Looking a bit better

Dave Mohr, Chief Investment Strategist, at Old Mutual Multi-Managers

Izak Odendaal, Investment Strategist, at Old Mutual Multi-Managers

October was nothing short of a horror show for global equities. The MSCI All Countries World Index lost 7.4% in US dollars in the month, dragging year-to-date returns into negative territory.

The high-flying US S&P 500 Index lost 6.8% in October, but is still positive in 2018. The MSCI Emerging Markets extended year-to-date losses by dropping a further 8.7% in October. The local market was also not spared. The FTSE/JSE All Share Index lost 5.7% in October, and is in the red year-to-date and over one year.

Turning around

But the last few days have seen a promising turnaround. Why? The main reason is that the sell-off was probably overdone, as it usually is, and bargain-hunters piled in.

Another reason is that the underlying economic conditions are still pretty solid. The US added 250 000 new jobs in October, well ahead of market expectations for 190 000 jobs, and the unemployment rate remains a 49-year low of 3.7%. While wage growth has accelerated somewhat, it is still around 3% on most measures and below the prevailing rate seen at similar points of past cycles, and certainly well below where the unemployment rate has historically suggested it should be.

There are three interpretations of this: Firstly, it is only a matter of time before wage growth shoots up as scarce workers (job openings outnumber active job seekers in the US) bid up wages.

Secondly, there is something more fundamental depressing wages, particularly the lack of bargaining power in an age of outsourcing, offshoring and automation. The third interpretation is that there is simply more slack in the labour market than the headline unemployment number suggests, in the form of people who could work but aren’t actively looking for work or people working part time who would prefer full-time employment. On balance, the evidence favours the latter two explanations.

In any event, the Federal Reserve’s preferred inflation measure, the personal consumption expenditure deflator, softened to 2% in September, in line with its target. While the market turmoil is unlikely to prevent a December hike, the lack of upward inflationary pressure still suggests that the Fed will hike gradually, and that monetary policy overkill is unlikely.

Eurozone growth disappointed in the third quarter, slowing to 1.7% year-on-year. However, this is still in line with the long-term average growth rate of the Eurozone economy, after several quarters of above-average growth. Slowing growth in the Eurozone creates a headache for the European Central Bank (ECB), which left policy unchanged at its October meeting.

The ECB still plans to end its large-scale bond purchase programme (quantitative easing) at the end of the year and start hiking rates mid-2019. However, despite all its efforts, core inflation (excluding food and fuel prices) has been stubbornly stuck around 1%. The ECB’s view is that the slowdown in growth is temporary (one-off issues affected German car manufacturers, for instance) and that the continued decline in unemployment (8.1% In September) will lead to firmer wage growth ultimately pushing inflation closer to target. In other words, it expects the same mechanism that hasn’t worked in the US to raise inflation in Europe. It is therefore also unlikely that interest rates will rise sharply in Europe.

Thirdly, global companies are reporting strong profit growth numbers. US S&P 500 companies are reporting 27% earnings growth in the third quarter compared to a year ago, benefiting from the company tax cut in December. European shares don’t have the benefit of tax cuts and face a weaker domestic economy than their American counterparts, but Eurostoxx 600 companies are still posting decent 14% earnings growth, according to Thomson Reuters. These companies thus benefit from a strong overall global economy.

An often overlooked technical factor is that companies aren’t allowed to purchase their own shares in the weeks leading up to earnings announcements. Therefore, a substantial participant in the market - Goldman Sachs estimates buybacks will total $1 trillion this year - has been largely absent during the worst days of the sell-off for regulatory reasons. With results season now wrapping up, these buyers are returning. US companies buy-back shares to a much greater degree than elsewhere, but if the US market rises, it tends to set the tone globally.

The final catalyst supporting the markets over the past few days is a potential thawing of US-China trade relations, particularly after a “long and very good” phone call between US President Donald Trump and Chinese President Xi Jinping ahead of a formal meeting at the G20 summit later this month. Worries of a trade war between the world’s two largest economies have weighed on investor sentiment since the start of the year. There is clearly some way to go before the issues are resolved, but as long as tensions don’t escalate further, that is already a positive. In the meantime, authorities in Beijing have signalled stimulus measures to prevent the economy from sliding further.

On the local side, Naspers, the largest share on the JSE, jumped 18% between Tuesday and Friday, having slumped in October. The reason of course has nothing to do with South Africa, and everything to do with the company’s stake in Chinese internet giant Tencent. Tencent in turn bounced with the rest of the battered Chinese equity market (the Shanghai Composite is still down 20% in yuan terms this year).

Good news and bad news

In this way, the fortunes of local investors are very much tied to China. But what about developments in the local economy? There’s some good news and bad news.

On the negative side, South Africa posted a surprise R2 billion trade deficit in September according to SARS customs data, with economists expecting a surplus. It means that the year-to-date trade balance is marginally in deficit, compared to a R44 billion surplus in 2017. The difference is largely due to a 37% jump in the oil import bill. For the first nine months of 2018, South Africa ran a surplus of R67.8 billion with Botswana, eSwatini, Lesotho and Namibia (the BELN countries) and a R68.2 billion deficit with the rest of the world.

The most up-to-date ‘hard’ economic indicator (as opposed to ‘soft’ survey data) is new vehicle sales numbers, which are released on the second day of the next month. Other data points like manufacturing and mining output are produced with a two-month lag, and GDP with a three-month lag. Passenger vehicle sales shows consumer confidence and the availability of credit, while commercial vehicle sales provides information on business sentiment. South Africa also exports new vehicles.

In October, vehicle sales were up 1.7% from a year ago, which doesn’t sound like much, but does represent the best month so far this year, and tentatively points to better days ahead. New vehicle prices have increased less than consumer inflation this year (2.9% year-on-year in September) so new cars have become cheaper in real terms. Instalment credit, the category of credit that includes vehicle loans, increased by 6.7% from a year ago, the fastest pace since 2015.

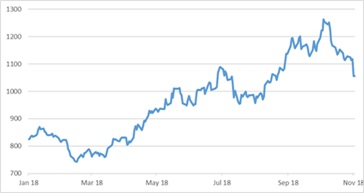

Potentially supporting this is good news on the petrol price front. While equity prices rebounded somewhat last week, oil prices didn’t. The US will exempt eight countries from complying with its sanctions on Iran which took effect over the weekend. Strong output growth from the US shale fields have also weighed on the price. Together with a firmer rand, this means that South Africans can now look forward to petrol price cuts in December (if current conditions prevail).

The decline in the oil price is clearly good news for the trade balance as well, especially since the dollar prices of some of South Africa’s key export commodities – iron ore, gold and palladium - have picked up over the past few weeks.

Sentiment can shift quickly

It is still too early to tell if the market rebound of the past few days can hold (if it does, it certainly won’t be at the same blistering pace). There is also still a lot of ground to catch up, especially for the local equities. But it does highlight how quickly sentiment can shift, even if nothing changes on the ground. This in turn warns strongly against trying to time the market. Though it is possible to argue that markets should turn by looking at the fundamentals, it is impossible to know when they’ll turn. When it does turn, the market tends to turn rapidly and missing out on those first few days can result in much lower overall returns from equities. Hence the old saying, what counts is “time in the markets, not timing the markets.”

Chart 1: Major equity indices in 2018, rebased to 100

Source: Thomson Reuters Datastream

Chart 2: Brent oil price, rand per barrel

Source: Thomson Reuters Datastream

Chart 3: Local new vehicle sales (number of units)

Source: Naamsa