Looking for measured consolidation and faster growth

Dave Mohr, Chief Investment Strategist at Old Mutual.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

The message from Finance Minister Gordhan at this year’s Medium Term Budget Policy Statement (MTBPS) was one of “measured consolidation” and a call to tackle South Africa’s problems in a committed, coherent and coordinated way. Government will take steps to reduce its budget deficit (the difference between spending and revenue) over the next three years. Closing the deficit too quickly – through a combination of spending cuts and tax increases – risks tipping the economy into recession and worsening the debt-to-GDP ratio, instead of reducing it (ask Greece). Closing it too slowly, especially relative to promises made, risks a loss of credibility, ratings downgrades, and therefore higher borrowing costs that will end up increasing the debt ratio.

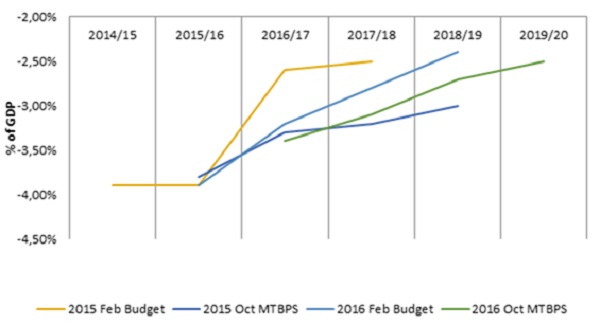

This fiscal year’s headline deficit of 3.4% of gross domestic product (GDP) will already be smaller than the previous year, so there is some evidence of consolidation in action. However, the path of consolidation will be more gradual than projected in February and is expected to narrow to 2.5% by the 2019/2020 fiscal year, instead of 2.4% in 2018/19 as per the February Budget.

Tax revenue shortfall

The reason is weaker economic growth than expected in February. Back then, the economy was projected to grow by 0.9% in 2016, climbing to 2.4% in 2018. Even at the time it was considered a touch enthusiastic – after all, the previous three years’ forecasts proved to also be too optimistic. These have now been revised to 0.5% for 2016, 1.3% for 2017, rising to 2.2% in 2019.

As a result of the slower growth (but also due to a change in the composition of growth), revenue will be R23 billion less in the current fiscal year than expected in February, with the shortfall rising to R52 billion in 2018/19.

To address this, an additional R28 billion will have to be raised next year. Unless the economy suddenly overshoots all expectations, this will have to come from new tax initiatives likely to be announced in February 2017, informed by the work of the Davis Tax Committee. This could include a combination of the sugar tax, fuel levy hike or a new top tax bracket (or similar wealth tax). The easiest way is to simply allow inflation to silently push individuals into higher tax brackets without the usual compensation for ‘bracket creep’. A VAT increase is unlikely in a weak economy, but the overall prospect is unfortunately not a happy one for South African taxpayers. The overall tax burden (tax as a percentage of GDP) will rise by 1.8%, but this remains broadly in the middle of our global peer group.

On the spending side, the expenditure ceiling remains in place, which is crucial since it limits how much Government can spend on non-interest items and is an important statement of Government’s commitment to spending discipline. In the February Budget, the ceiling was lowered by R25 billion from the previous year. In other words, the rate at which spending could grow was reduced. This was further cut by another R26 billion. This means that relative to last October’s MTBPS projections, Government will spend R51 billion less in total.

South Africa is not the only country trying to consolidate. After ten months without an official government, Spain’s People’s Party will finally form a minority government. Its first order of business will be to find a way to cut €5 billion from the 2017 budget to meet the European Union’s deficit target. Spain’s budget deficit was 5.1% of GDP last year, from a peak of 10% in 2012. However, the global obsession with debt and deficits, which led to ruinous austerity policies in many places from 2010 onwards, seems to be fading. This is partly due to lower government bond yields (borrowing costs). Spain’s government paid 4% per year to borrow over 10 years in January 2014; it can now borrow at 1%. For the US, government bond yields declined from 3% to 1.8% over the same period.

Market reaction muted

The reaction from the analyst community can be summarised as “credible but underwhelming”, as one economist put it. The market reaction to the MTBPS appeared negative, but of course it is difficult to disentangle the many factors that influence market prices over a short period. The JSE followed global markets lower. The rand immediately sold-off around 1% after the speech, but by the end of the week it had retraced its losses. The rand has been supported by higher dollar prices of South Africa’s main export commodities – gold, platinum, coal and iron ore (especially the latter two). The euro has been weaker and the rand typically follows the euro when it falls against the US dollar, but not this month. The UK pound remains weak, but lifted its head a bit after UK GDP for the third quarter was surprisingly robust. However, it is important to note that Britain’s relationship with the EU has not changed at all. The real adjustment begins after Britain has left the EU, and at this stage it does not seem as if the split will be entirely amicable.

The bond market is the most sensitive to Budget news, simply because any shortfall between revenue and spending has to be borrowed, implying an increasing supply of bonds on the market. Treasury estimates issuing R180 billon long-term rand-denominated bonds per year over the next three years to cover the deficit and redemptions. The 10-year Government bond yield (which moves inversely to the price) jumped from 8.8% prior to the MTBPS to 8.9% afterwards, but is below the 9.8% level in January at the height of global risk aversion. The bond market is also sensitive to perceptions of Government’s creditworthiness, and credit ratings are a factor investors take into account.

Ratings still at risk

It is the rating on foreign currency debt that faces the most immediate risk, since S&P Global distinguishes between rand-denominated debt and hard currency debt. The former is rated BBB+ and the latter BBB- (with a negative outlook for both). A likely outcome is for S&P Global to cut foreign currency-denominated debt to sub-investment grade level (“junk status”) but keep the rand-denominated rating at investment grade. Fitch has both ratings one notch above junk status, but with a stable outlook, while Moody’s has both ratings two notches above junk. The cost of insuring against a default on our foreign currency debt through credit default swaps (CDS) rose marginally after the MTBPS, but is much lower than earlier in the year. It still trades in line with other junk-status economies Brazil, Turkey and Russia.

Fortunately, South Africa does not have a lot of foreign currency debt. By 2019, Treasury expects net (of cash balances) Government debt to be R2.6 trillion, of which only R164 billion will be foreign debt. South Africa issued $3 billion in dollar-denominated 10 and 30-year bonds in September. The issue was oversubscribed and at a spread over US yields of just over 270 basis points. This will partly be used to manage foreign loan redemptions in 2019/20, providing some cover should market conditions become unfavourable.

Government should try to avoid a downgrade, but its credit rating is not the only factor that will influence its borrowing cost. Take the case of Brazil. S&P Global cut both its domestic and foreign rating to BB in February, but since then the government’s long-term borrowing cost has declined from 17% to 11%. There have been political developments in Brazil with the impeachment of President Rousseff and while President Temer has brought some stability, there is no real change yet. But ultimately, Brazil has benefited from the same trends as South Africa since the start of the year: firmer commodity prices, improved global sentiment towards emerging markets, currency appreciation, a better inflation outlook and prospects for interest rate cuts (the central bank has already delivered one small cut).

Little detail on growth-enhancing reforms

The first downgrade is therefore widely expected and shouldn’t cause massive market reaction. The key questions are whether one downgrade will be followed by others, or whether the ship will be steadied? The key issue is faster growth over the long term. Government plans to grow its fixed investment spending by 4% in real terms per year on average over the next three years. Unfortunately, there was little detail on other measures and reforms that would lift South Africa’s growth potential. The main initiatives are clearly still a work in progress (and subject to much contestation). Government is still “finalising” a regulatory framework that would allow greater private-sector participation in infrastructure projects. There was also no detail on addressing “legislative and regulatory uncertainties” that constrain mining and agriculture. Nor on the mooted rationalisation or selling off of public assets “that are no longer relevant to Government’s development agenda”. Crucial labour market reforms are also still underway, with ratings agencies having expressed a particular concern over the negative side-effects of a proposed national minimum wage.

We will therefore have to wait for the February Budget Speech (and beyond) to get clarity on these measures. The problem is that many of these reforms fall outside Treasury’s direct ambit.

Chart 1: Consolidated projected medium-term budget balance (negative number implies a deficit)

Source: National Treasury