Long-term investment strategies vs Award winners

Kamil Maharajh, Research & Investment Analyst at Glacier by Sanlam.

Every year we see asset managers walking away with awards, based on returns and risk-adjusted returns. These include the Raging Bull, MorningStar and PlexCrown awards. The question then of whether it is a sensible long-term investment strategy to invest in these managers’ funds after they’ve won, proves to be an interesting one.

The Raging Bull is awarded every year, in January, to the best performing fund, NAV to NAV, over the past three years in each of the ASISA categories. I conducted a study from 1 February 2006 to 2016 (10-year period). I looked at the Raging Bull award winners over the past 10 years, in the SA Equity General and SA Multi-Asset Flexible ASISA categories, and compared the returns one would receive if one followed an investment strategy of investing in the award-winners, switching from one winner to the next over 10 years, to a strategy where one invests in a single fund over the same period (10 years ending 31 January 2016).

SA Equity General

In this category, the past 10 Raging Bull winners were as follows:

2006 PSG Alphen Growth (Equity)

2007 Prudential Equity

2008 Allan Gray Equity

2009 Prudential Dividend Maximiser

2010 ABSA Select Equity

2011 Marriott Dividend Growth

2012 PSG Equity

2013 SASFIN Value

2014 MAZI MET Equity

2015 Harvard House General Equity

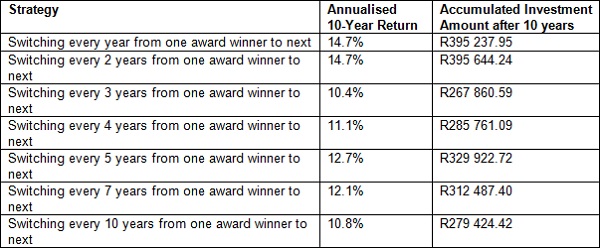

There were 56 funds available in this category at the start of the 10-year period. The strategy in which one switches from one award winner to the next every year would be the most relevant for this study, but I have also taken into account strategies where one invests in an award winner for a longer period (two to five years) so that we can compare shorter and longer-term investment horizons.

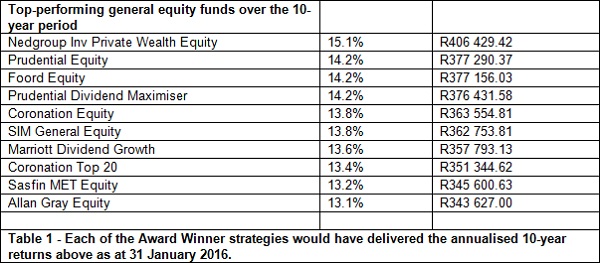

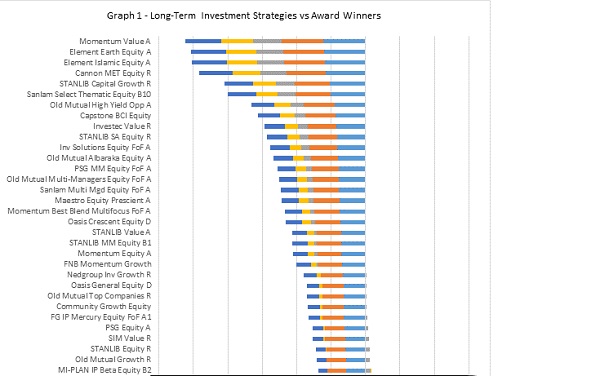

Graph 1 – Each stacked bar shows the cumulative over- or under-performance of investment in the equity funds only against the strategies of investing in award-winners only (switching to the next winner every year, two years, three years, four years or five years). We see the qualitatively stronger asset managers (such as Allan Gray, Nedgroup Investments and Sanlam Investments) begin to stand out once investment periods become longer than two years.

Over shorter investment periods (one and two years), we see strategies of investing in award winners outperform the strategy of investing in a single fund over the long term. The strategy of investing in award winners would suit the ‘trading’ investors, but they would also need to deal with the additional costs and taxes involved in trading more frequently. As we move into longer investment periods (three years and greater), which are recommended for equities, we begin to see the strategies of investing in the award winners lose their steam and underperform compared to the strategy of investing in a single fund over the long term. In this category, unit trusts are required to be invested in 80% equities at all times. This means that they have much longer investment horizons, due to the nature of equities, to meet their performance objectives. They would not be able to leave the equity asset class if they cannot find any value or there is a sudden correction or shock. This is why shorter-term investment strategies, and switching more frequently, would not be recommended in this more aggressive asset class.

SA Multi-Asset Flexible

In this category, these were the last 10 Raging Bull award winners:

2006 RMB High Tide

2007 ABSA Flexible

2008 Centaur BCI Flexible

2009 Rezco Value Trend

2010 BlueAlpha BCI All Seasons

2011 PSG Flexible

2012 36ONE MET Flexible Opportunity

2013 36ONE MET Flexible Opportunity

2014 Autus BCI Opportunity

2015 Bateleur Flexible Prescient

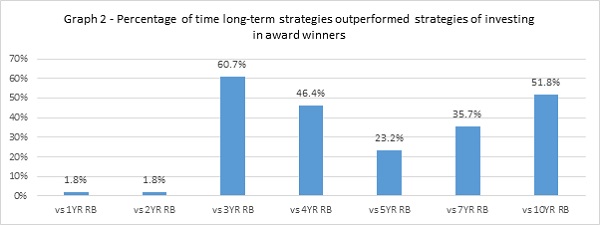

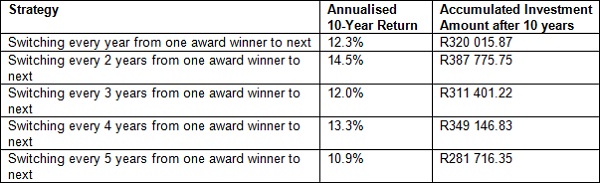

There were 29 funds available at the start of the 10-year period. I have summarised the results by comparing the strategy of investing in a single fund over 10 years to the strategies of investing in an award winner over one to five year periods before switching to the next award winner.

Assuming an initial investment amount of R100 000:

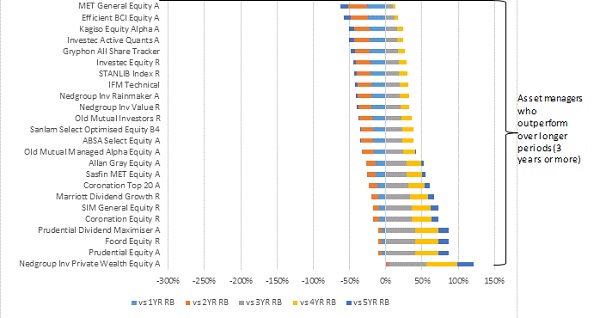

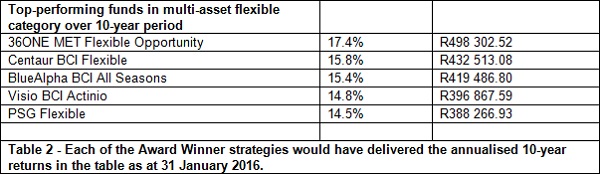

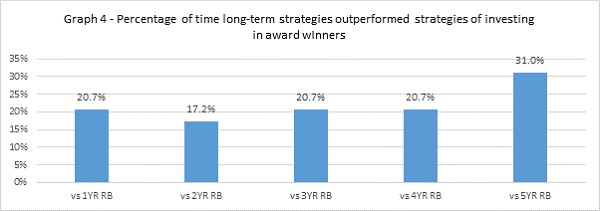

Looking at the top five funds in the category, we see that they were able to consistently outperform all strategies of investing in the award winners, regardless of when the switches took place.

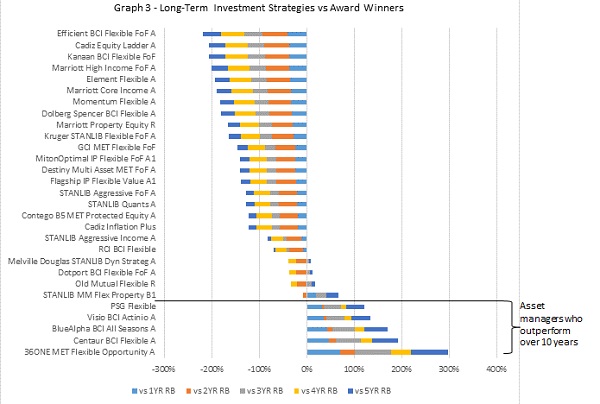

Graph 3 – The above graph again cumulatively stacks the accumulated invested amount in each fund, divided by each of the strategies of investing in award winners. If the values are positive, they indicate the percentage by which a 10-year investment in a single fund outperformed each of the strategies of investing in the award winners.

In this category, which allows asset managers to switch completely between asset classes, with a maximum allocation to offshore assets of 25%, we can see that a quality asset manager would always be able to outperform any strategy which chases award winners. The rules of the category allow them to choose asset classes they believe have the most value, and to avoid asset classes in which they see no value.

Conclusion

Through this study, we have identified that chasing award winners may provide superior returns over shorter investment periods. However, due to the long-term investment horizons required with the more aggressive funds, we find that the award winner strategies begin to lose some of their momentum as we look at periods of three years or more. This trend is seen in both the SA equity and SA flexible categories. Award winners may be of the highest quality in terms of investment teams, processes and philosophy, but chasing them each year does not lead to consistent, long-term outperformance. At Glacier Research we believe that investing in quality asset managers for longer investment periods, allowing the asset managers to use their skill and expertise to achieve their investment objectives, would be the most successful investment strategy.