Locked down but fighting back

South Africa is now in full lockdown to prevent the further spread of the coronavirus.

We have joined several other nations that have taken the decision to put life and health ahead of economic considerations. There is no doubt that these measures will hurt our economy deeply, just as they have brought economic activity to a sudden and shuddering halt elsewhere. On the same day that President Ramaphosa made his historic announcement, his UK counterpart Boris Johnson also put his country into lockdown. The difference is that the UK had 6 600 confirmed cases at that point, while South African had only 402. Our faster response gives us a fighting chance despite our much weaker public health system.

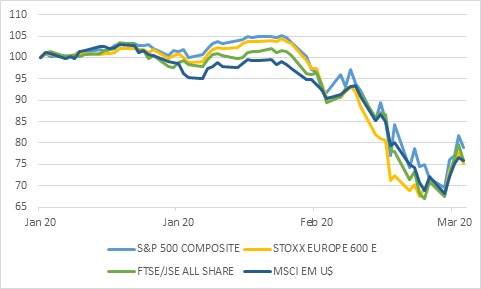

Chart 1: A better week for global equities

Source: Refinitiv Datastream

Big bazookas

The other big news item during the week was the massive fightback effort from policymakers across the globe. Starting with monetary policy in the US, the Federal Reserve last Monday announced effectively unlimited purchases of US government bonds, along with significant purchases of municipal bonds and mortgage backed securities, as well as for the first time, large quantities of corporate bonds.

The main reason for the Fed’s intervention is not to drive long-term interest rates down as in previous rounds of quantitative easing (QE). Instead, the Fed is trying to keep markets functioning smoothly. The scramble for cash has led to rapid withdrawals from the various different funding markets. Banks have been unable to fulfil their usual market-making role since they are wary of taking on more risk on their balance sheets, having already had to increase loans to cash-strapped customers. With so many investors running for the exits, wide gaps have opened between what sellers want and what buyers are prepared to pay, typical of constrained liquidity. The growth of bond exchange traded funds (ETFs) has exacerbated the problem, since they promised investors that they would be able to get out instantly, even though some of their underlying holdings are illiquid.

Also in the US, Congress approved a $2 trillion fiscal support package. This is a staggering number (around 9% of US GDP) that would have been completely unthinkable only a few weeks ago. But this is the new normal, and it might not even be large enough. Other countries have announced packages of a similar scale relative to the size of their economies.

Will it work? For one thing it is likely to be more effective than interest rate cuts. Businesses are closed and consumers are staying at home. The immediate problem is an unprecedented loss of income across the economy (though it is clearly more concentrated in tourism, travel, restaurants and face-to-face services).

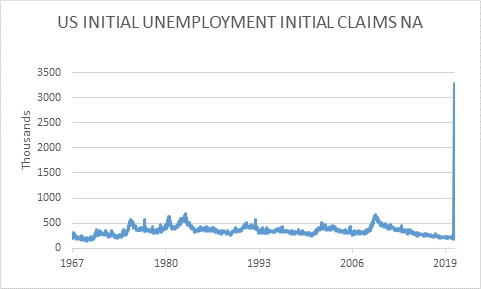

The fiscal package aims to address this through cheques mailed directly to households, extended unemployment benefits, loans and bridging finance to companies. Like other governments across the world, the US might end up buying equity stakes in struggling companies. These steps will be necessary to prevent businesses shutting for good and laying off even more workers. Already, new unemployment insurance claims in the US jumped to 3.25 million, the largest weekly increase since record keeping began in 1967. Even in the depths of the Great Recession of 2008/09, the highest weekly increase in new claims was ‘only’ 665 000.

Chart 2: New unemployment insurance claims in the US

Source: Refinitv Datastream

The South African government has also cobbled together a support plan, but it is not even in the same ballpark as what other countries are doing for the simple reason that it has no fiscal space. Government’s spending already exceeded tax revenues by several hundred billion rand before this crisis hit, and its debt to GDP ratio doubled in the past decade. On top of this, Eskom’s unsustainable debt load still needs to be absorbed somehow. Now tax revenues are likely to slump while coronavirus-related spending is going to increase. The projected 6.8% of GDP budget deficit for the current year – already large - could end up in double digits. When the 2008 crisis hit, government debt was low and it had a budget surplus. We approached the current crisis with no ammunition in the store.

Junked

It is therefore unsurprising that Moody’s downgraded South Africa’s last remaining investment grade rating. Like Fitch and S&P, Moody’s also maintained a negative outlook, meaning that more downgrades could follow. While the ratings cut was likely even without the corona crisis, it should also be noted that global economic downturns tend to lead to widespread downgrades across countries and industries.

Whether Moody’s decision will lead to further significant outflows from our bond market remains to be seen. However, it was widely anticipated and therefore likely priced in. Besides, as they de-risked portfolios and attempted to raise cash, global investors have pulled an estimated $60 billion from emerging markets this year. This included heavy selling of South African bonds. How the global coronavirus crisis evolves from here is going to have a larger impact on our markets than the ratings downgrade.

QE-ish

Our bond and money markets also experienced liquidity strains. This led to the Reserve Bank announcing an intervention to maintain liquidity in local bond and money markets. Since it transmits monetary policy through these markets, their smooth functioning is crucial. Though it said it will purchase government bonds across the yield curve, it did not disclose the amount. It is likely to be very small relative to other major markets.

By not disclosing the amount, the policy loses some of its potency. The biggest impact of quantitative easing as conducted by other countries in the past decade is not the actual ‘flood of money’ (which mostly ended up returning to central banks in the form of excess reserves) but rather the message that it sent, namely that the central bank in question was serious about achieving its objective. Putting a number on the size of the programme can help give it a positive ‘shock and awe’ quality.

Flattening the other curve

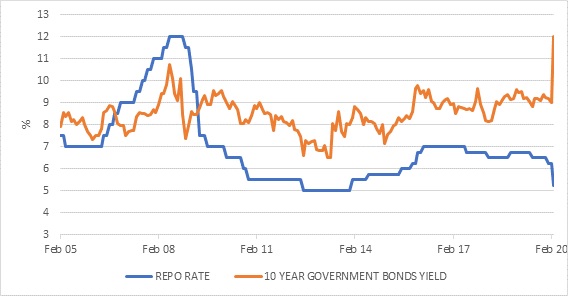

The SARB should be much more ambitious. Extraordinary times call for extraordinary measures. The difference between short-term interest rates (which it controls directly) and long-term bond yields (which are set by the market) has blown out to record levels. The SARB should buy as many government bonds as needed to flatten the yield curve. Otherwise, what is the point of cutting short-term interest rates by 100 basis points when long-term rates rise by 200 bps? A narrow interpretation of the SARB’s mandate amid an unprecedented global natural disaster could cause lasting damage.

Chart 3: Short and long-term interest rates in South Africa

Source: Refinitiv Datastream

The SARB insists that its intervention is not quantitative easing, but that’s largely semantics at this point. Some might fret that this could lead to Zimbabwe-style hyperinflation, but it is extremely unlikely. For one thing, the experience with QE in the US, Europe and Japan over the past decade is that it failed to raise inflation sufficiently. Hyperinflation is also usually a symptom of economic dysfunction rather than a cause, occurring in countries where inflation was typically already high and where central banks lack independence from government (not the case in South Africa). Note also that central banks buy bonds in the open market from financial institutions when engaging in quantitative easing, rather than sending cheques directly to government departments. In the case of South Africa, the SARB is not allowed to buy bonds directly from government, and government would still have to sell its bonds to the market to fund itself.

Most importantly, the global backdrop is one where many central banks are buying government debt in large quantities. The SARB would not stand out if it did the same. Other central banks are adopting a “whatever it takes” approach. To put it into perspective, the Fed’s actions could easily amount to $2 trillion in total purchases of debt securities, over and above the $4.5 trillion it bought between 2008 and 2015. Meanwhile, the ECB has removed most of the self-imposed limits on its expanded €750bn QE programme, giving it new flexibility. Previously it would only buy up to a third of a country’s outstanding debt, only longer-dated securities, and excluding riskier countries like Greece. Korea, Australia and Canada have also embarked on versions of quantitative easing for the first time. Things are moving so quickly that rulebooks are being rewritten on an almost daily basis.

Staying alive, staying invested

The unprecedented global policy response to an unprecedented global crisis has buoyed markets over the past few days. However, it is far too early to say if the worst is over for investors. Certainly from a public health point of view, infection rates in Europe and North America are still climbing, and it is still early days in the infection cycle in places like Africa, South America and India. This means the economic impact of lockdowns, quarantines and social distancing will still be felt for several weeks, if not months. But markets are likely to turn before the virus completely disappears.

The old saying of market veterans is that nobody rings a bell at the bottom (or the top for that matter). It will be true this time too. There is tremendous uncertainty now, but there will still be plenty of unanswered questions when markets do turn. The rise in US unemployment claims mentioned above reached a crescendo in March 2009, exactly when the stock market bottomed. In other words, the market bottomed when conditions on the ground were unimaginably bad. Market rebounds are unpredictable and cannot be timed, and remaining invested is the only way to make sure you participate.