it. But once recovery was underway, it outperformed other major developed economies. While China is still growing faster in absolute terms, at least according to official data, relative to lofty expectations China’s economy has struggled in recent years. US equities have comfortably outperformed most other markets over the past decade or so, and the dollar has gained against other currencies. The US re-emerged as a global fossil fuel superpower thanks to fracking but is also at the forefront of the emerging artificial intelligence (AI) technologies.

In other words, when Donald Trump promised to make America great again, he faced a major obstacle: from such a strong base, further outperformance was always going to be difficult. US corporate profit margins are already near record levels, the dollar is already very strong, the US is already pumping record quantities of oil and unemployment is already low. It is a simple fact of economics and finance that growth is easier off a low base when expectations are depressed than off a high base with little room for positive surprises.

The other major obstacle Trump faces is himself. Whether or not he is implementing a grand strategy to rewire the US and global economies, or simply aiming for a series of tactical negotiated wins, “Art of the Deal” style, we don’t know yet. Markets rallied after his election on the assumption that it’s the latter, and that he would be pro-business. But his focus so far has been on tariffs, immigration and foreign policy. This creates uncertainty and does nothing to boost growth. In fact, it may be doing the opposite.

It has been a remarkably busy first month in office for Trump. Some of his actions, such as firing perceived opponents from senior positions was always likely. It was also expected that he would threaten tariffs on countries with whom the US has a trade deficit and put pressure on allies to conform with his world view, including pushing Europe – rightly– to spend more on defence. It was expected that he would push Ukraine to the negotiation table with Russia.

What was not expected was that Trump would seemingly punish friends more than foes when it comes to tariffs (Canada more than China) or that he would cozy up to Russia’s Vladimir Putin, blame Ukraine for the war and demand a share of Ukraine’s mineral wealth. Or threaten to annex Greenland or the Panama Canal. Again, all this might be a negotiation tactic, or it may be a serious attempt to alter the global geopolitical landscape. But it creates uncertainty either way.

What was also not expected was that he would give the billionaire Elon Musk, who is neither a government employee nor an elected official, free rein to take an axe to the civil service. While the job cuts so far are small in the context of a three million federal government workforce, they seem indiscriminate and reckless, rather than a careful reprioritisation of government activity or attempts to save money. For instance, Musk cut thousands of workers at the Inland Revenue Service, the US equivalent of SARS. This will harm tax collection and could therefore end up widening the budget deficit, the opposite of what he claims to achieve.

As an aside, the level of federal employment has been fairly steady around three million over the past five decades even as the population has grown. Though there is obviously some waste in such a large system, this does not seem to be bloated civil service. Either way, many government employees surely fear for their future now and might hold back on big purchases. Though American households sit with record levels of cash, most of that is concentrated in the hands of the rich. Less affluent families might start building savings buffers.

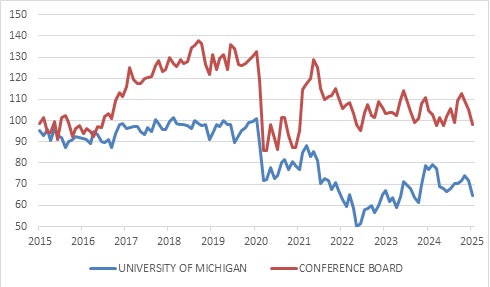

Chart 1: US consumer sentiment indices

Source: LSEG Datastream

With consumer spending at robust levels coming into the year it was always likely that things would slow. The head-spinning pace of change unleashed by the White House in recent weeks might just accelerate the process. The two best-known consumer confidence indices rose in the wake of the November election but pulled back sharply in the January and February readings. People seem unsettled, particularly at the prospect of tariffs raising prices. It is possible to read too much into consumer sentiment surveys, since the US population is deeply divided, and political views might colour their perception. The decline is telling, nonetheless.

The health of the American consumer remains at the core of the US, indeed global, economic outlook. Importantly for now, despite Musk’s job cuts, broader indicators of job losses remain stable. However, this can change and is something to pay close attention to, especially since US interest rates relief has been limited.

One of the factors behind the unexpected strength of the US economy in the past three years has been how shielded households were from the great global interest rate surge. Across Europe, Canada, Australia, South Africa and more, higher central bank interest rates fed into rising mortgage rates, and a growing debt service burden for households. Not in America, where mortgage rates are mostly fixed, keeping the interest burden low. But it also means that consumers in these other countries are now benefiting from falling rates, in a way that American homeowners aren’t. The mortgage rate in the US remains around 7%, and the housing market remains frozen. Sales activity is depressed, as are leading indicators. The Federal Reserve, meanwhile, has paused its cutting cycle unlike central banks elsewhere, since inflation has been sticky in the past few readings.

Click here to read more...